Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we use the concept of excursion sets for the extrapolation of stationary random fields. Doing so, we define excursion sets for the field and its linear predictor, and then minimize th...

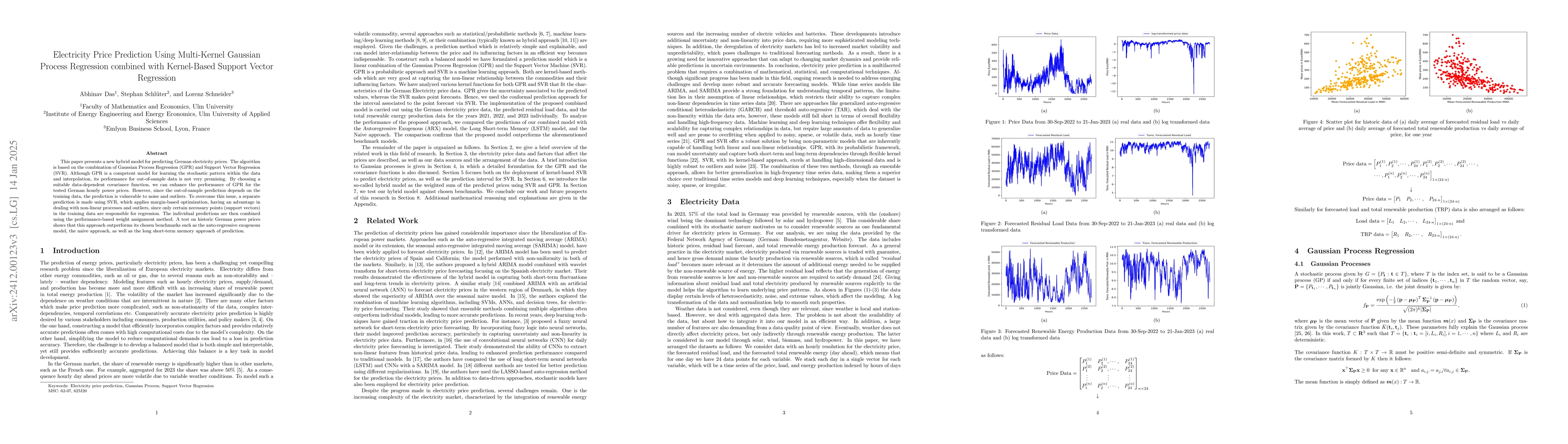

This paper presents a new hybrid model for predicting German electricity prices. The algorithm is based on combining Gaussian Process Regression (GPR) and Support Vector Regression (SVR). While GPR is...

Electricity storage is crucial for a successful transition towards carbon-neutral energy production. Despite considerable research and a number of promising future alternatives such as hydrogen, batte...

This work integrates Bayesian regime detection with conditional neural processes for 24-hour electricity price prediction in the German market. Our methodology integrates regime detection using a dise...

Precise probabilistic forecasts are fundamental for energy risk management, and there is a wide range of both statistical and machine learning models for this purpose. Inherent to these probabilistic ...

Accurate electricity price forecasting is critical for strategic decision-making in deregulated electricity markets, where volatility stems from complex supply-demand dynamics and external factors. Tr...