Financial time series forecasting faces a fundamental challenge: predicting

optimal asset allocations requires understanding regime-dependent correlation

structures that transform during crisis periods. Existing graph-based

spatio-temporal learning approaches rely on predetermined graph

topologies--correlation thresholds, sector classifications--that fail to adapt

when market dynamics shift across different crisis mechanisms: credit

contagion, pandemic shocks, or inflation-driven selloffs.

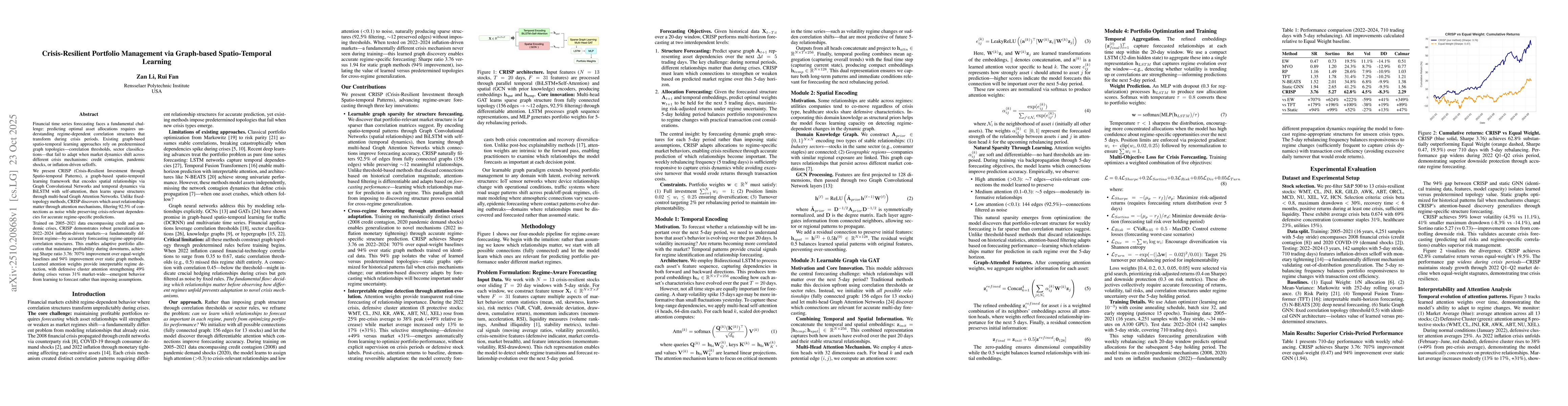

We present CRISP (Crisis-Resilient Investment through Spatio-temporal

Patterns), a graph-based spatio-temporal learning framework that encodes

spatial relationships via Graph Convolutional Networks and temporal dynamics

via BiLSTM with self-attention, then learns sparse structures through

multi-head Graph Attention Networks. Unlike fixed-topology methods, CRISP

discovers which asset relationships matter through attention mechanisms,

filtering 92.5% of connections as noise while preserving crisis-relevant

dependencies for accurate regime-specific predictions.

Trained on 2005--2021 data encompassing credit and pandemic crises, CRISP

demonstrates robust generalization to 2022--2024 inflation-driven markets--a

fundamentally different regime--by accurately forecasting regime-appropriate

correlation structures. This enables adaptive portfolio allocation that

maintains profitability during downturns, achieving Sharpe ratio 3.76: 707%

improvement over equal-weight baselines and 94% improvement over static graph

methods. Learned attention weights provide interpretable regime detection, with

defensive cluster attention strengthening 49% during crises versus 31%

market-wide--emergent behavior from learning to forecast rather than imposing

assumptions.

Discussion 0