Machine learning memory kernels as closure for non-Markovian stochastic processes

Publication

Metrics

AI Quick Summary

This paper proposes a machine learning approach, combining multilayer perceptrons with the generalized Langevin equation, to model non-Markovian stochastic processes. This method effectively addresses the challenges of inaccessible historical data and complex system dynamics, demonstrating successful application across various fields.

Paper Preview

Abstract

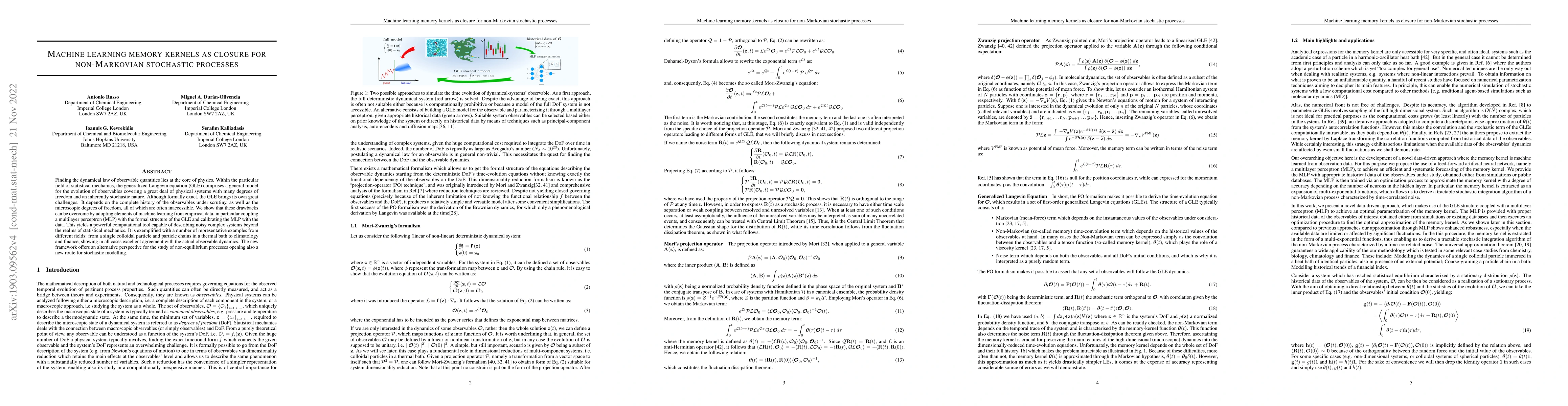

Finding the dynamical law of observable quantities lies at the core of physics. Within the particular field of statistical mechanics, the generalized Langevin equation (GLE) comprises a general model for the evolution of observables covering a great deal of physical systems with many degrees of freedom and an inherently stochastic nature. Although formally exact, the GLE brings its own great challenges. It depends on the complete history of the observables under scrutiny, as well as the microscopic degrees of freedom, all of which are often inaccessible. We show that these drawbacks can be overcome by adopting elements of machine learning from empirical data, in particular coupling a multilayer perceptron (MLP) with the formal structure of the GLE and calibrating the MLP with the data. This yields a powerful computational tool capable of describing noisy complex systems beyond the realms of statistical mechanics. It is exemplified with a number of representative examples from different fields: from a single colloidal particle and particle chains in a thermal bath to climatology and finance, showing in all cases excellent agreement with the actual observable dynamics. The new framework offers an alternative perspective for the study of non-equilibrium processes opening also a new route for stochastic modelling.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0