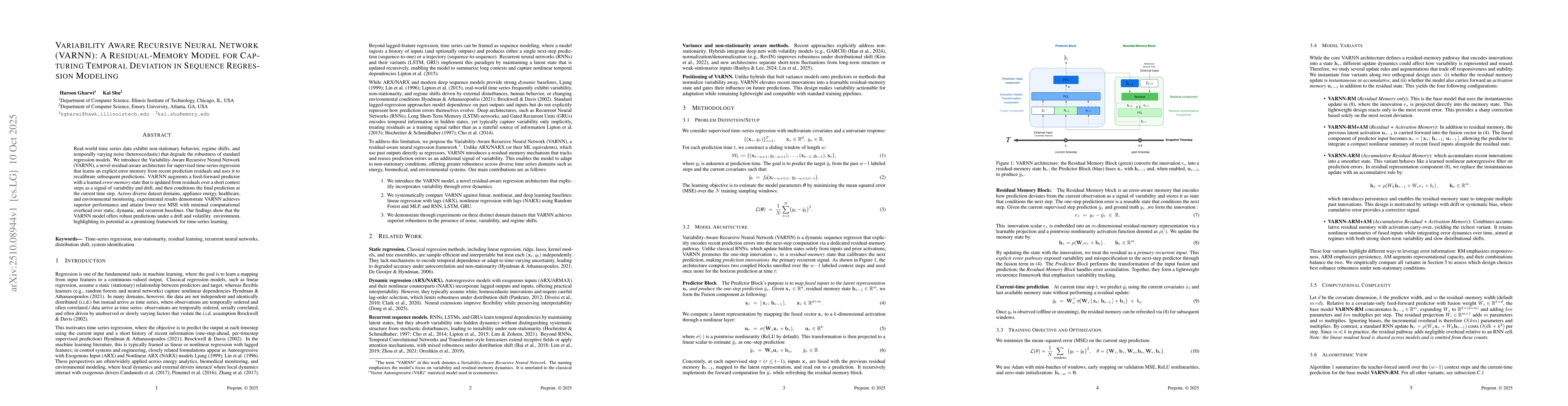

Real-world time series data exhibit non-stationary behavior, regime shifts,

and temporally varying noise (heteroscedastic) that degrade the robustness of

standard regression models. We introduce the Variability-Aware Recursive Neural

Network (VARNN), a novel residual-aware architecture for supervised time-series

regression that learns an explicit error memory from recent prediction

residuals and uses it to recalibrate subsequent predictions. VARNN augments a

feed-forward predictor with a learned error-memory state that is updated from

residuals over a short context steps as a signal of variability and drift, and

then conditions the final prediction at the current time step. Across diverse

dataset domains, appliance energy, healthcare, and environmental monitoring,

experimental results demonstrate VARNN achieves superior performance and

attains lower test MSE with minimal computational overhead over static,

dynamic, and recurrent baselines. Our findings show that the VARNN model offers

robust predictions under a drift and volatility environment, highlighting its

potential as a promising framework for time-series learning.

Discussion 0