Academic Profile

Statistics

Similar Authors

Papers on arXiv

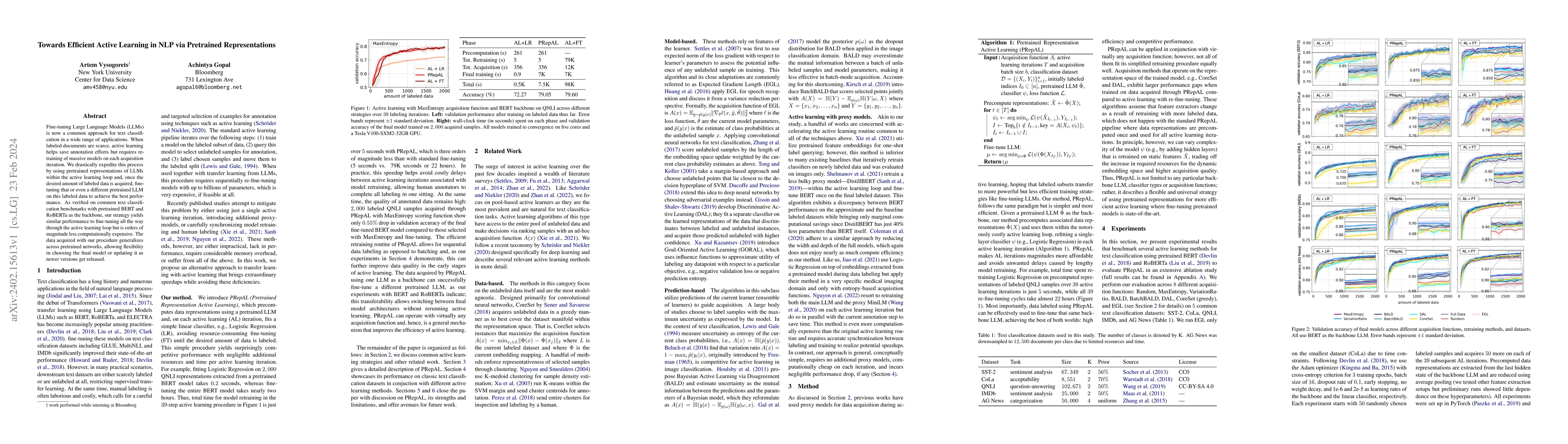

Fine-tuning Large Language Models (LLMs) is now a common approach for text classification in a wide range of applications. When labeled documents are scarce, active learning helps save annotation ef...

This paper introduces a new causal structure learning method for nonstationary time series data, a common data type found in fields such as finance, economics, healthcare, and environmental science....

