Why is order flow so persistent?

Publication

Metrics

Paper Preview

Abstract

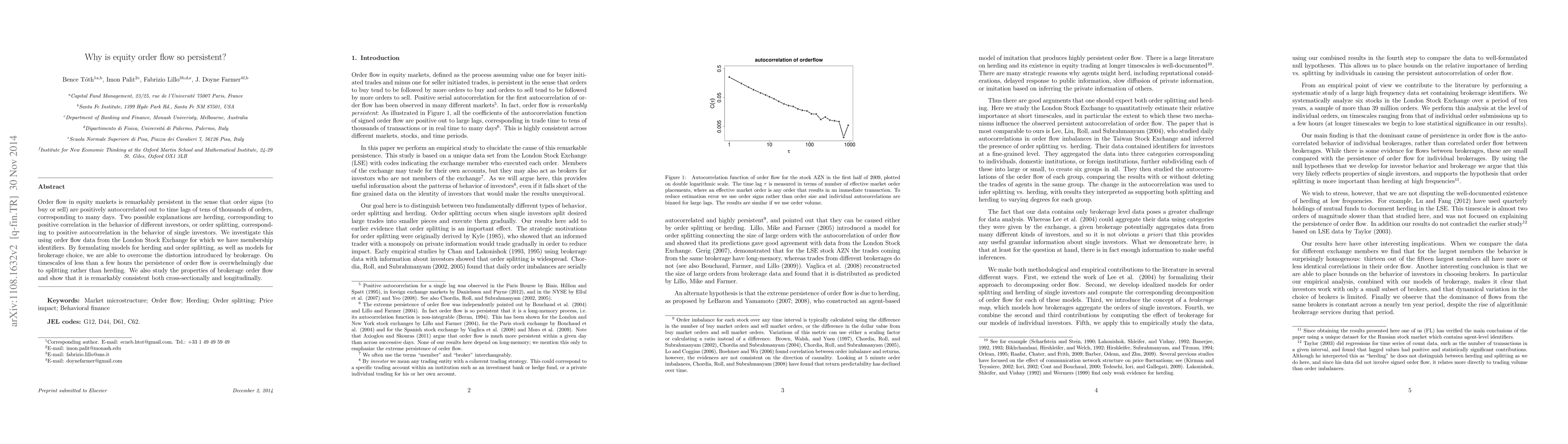

Order flow in equity markets is remarkably persistent in the sense that order signs (to buy or sell) are positively autocorrelated out to time lags of tens of thousands of orders, corresponding to many days. Two possible explanations are herding, corresponding to positive correlation in the behavior of different investors, or order splitting, corresponding to positive autocorrelation in the behavior of single investors. We investigate this using order flow data from the London Stock Exchange for which we have membership identifiers. By formulating models for herding and order splitting, as well as models for brokerage choice, we are able to overcome the distortion introduced by brokerage. On timescales of less than a few hours the persistence of order flow is overwhelmingly due to splitting rather than herding. We also study the properties of brokerage order flow and show that it is remarkably consistent both cross-sectionally and longitudinally.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0