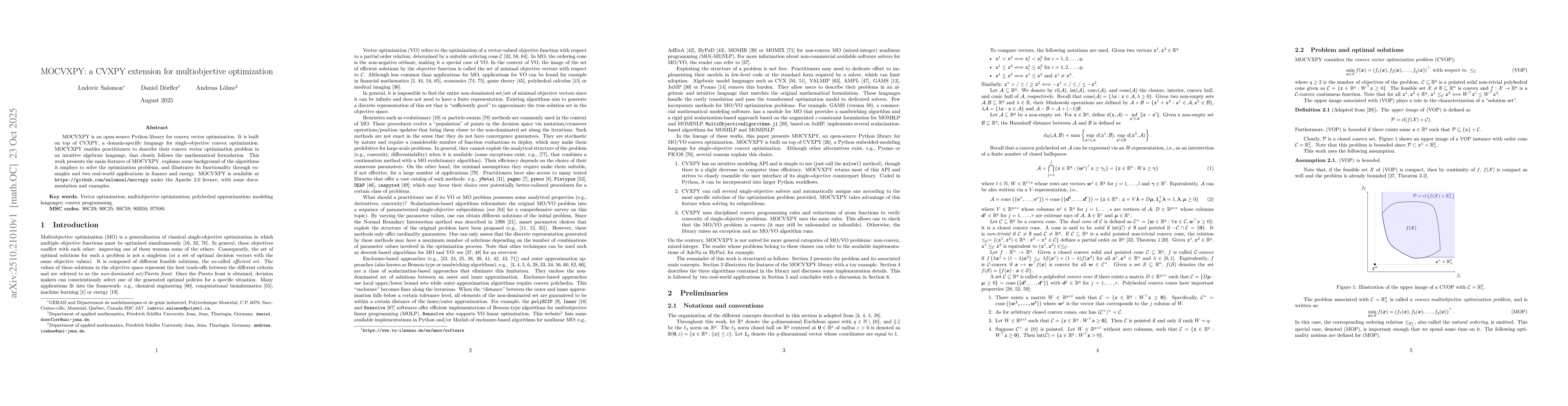

MOCVXPY is an open-source Python library for convex vector optimization. It

is built on top of CVXPY, a domain-specific language for single-objective

convex optimization. MOCVXPY enables practitioners to describe their convex

vector optimization problem in an intuitive algebraic language, that closely

follows the mathematical formulation. This work presents the main features of

MOCVXPY, explains some background of the algorithms it employs to solve the

optimization problems, and illustrates its functionality through examples and

two real-world applications in finance and energy. MOCVXPY is available at

https://github.com/salomonl/mocvxpy under the Apache 2.0 licence, with some

documentation and examples.

Discussion 0