Understanding how market participants react to shocks like scheduled

macroeconomic news is crucial for both traders and policymakers. We develop a

calibrated data generation process DGP that embeds four stylized trader

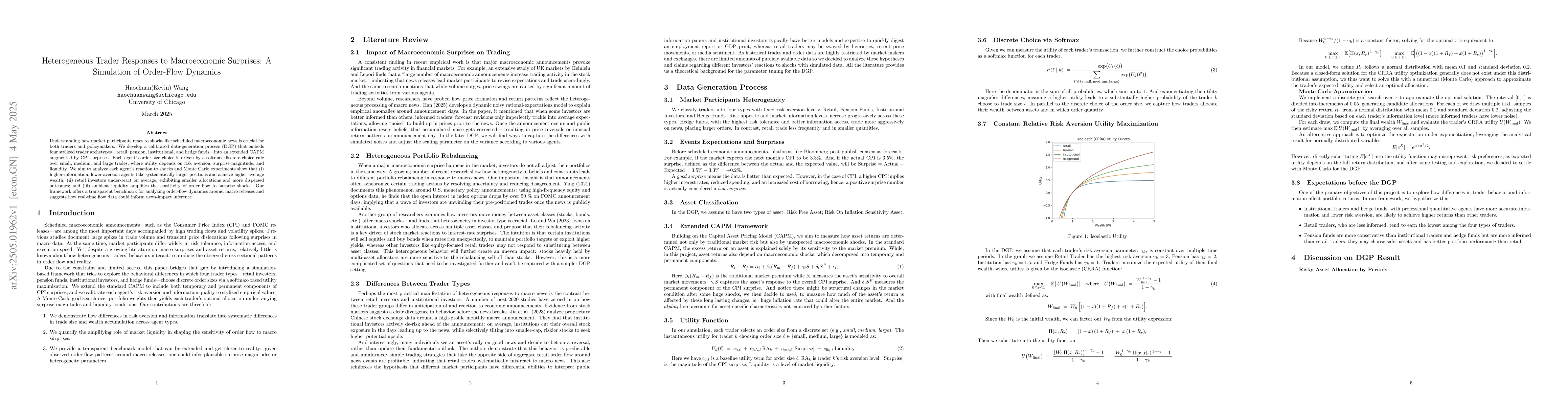

archetypes retail, pension, institutional, and hedge funds into an extended

CAPM augmented by CPI surprises. Each agents order size choice is driven by a

softmax discrete choice rule over small, medium, and large trades, where

utility depends on risk aversion, surprise magnitude, and liquidity. We aim to

analyze each agent's reaction to shocks and Monte Carlo experiments show that

higher information, lower aversion agents take systematically larger positions

and achieve higher average wealth. Retail investors under react on average,

exhibiting smaller allocations and more dispersed outcomes. And ambient

liquidity amplifies the sensitivity of order flow to surprise shocks. Our

framework offers a transparent benchmark for analyzing order flow dynamics

around macro releases and suggests how real time flow data could inform news

impact inference.

Discussion 0