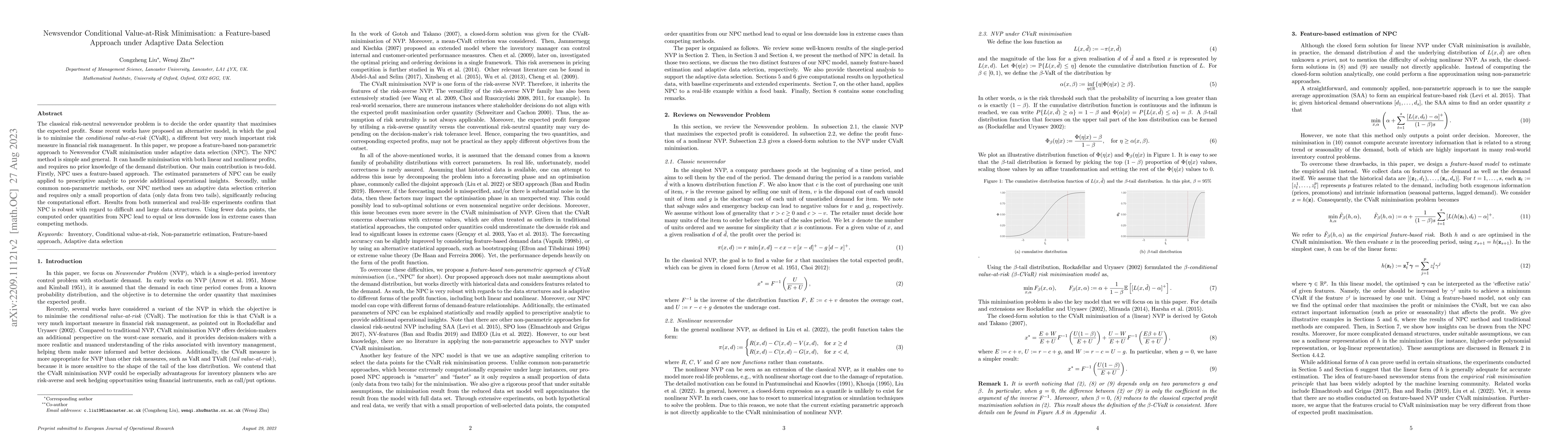

The classical risk-neutral newsvendor problem is to decide the order quantity

that maximises the expected profit. Some recent works have proposed an

alternative model, in which the goal is to minimise the conditional

value-at-risk (CVaR), a different but very much important risk measure in

financial risk management. In this paper, we propose a feature-based

non-parametric approach to Newsvendor CVaR minimisation under adaptive data

selection (NPC). The NPC method is simple and general. It can handle

minimisation with both linear and nonlinear profits, and requires no prior

knowledge of the demand distribution. Our main contribution is two-fold.

Firstly, NPC uses a feature-based approach. The estimated parameters of NPC can

be easily applied to prescriptive analytic to provide additional operational

insights. Secondly, unlike common non-parametric methods, our NPC method uses

an adaptive data selection criterion and requires only a small proportion of

data (only data from two tails), significantly reducing the computational

effort. Results from both numerical and real-life experiments confirm that NPC

is robust with regard to difficult and large data structures. Using fewer data

points, the computed order quantities from NPC lead to equal or less downside

loss in extreme cases than competing methods.

Discussion 0