Academic Profile

Statistics

Similar Authors

Papers on arXiv

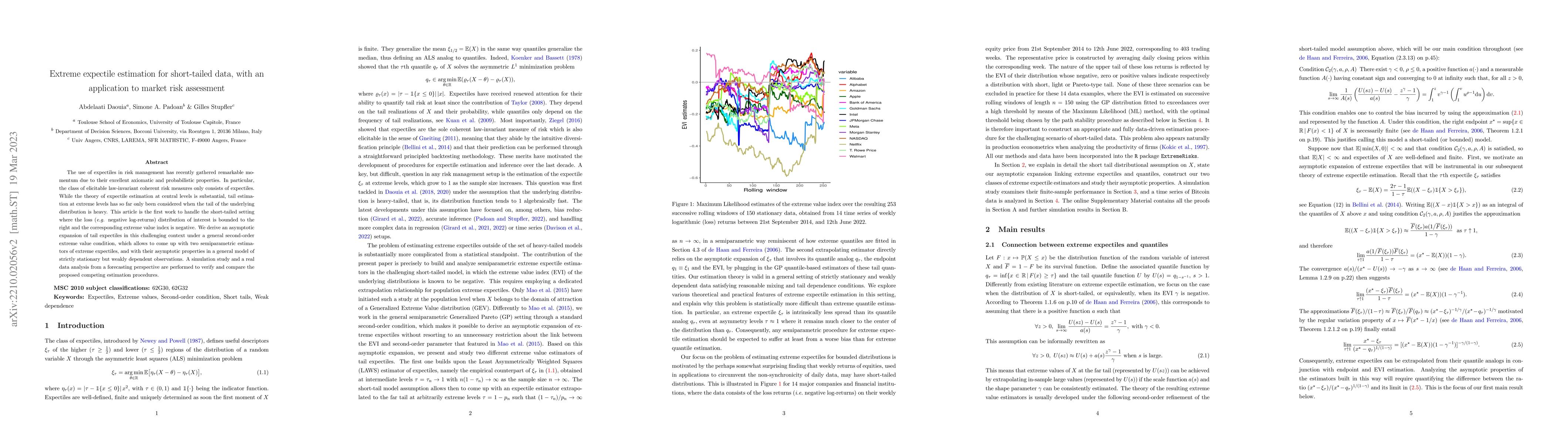

The use of expectiles in risk management has recently gathered remarkable momentum due to their excellent axiomatic and probabilistic properties. In particular, the class of elicitable law-invariant...

This paper investigates pooling strategies for tail index and extreme quantile estimation from heavy-tailed data. To fully exploit the information contained in several samples, we present general we...

Despite the renewed interest in the Newey and Powell (1987) concept of expectiles in fields such as econometrics, risk management, and extreme value theory, expectile regression---or, more generally...