Stock movement prediction remains fundamentally challenging due to complex

temporal dependencies, heterogeneous modalities, and dynamically evolving

inter-stock relationships. Existing approaches often fail to unify structural,

semantic, and regime-adaptive modeling within a scalable framework. This work

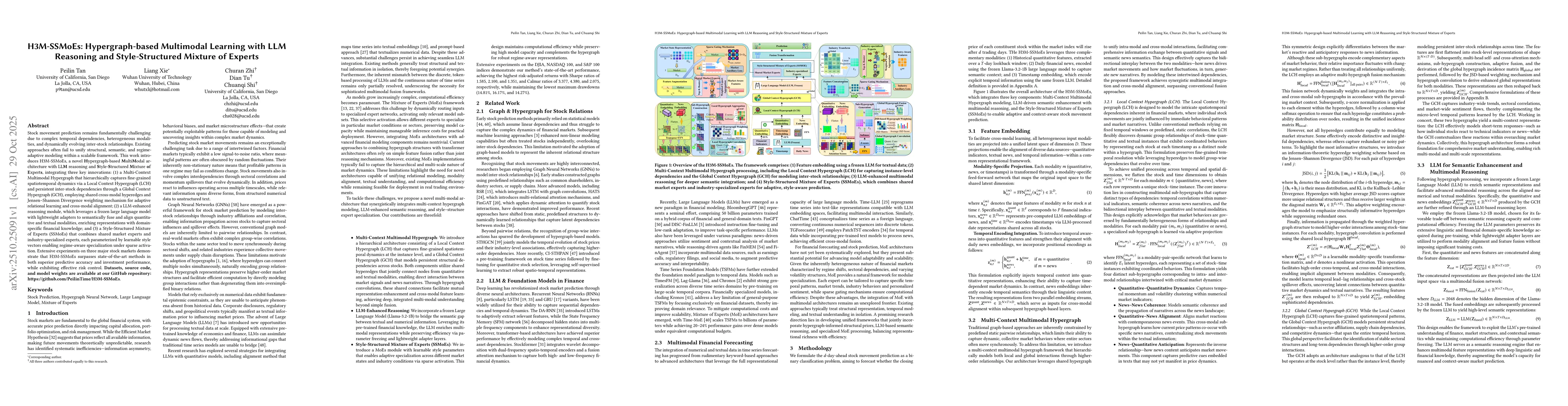

introduces H3M-SSMoEs, a novel Hypergraph-based MultiModal architecture with

LLM reasoning and Style-Structured Mixture of Experts, integrating three key

innovations: (1) a Multi-Context Multimodal Hypergraph that hierarchically

captures fine-grained spatiotemporal dynamics via a Local Context Hypergraph

(LCH) and persistent inter-stock dependencies through a Global Context

Hypergraph (GCH), employing shared cross-modal hyperedges and Jensen-Shannon

Divergence weighting mechanism for adaptive relational learning and cross-modal

alignment; (2) a LLM-enhanced reasoning module, which leverages a frozen large

language model with lightweight adapters to semantically fuse and align

quantitative and textual modalities, enriching representations with

domain-specific financial knowledge; and (3) a Style-Structured Mixture of

Experts (SSMoEs) that combines shared market experts and industry-specialized

experts, each parameterized by learnable style vectors enabling regime-aware

specialization under sparse activation. Extensive experiments on three major

stock markets demonstrate that H3M-SSMoEs surpasses state-of-the-art methods in

both superior predictive accuracy and investment performance, while exhibiting

effective risk control. Datasets, source code, and model weights are available

at our GitHub repository: https://github.com/PeilinTime/H3M-SSMoEs.

Discussion 0