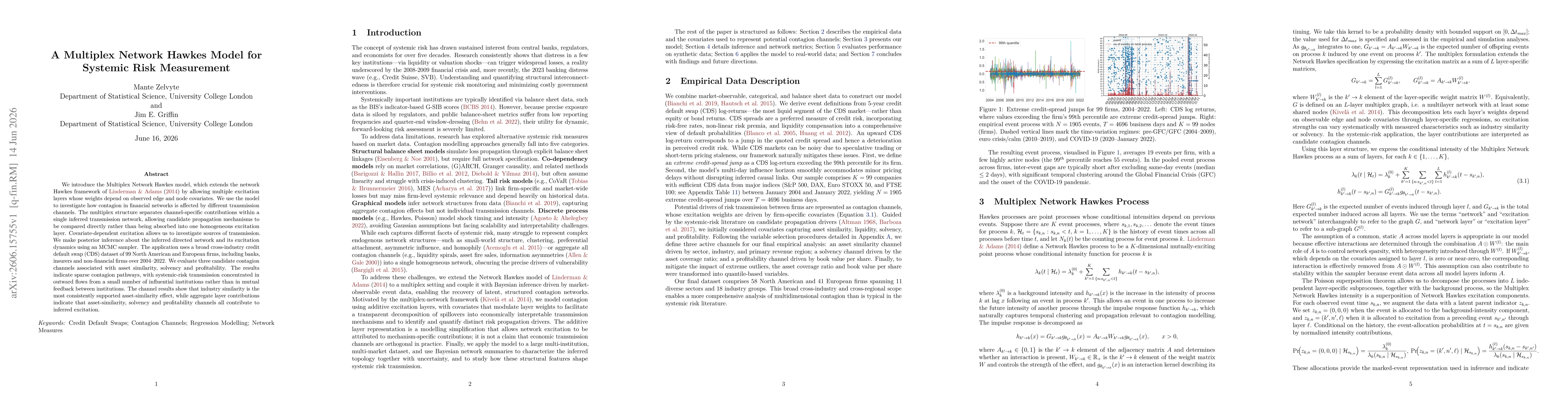

We introduce the Multiplex Network Hawkes model, which extends the network Hawkes framework of Linderman & Adams (2014) by allowing multiple excitation layers whose weights depend on observed edge and node covariates. We use the model to investigate how contagion in financial networks is affected by different transmission channels. The multiplex structure separates channel-specific contributions within a single inferred transmission network, allowing candidate propagation mechanisms to be compared directly rather than being absorbed into one homogeneous excitation layer. Covariate-dependent excitation allows us to investigate sources of transmission. We make posterior inference about the inferred directed network and its excitation dynamics using an MCMC sampler. The application uses a broad cross-industry credit default swap (CDS) dataset of 99 North American and European firms, including banks, insurers and non-financial firms over 2004-2022. We evaluate three candidate contagion channels associated with asset similarity, solvency and profitability. The results indicate sparse contagion pathways, with systemic-risk transmission concentrated in outward flows from a small number of influential institutions rather than in mutual feedback between institutions. The channel results show that industry similarity is the most consistently supported asset-similarity effect, while aggregate layer contributions indicate that asset-similarity, solvency and profitability channels all contribute to inferred excitation.

Discussion 0