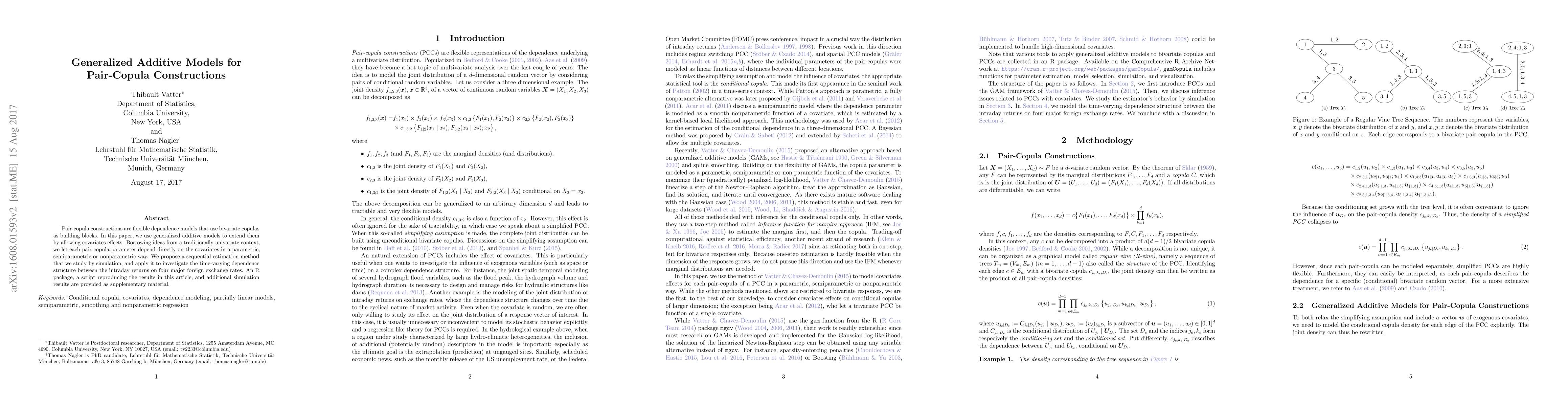

Generalized Additive Models for Pair-Copula Constructions

Publication

Metrics

AI Quick Summary

This paper extends pair-copula constructions using generalized additive models to incorporate covariate effects, proposing a sequential estimation method and applying it to analyze time-varying dependence in intraday foreign exchange returns. Supplementary material includes an R package and additional simulation results.

Paper Preview

Abstract

Pair-copula constructions are flexible dependence models that use bivariate copulas as building blocks. In this paper, we use generalized additive models to extend them by allowing covariates effects. Borrowing ideas from a traditionally univariate context, we let each pair-copula parameter depend directly on the covariates in a parametric, semiparametric or nonparametric way. We propose a sequential estimation method that we study by simulation, and apply it to investigate the time-varying dependence structure between the intraday returns on four major foreign exchange rates. An R package, a script reproducing the results in this article, and additional simulation results are provided as supplementary material.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0