Publication

Metrics

AI Quick Summary

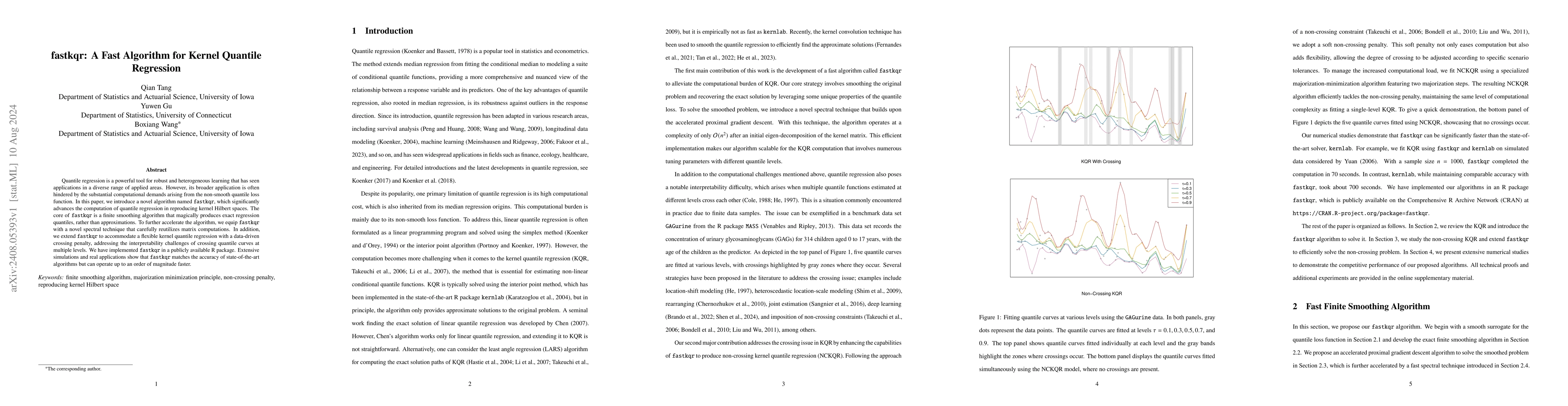

This paper introduces fastkqr, a novel algorithm for efficient kernel quantile regression that uses a finite smoothing technique and spectral methods to achieve exact quantiles with significantly reduced computational costs, outperforming existing methods by up to an order of magnitude while maintaining accuracy.

Paper Preview

Abstract

Quantile regression is a powerful tool for robust and heterogeneous learning that has seen applications in a diverse range of applied areas. However, its broader application is often hindered by the substantial computational demands arising from the non-smooth quantile loss function. In this paper, we introduce a novel algorithm named fastkqr, which significantly advances the computation of quantile regression in reproducing kernel Hilbert spaces. The core of fastkqr is a finite smoothing algorithm that magically produces exact regression quantiles, rather than approximations. To further accelerate the algorithm, we equip fastkqr with a novel spectral technique that carefully reutilizes matrix computations. In addition, we extend fastkqr to accommodate a flexible kernel quantile regression with a data-driven crossing penalty, addressing the interpretability challenges of crossing quantile curves at multiple levels. We have implemented fastkqr in a publicly available R package. Extensive simulations and real applications show that fastkqr matches the accuracy of state-of-the-art algorithms but can operate up to an order of magnitude faster.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0