Publication

Metrics

AI Quick Summary

This paper develops multifractal random walk inference tools for financial data, including smoothing, filtering, and volatility forecasting methods. Applied to Oslo Stock Exchange data, these techniques reveal more complex volatility structures compared to basic stochastic volatility models.

Paper Preview

Abstract

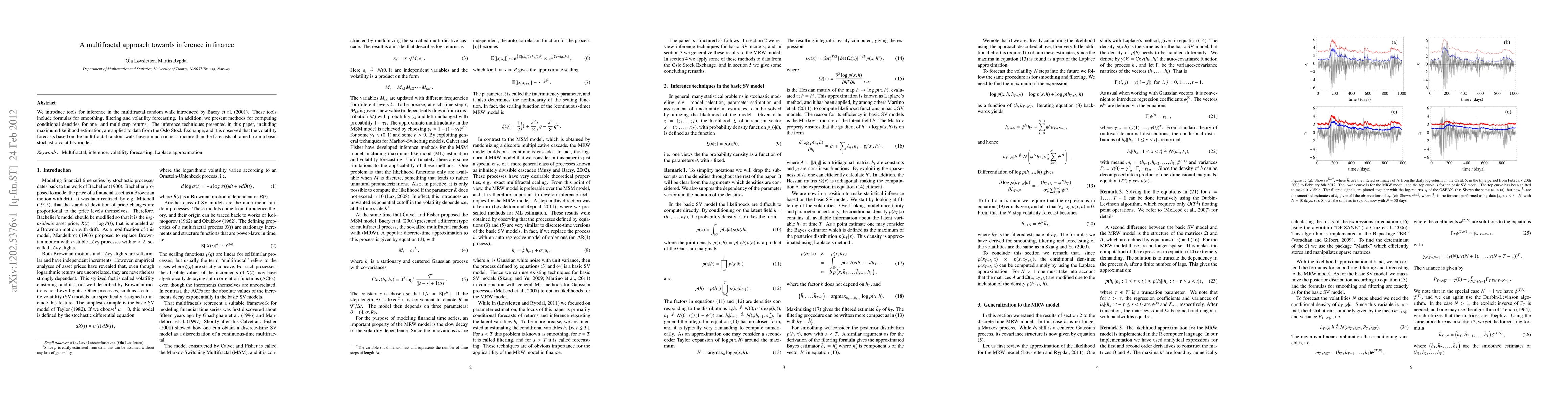

We introduce tools for inference in the multifractal random walk introduced by Bacry et al. (2001). These tools include formulas for smoothing, filtering and volatility forecasting. In addition, we present methods for computing conditional densities for one- and multi-step returns. The inference techniques presented in this paper, including maximum likelihood estimation, are applied to data from the Oslo Stock Exchange, and it is observed that the volatility forecasts based on the multifractal random walk have a much richer structure than the forecasts obtained from a basic stochastic volatility model.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0