Publication

Metrics

Paper Preview

Abstract

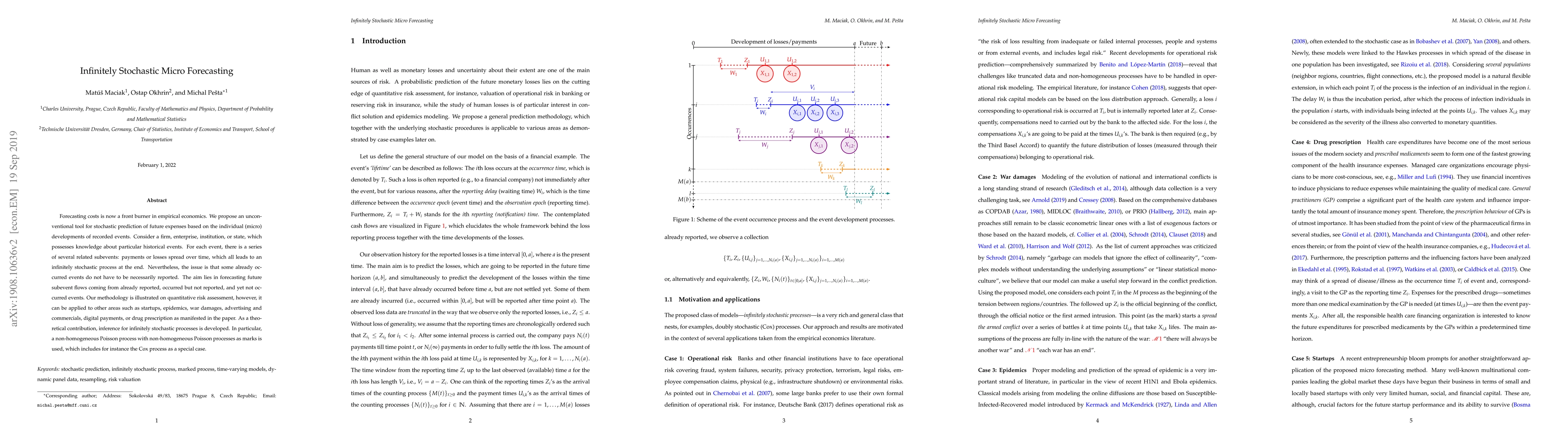

Forecasting costs is now a front burner in empirical economics. We propose an unconventional tool for stochastic prediction of future expenses based on the individual (micro) developments of recorded events. Consider a firm, enterprise, institution, or state, which possesses knowledge about particular historical events. For each event, there is a series of several related subevents: payments or losses spread over time, which all leads to an infinitely stochastic process at the end. Nevertheless, the issue is that some already occurred events do not have to be necessarily reported. The aim lies in forecasting future subevent flows coming from already reported, occurred but not reported, and yet not occurred events. Our methodology is illustrated on quantitative risk assessment, however, it can be applied to other areas such as startups, epidemics, war damages, advertising and commercials, digital payments, or drug prescription as manifested in the paper. As a theoretical contribution, inference for infinitely stochastic processes is developed. In particular, a non-homogeneous Poisson process with non-homogeneous Poisson processes as marks is used, which includes for instance the Cox process as a special case.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0