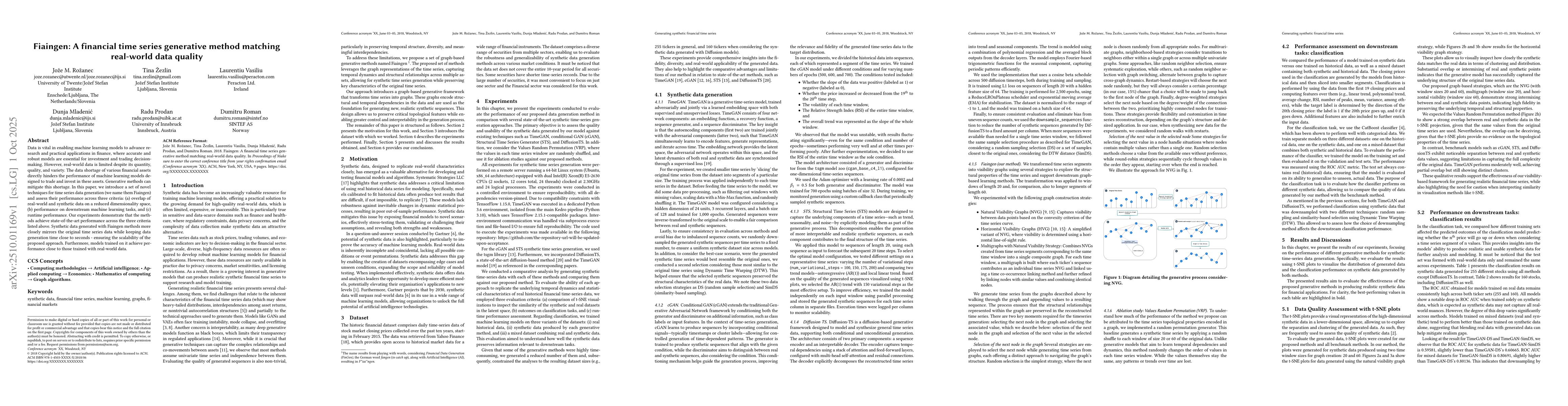

Data is vital in enabling machine learning models to advance research and

practical applications in finance, where accurate and robust models are

essential for investment and trading decision-making. However, real-world data

is limited despite its quantity, quality, and variety. The data shortage of

various financial assets directly hinders the performance of machine learning

models designed to trade and invest in these assets. Generative methods can

mitigate this shortage. In this paper, we introduce a set of novel techniques

for time series data generation (we name them Fiaingen) and assess their

performance across three criteria: (a) overlap of real-world and synthetic data

on a reduced dimensionality space, (b) performance on downstream machine

learning tasks, and (c) runtime performance. Our experiments demonstrate that

the methods achieve state-of-the-art performance across the three criteria

listed above. Synthetic data generated with Fiaingen methods more closely

mirrors the original time series data while keeping data generation time close

to seconds - ensuring the scalability of the proposed approach. Furthermore,

models trained on it achieve performance close to those trained with real-world

data.

Discussion 0