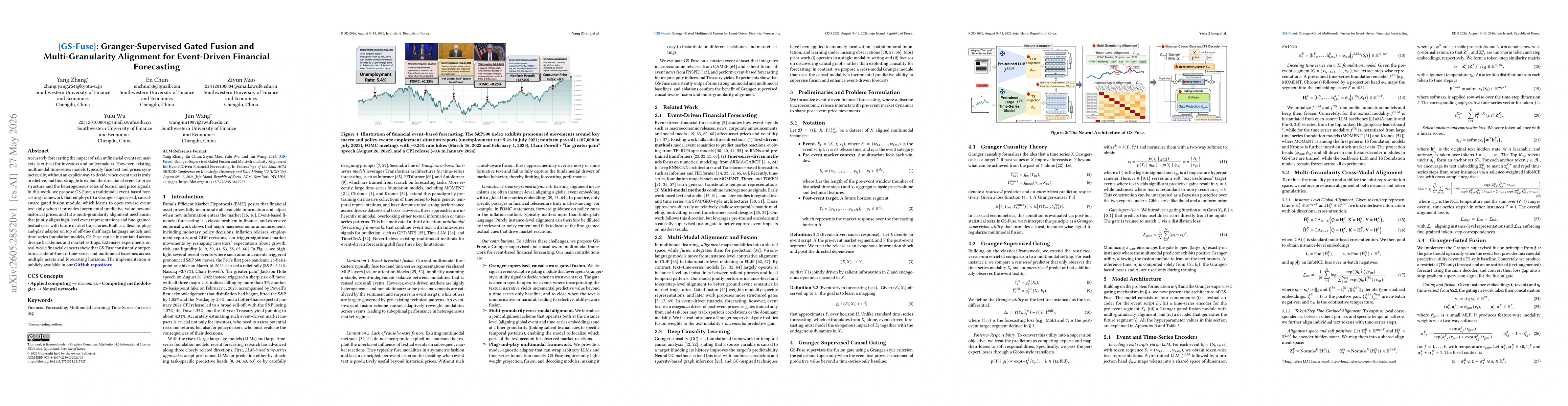

Accurately forecasting the impact of salient financial events on markets is critical for investors and policymakers. However, existing multimodal time-series models typically fuse text and prices symmetrically, without an explicit way to decide when event text is truly predictive, and thus struggle to exploit the directional event-to-price structure and the heterogeneous roles of textual and price signals. In this work, we propose GS-Fuse, a multimodal event-based forecasting framework that employs (i) a Granger-supervised, causal-aware gated fusion module, which learns to open toward event text only when it provides incremental predictive value beyond historical prices, and (ii) a multi-granularity alignment mechanism that jointly aligns high-level event representations and fine-grained textual cues with future market trajectories. Built as a flexible, plug-and-play adapter on top of off-the-shelf large language models and time-series foundation models, GS-Fuse can be instantiated across diverse backbones and market settings. Extensive experiments on real-world financial datasets show that GS-Fuse consistently outperforms state-of-the-art time-series and multimodal baselines across multiple assets and forecasting horizons.

Discussion 0