An approximate solution for the power utility optimization under predictable returns

Publication

Metrics

AI Quick Summary

Researchers developed an approximate solution for optimizing power utility portfolios using a multivariate normal distribution, with a focus on machine learning algorithm Gradient Descent.

Paper Preview

Abstract

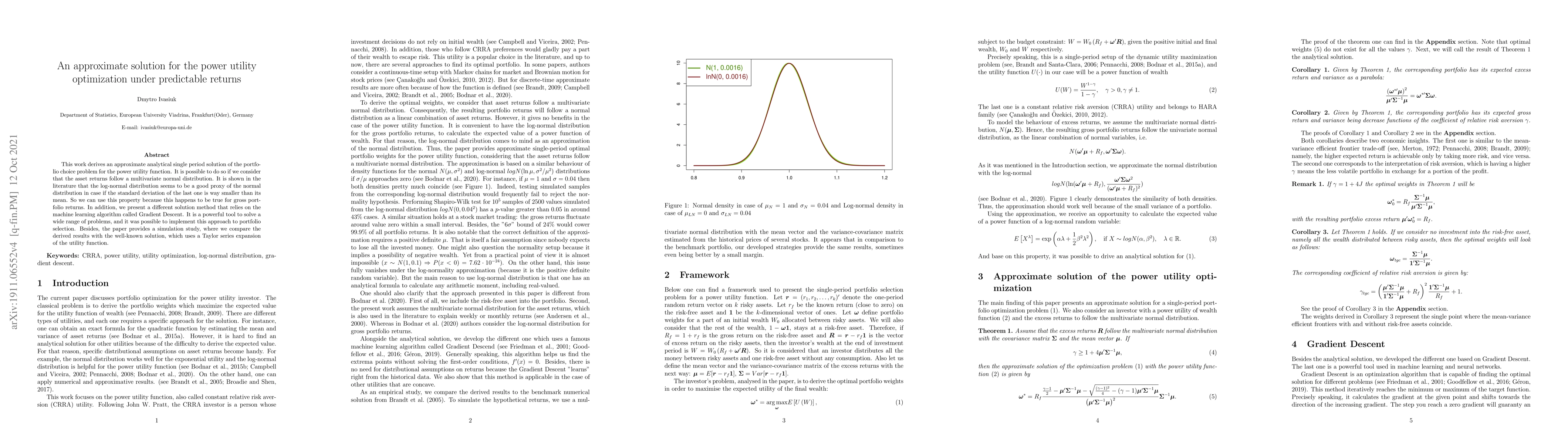

This work derives an approximate analytical single period solution of the portfolio choice problem for the power utility function. It is possible to do so if we consider that the asset returns follow a multivariate normal distribution. It is shown in the literature that the log-normal distribution seems to be a good proxy of the normal distribution in case if the standard deviation of the last one is way smaller than its mean. So we can use this property because this happens to be true for gross portfolio returns. In addition, we present a different solution method that relies on the machine learning algorithm called Gradient Descent. It is a powerful tool to solve a wide range of problems, and it was possible to implement this approach to portfolio selection. Besides, the paper provides a simulation study, where we compare the derived results with the well-known solution, which uses a Taylor series expansion of the utility function.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0