Publication

Metrics

Paper Preview

Abstract

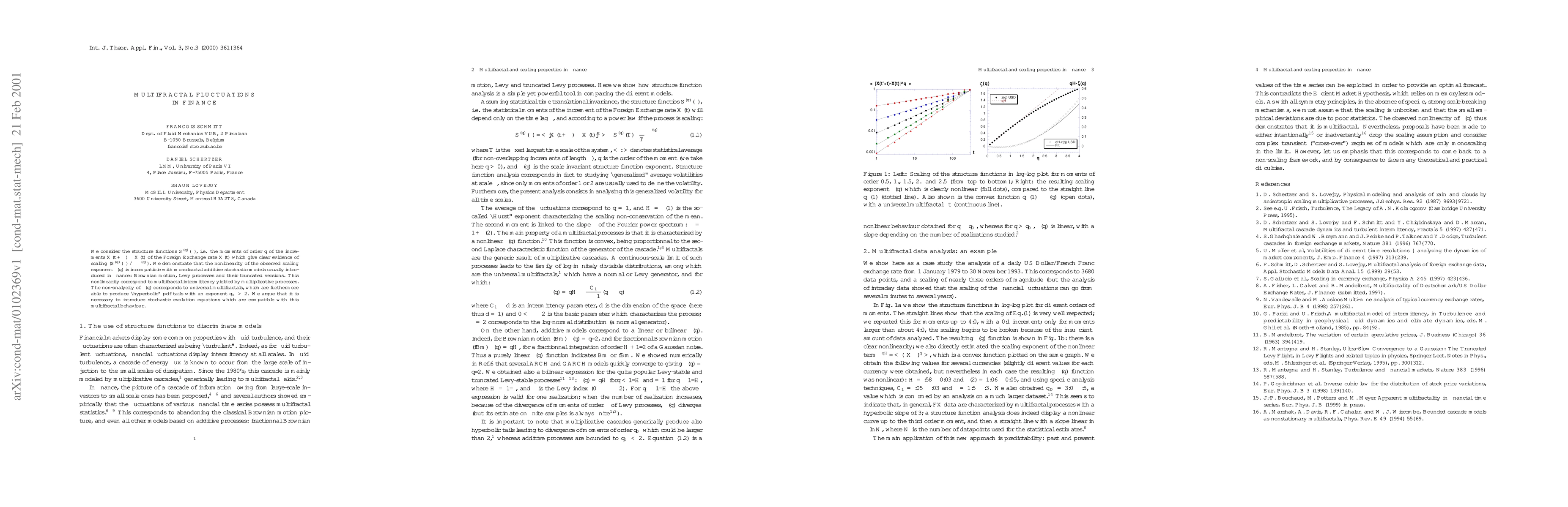

We consider the structure functions S^(q)(T), i.e. the moments of order q of the increments X(t+T)-X(t) of the Foreign Exchange rate X(t) which give clear evidence of scaling (S^(q)(T)~T^z(q)). We demonstrate that the nonlinearity of the observed scaling exponent z(q) is incompatible with monofractal additive stochastic models usually introduced in finance: Brownian motion, Levy processes and their truncated versions. This nonlinearity corresponds to multifractal intermittency yielded by multiplicative processes. The non-analycity of z(q) corresponds to universal multifractals, which are furthermore able to produce ``hyperbolic'' pdf tails with an exponent q_D >2. We argue that it is necessary to introduce stochastic evolution equations which are compatible with this multifractal behaviour.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0