Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we simulate the execution of a large stock order with real data and general power law in the Almgren and Chriss model. The example that we consider is the liquidation of a large posit...

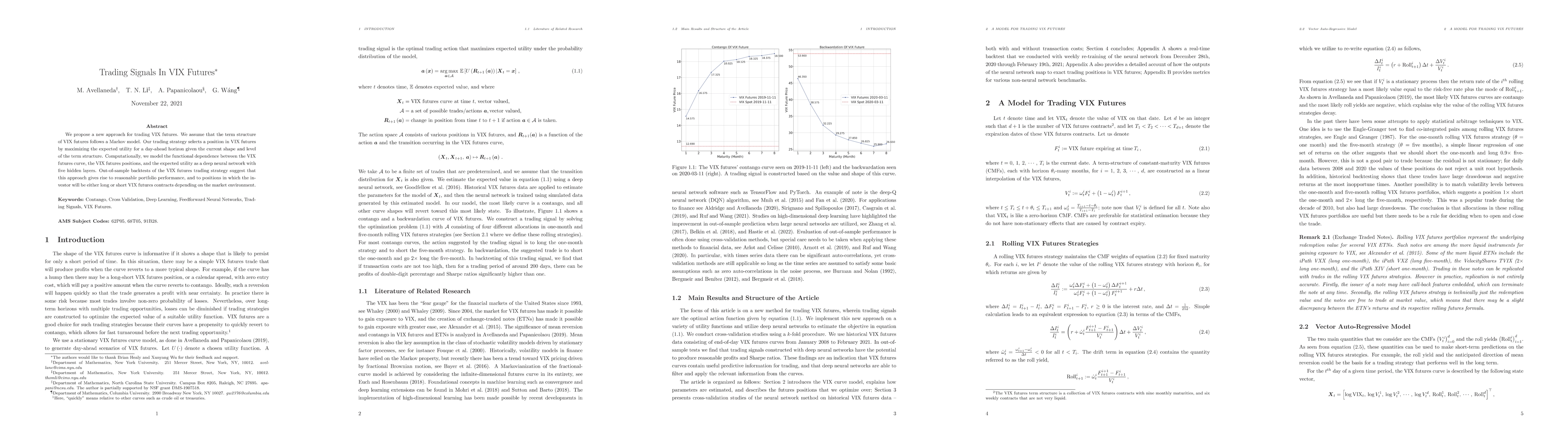

We propose a new approach for trading VIX futures. We assume that the term structure of VIX futures follows a Markov model. Our trading strategy selects a position in VIX futures by maximizing the e...

In this article, we analyse optimal statistical arbitrage strategies from stochastic control and optimisation problems for multiple co-integrated stocks with eigenportfolios being factors. Optimal p...