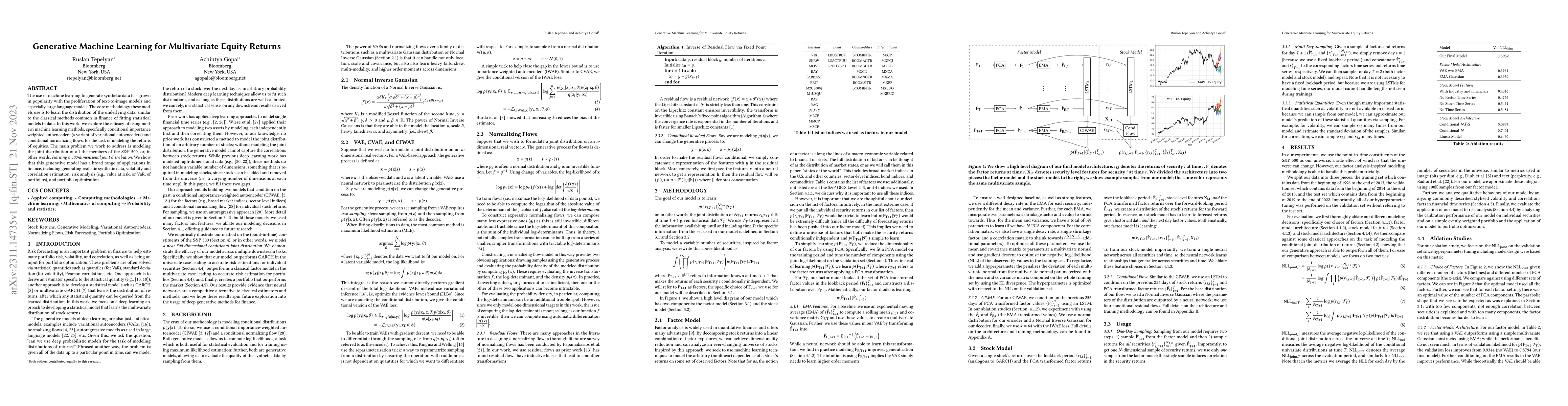

The use of machine learning to generate synthetic data has grown in popularity with the proliferation of text-to-image models and especially large language models. The core methodology these models ...

The generation of synthetic tabular data that preserves differential privacy is a problem of growing importance. While traditional marginal-based methods have achieved impressive results, recent wor...

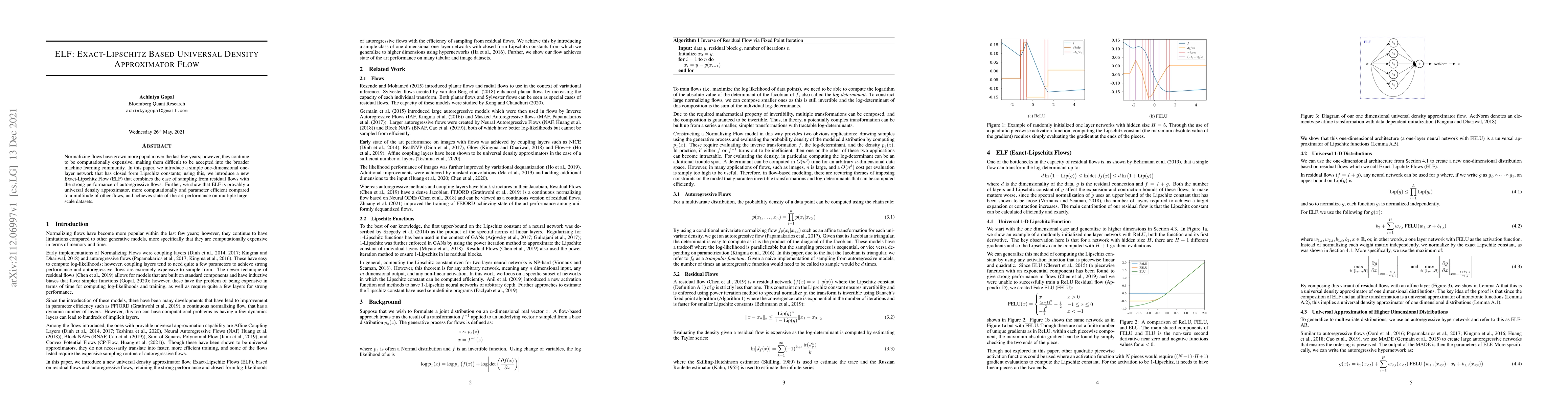

Normalizing flows have grown more popular over the last few years; however, they continue to be computationally expensive, making them difficult to be accepted into the broader machine learning comm...

