01

MethodologyHow they did it

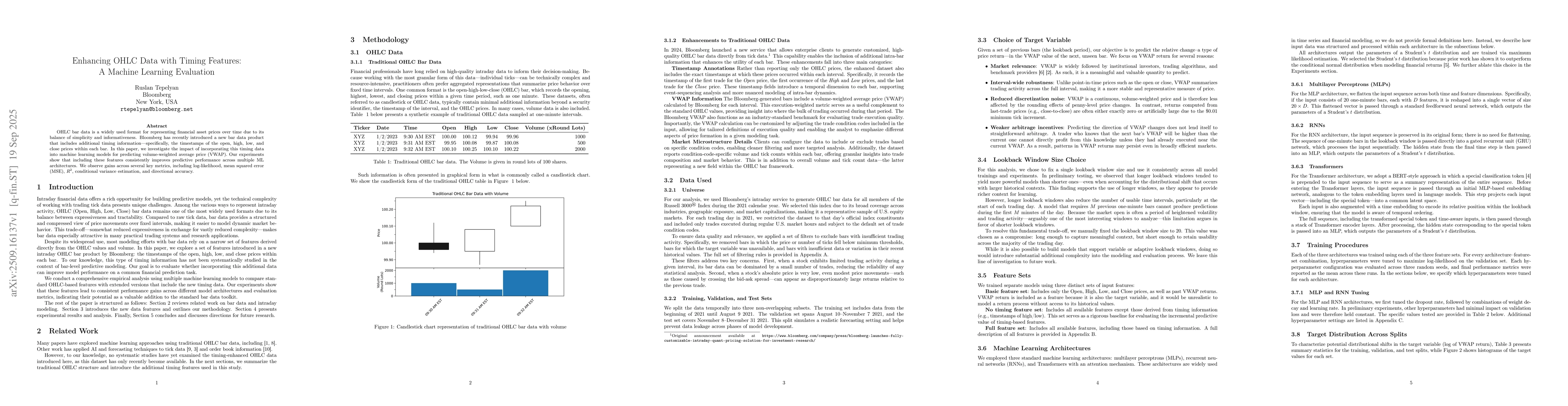

The study evaluates machine learning models for predicting volume-weighted average price (VWAP) using OHLC data enhanced with timing features. It compares three architectures (MLP, RNN, Transformer) across three feature sets (basic, no timing, full) using metrics like NLL, MSE, R2, and directional accuracy. The models are trained and validated on different splits of the dataset, with hyperparameters tuned for optimal performance.

Discussion 0