Selecting time-series hyperparameters with the artificial jackknife

Publication

Metrics

AI Quick Summary

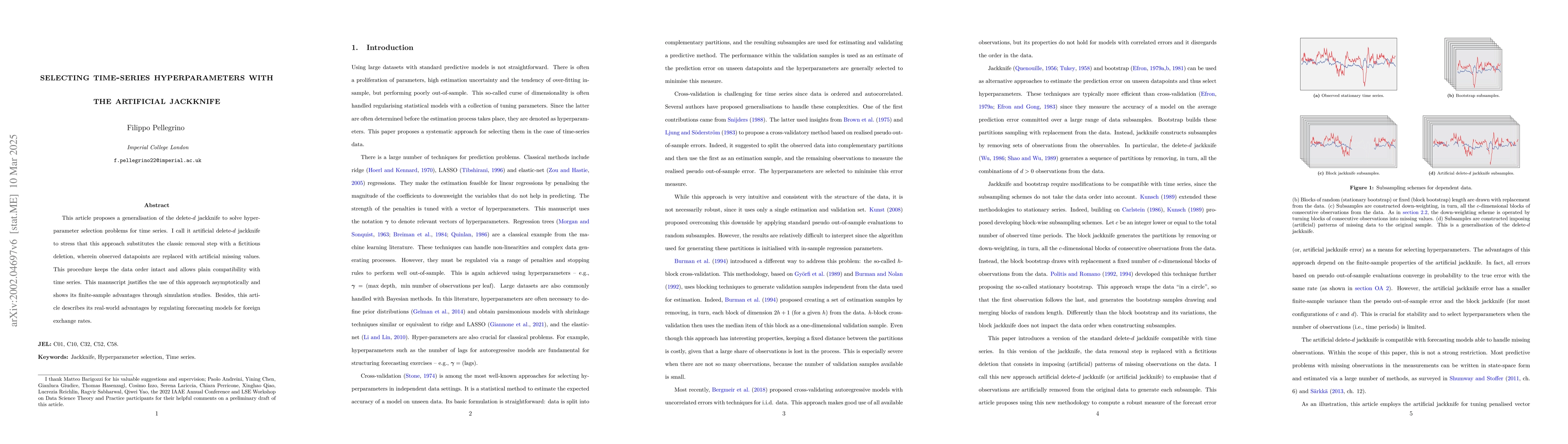

This paper introduces the artificial delete-$d$ jackknife, a method for hyperparameter selection in time-series models by replacing observed datapoints with artificial missing values, maintaining data order, and demonstrating its effectiveness through simulations and real-world applications in foreign exchange rate forecasting.

Paper Preview

Abstract

This article proposes a generalisation of the delete-$d$ jackknife to solve hyperparameter selection problems for time series. I call it artificial delete-$d$ jackknife to stress that this approach substitutes the classic removal step with a fictitious deletion, wherein observed datapoints are replaced with artificial missing values. This procedure keeps the data order intact and allows plain compatibility with time series. This manuscript justifies the use of this approach asymptotically and shows its finite-sample advantages through simulation studies. Besides, this article describes its real-world advantages by regulating high-dimensional forecasting models for foreign exchange rates.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0