Publication

Metrics

AI Quick Summary

This paper introduces DAG-TFRC, a new method for learning directed acyclic graphs from time-series data generated by few root causes. It outperforms existing methods in accuracy and scalability, successfully identifying instantaneous and time-lagged dependencies, and root cause locations and times in both synthetic and financial datasets.

Paper Preview

Abstract

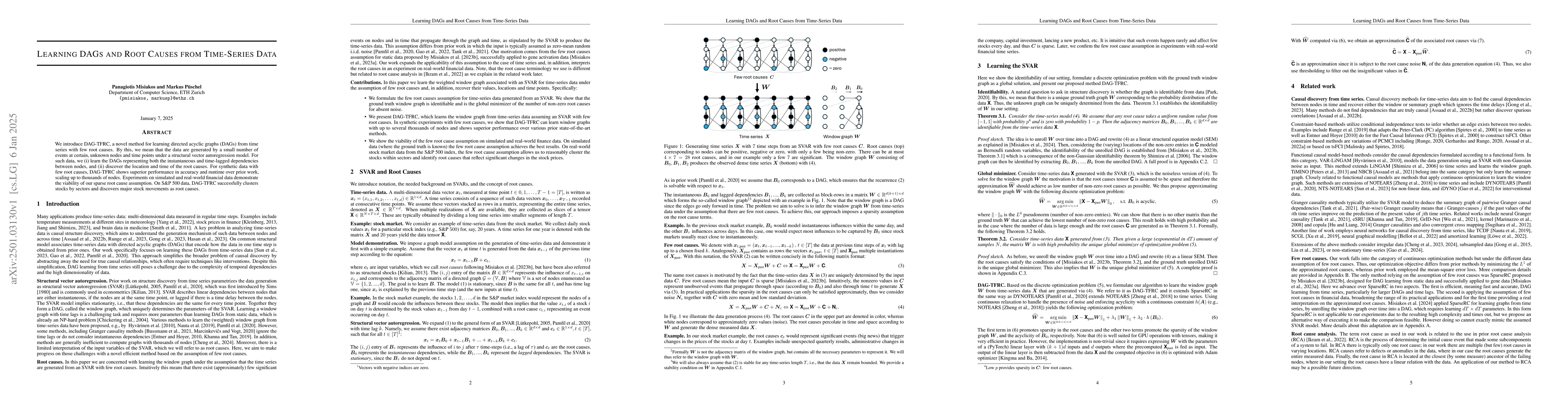

We introduce DAG-TFRC, a novel method for learning directed acyclic graphs (DAGs) from time series with few root causes. By this, we mean that the data are generated by a small number of events at certain, unknown nodes and time points under a structural vector autoregression model. For such data, we (i) learn the DAGs representing both the instantaneous and time-lagged dependencies between nodes, and (ii) discover the location and time of the root causes. For synthetic data with few root causes, DAG-TFRC shows superior performance in accuracy and runtime over prior work, scaling up to thousands of nodes. Experiments on simulated and real-world financial data demonstrate the viability of our sparse root cause assumption. On S&P 500 data, DAG-TFRC successfully clusters stocks by sectors and discovers major stock movements as root causes.

AI Key Findings — Processing

Key findings are being generated. Please check back in a few minutes.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0