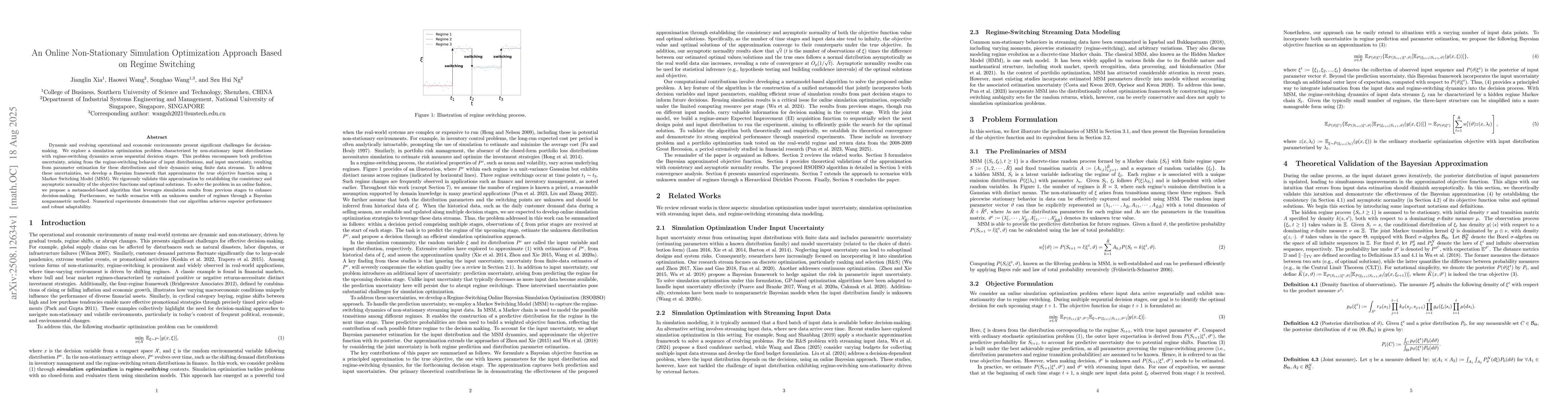

An Online Non-Stationary Simulation Optimization Approach Based on Regime Switching

Publication

Metrics

Paper Preview

Abstract

Dynamic and evolving operational and economic environments present significant challenges for decision-making. We explore a simulation optimization problem characterized by non-stationary input distributions with regime-switching dynamics across sequential decision stages. This problem encompasses both prediction uncertainty, arising from the regime-switching behavior of input distributions, and input uncertainty, resulting from parameter estimation for these distributions and their dynamics using finite data streams. To address these uncertainties, we develop a Bayesian framework that approximates the true objective function using a Markov Switching Model (MSM). We rigorously validate this approximation by establishing the consistency and asymptotic normality of the objective functions and optimal solutions. To solve the problem in an online fashion, we propose a metamodel-based algorithm that leverages simulation results from previous stages to enhance decision-making. Furthermore, we tackle scenarios with an unknown number of regimes through a Bayesian nonparametric method. Numerical experiments demonstrate that our algorithm achieves superior performance and robust adaptability.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0