01

MethodologyHow they did it

Brief description of the research methodology used

Brief description of the research methodology used More in Methodology →

Main finding 1 — Main finding 2 More in Key Results →

Why this research is important and its potential impact More in Significance →

Limitation 1 — Limitation 2 More in Limitations →

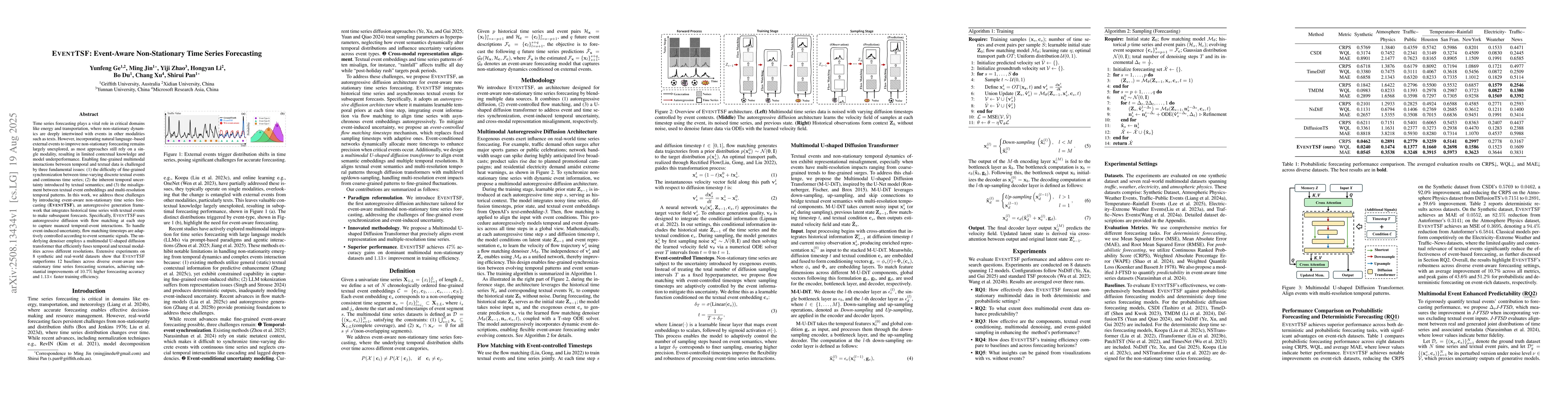

Time series forecasting plays a vital role in critical domains like energy and transportation, where non-stationary dynamics are deeply intertwined with events in other modalities such as texts. However, incorporating natural language-based external events to improve non-stationary forecasting remains largely unexplored, as most approaches still rely on a single modality, resulting in limited contextual knowledge and model underperformance. Enabling fine-grained multimodal interactions between temporal and textual data is challenged by three fundamental issues: (1) the difficulty of fine-grained synchronization between time-varying discrete textual events and continuous time series; (2) the inherent temporal uncertainty introduced by textual semantics; and (3) the misalignment between textual event embeddings and multi-resolution temporal patterns. In this work, we address these challenges by introducing event-aware non-stationary time series forecasting (EventTSF), an autoregressive generation framework that integrates historical time series with textual events to make subsequent forecasts. Specifically, EventTSF uses autoregressive diffusion with flow matching at each step to capture nuanced temporal-event interactions. To handle event-induced uncertainty, flow matching timesteps are adaptively controlled according to event semantic signals. The underlying denoiser employs a multimodal U-shaped diffusion transformer that efficiently fuses temporal and textual modalities across different resolutions. Extensive experiments on 8 synthetic and real-world datasets show that EventTSF outperforms 12 baselines across diverse event-aware non-stationary time series forecasting scenarios, achieving substantial improvements of 10.7% higher forecasting accuracy and $1.13\times$ faster training efficiency.

Seven facets of this paper, analysed and brought into focus by AI.

Why this research is important and its potential impact

Brief description of the research methodology used

Why this research is important and its potential impact

Main technical or theoretical contribution

What makes this work novel or different from existing research

Discussion 0