01

MethodologyHow they did it

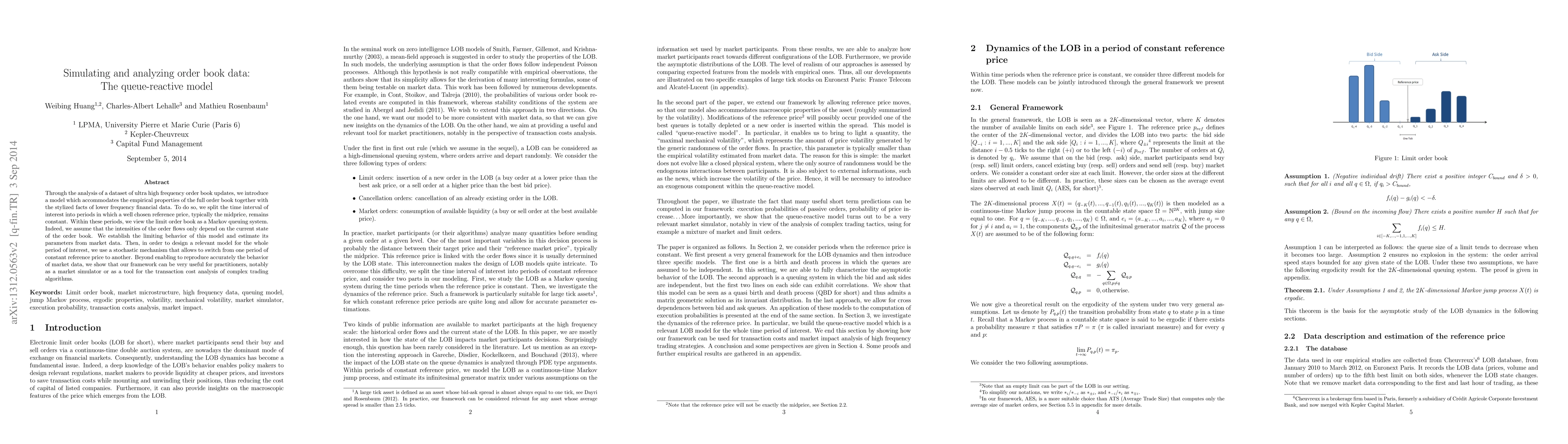

The research analyzes ultra-high-frequency order book updates, introducing a model that combines the empirical properties of the full order book with stylized facts of lower frequency financial data. It splits time intervals into periods with constant reference prices and models the limit order book as a Markov queuing system, where intensities of order flows depend on the current state of the order book. A stochastic mechanism allows for switches between periods of constant reference prices.

Discussion 0