We propose a framework for designing Target-Date Funds (TDFs) around an explicit return objective while controlling risk directly at the portfolio level through a declining Conditional Value-at-Risk (CVaR) constraint. In this approach, the regulator or sponsor specifies a CVaR glidepath that gives the portfolio manager enough flexibility to reach a target return with a reasonably high probability. The target return is determined exogenously from pension-design inputs such as retirement age, contribution rate, working years, life expectancy, and replacement-rate goals. This differs from conventional TDF design, where age-dependent asset-class limits are set without an explicit link to a required return.

A key feature of the method is that it does not assume the manager selects an optimal portfolio each period. Instead, each month the manager draws an allocation from the set of portfolios satisfying the CVaR constraint. This yields a conservative evaluation of each glidepath: success probabilities are averages over admissible allocations, rather than best-case outcomes. We introduce two figures of merit: the probability of meeting the target return and the cumulative risk assumed over the life of the TDF.

As a proof of concept, we apply the framework to Chile's 2025 pension reform using nine Chilean and global asset classes and a 40-year accumulation horizon. The results show that the transition age at which risk starts to decline is the most consequential design parameter, and that contribution density acts as a hard constraint: below a critical threshold, portfolio design alone cannot compensate for structurally low contributions. The framework is general and can be applied to any TDF designed around an explicit return objective.

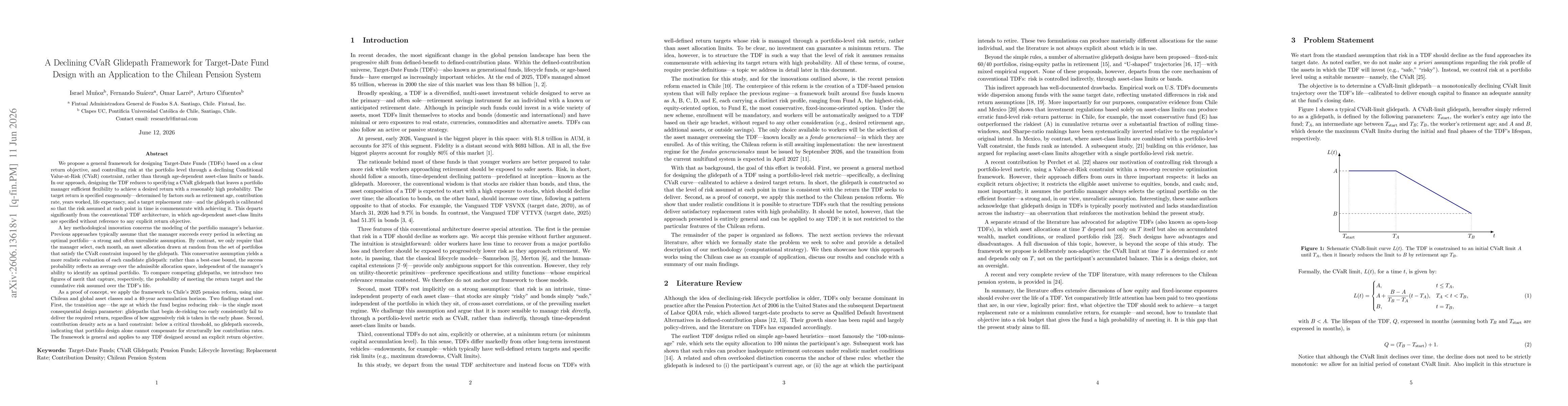

Discussion 0