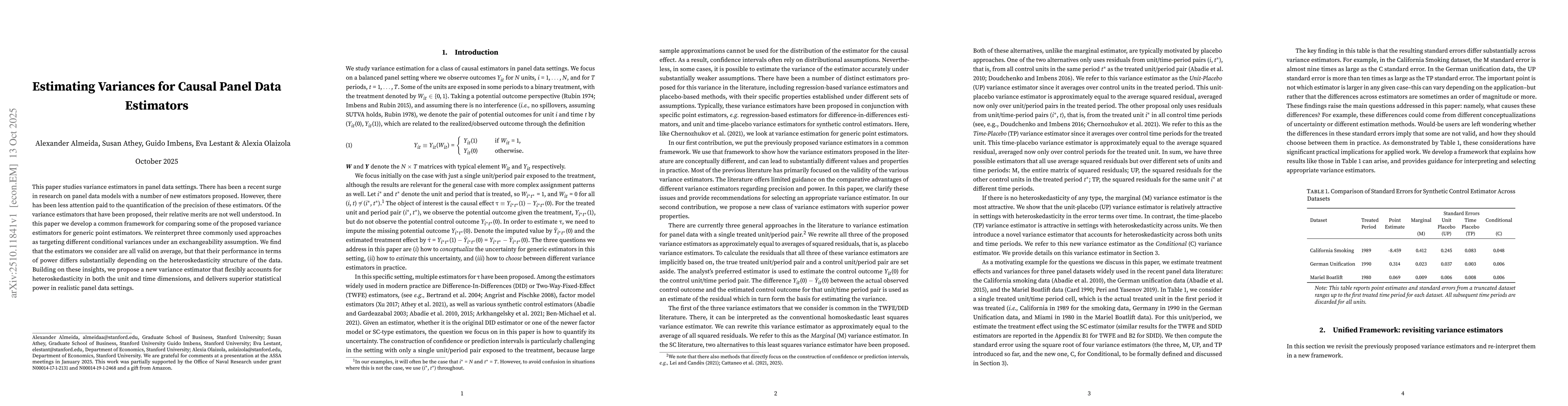

This paper studies variance estimators in panel data settings. There has been

a recent surge in research on panel data models with a number of new estimators

proposed. However, there has been less attention paid to the quantification of

the precision of these estimators. Of the variance estimators that have been

proposed, their relative merits are not well understood. In this paper we

develop a common framework for comparing some of the proposed variance

estimators for generic point estimators. We reinterpret three commonly used

approaches as targeting different conditional variances under an

exchangeability assumption. We find that the estimators we consider are all

valid on average, but that their performance in terms of power differs

substantially depending on the heteroskedasticity structure of the data.

Building on these insights, we propose a new variance estimator that flexibly

accounts for heteroskedasticity in both the unit and time dimensions, and

delivers superior statistical power in realistic panel data settings.

Discussion 0