01

MethodologyHow they did it

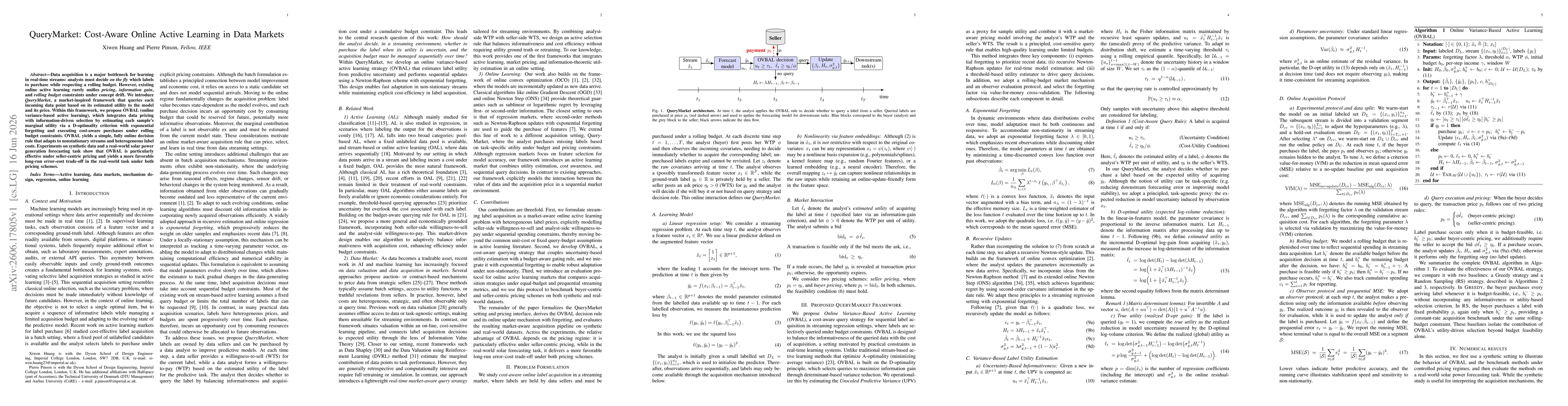

We formulate a market-aware, online active learning framework (QueryMarket) that, at each incoming data point, estimates the sample's marginal utility via a D-optimality criterion with exponential forgetting, and executes cost-aware purchases under a rolling budget. The OVBAL algorithm combines uncertainty-based utility estimation with a budget-aware gating rule and online Newton-style updates with forgetting to adapt to nonstationary streams. Experiments on synthetic data and a real-world solar forecasting task evaluate performance under buyer- and seller-centric pricing, focusing on long-run error-cost trade-offs.

Discussion 0