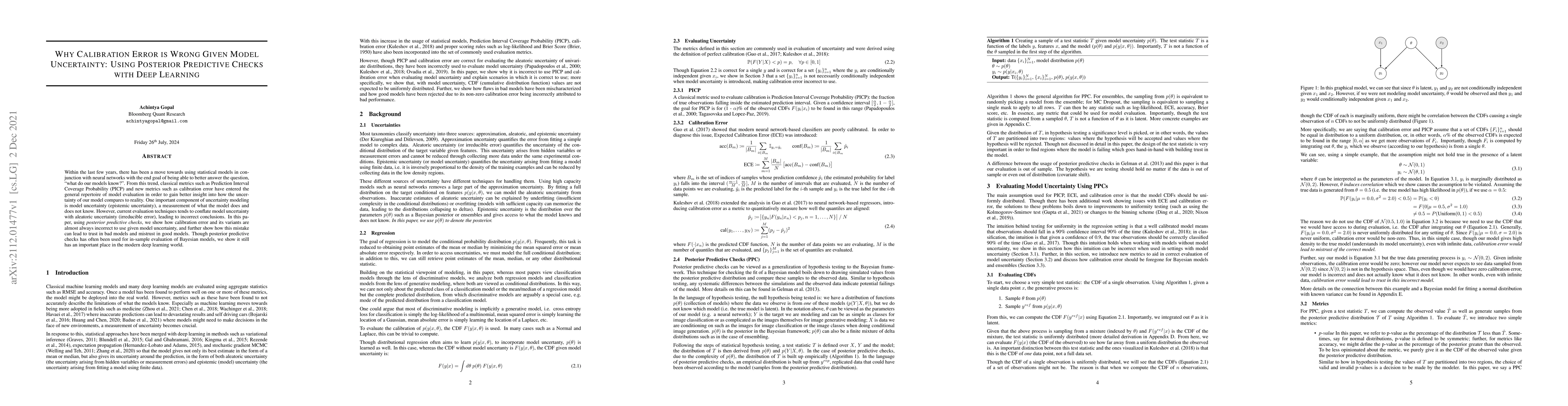

Within the last few years, there has been a move towards using statistical models in conjunction with neural networks with the end goal of being able to better answer the question, "what do our mode...

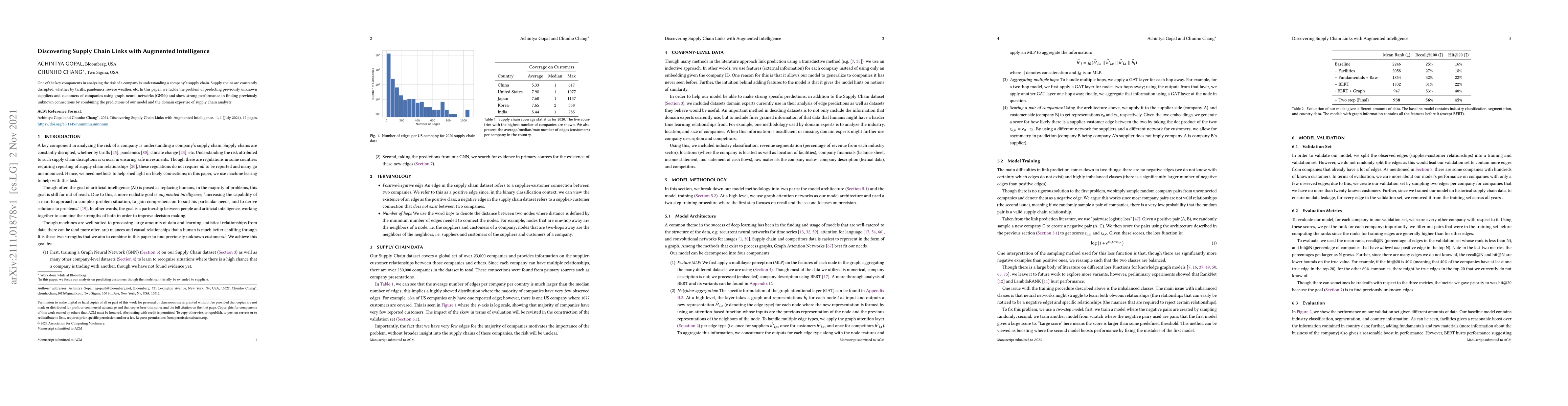

One of the key components in analyzing the risk of a company is understanding a company's supply chain. Supply chains are constantly disrupted, whether by tariffs, pandemics, severe weather, etc. In...

As an important step to fulfill the Paris Agreement and achieve net-zero emissions by 2050, the European Commission adopted the most ambitious package of climate impact measures in April 2021 to imp...

Normalizing Flows are a powerful technique for learning and modeling probability distributions given samples from those distributions. The current state of the art results are built upon residual fl...

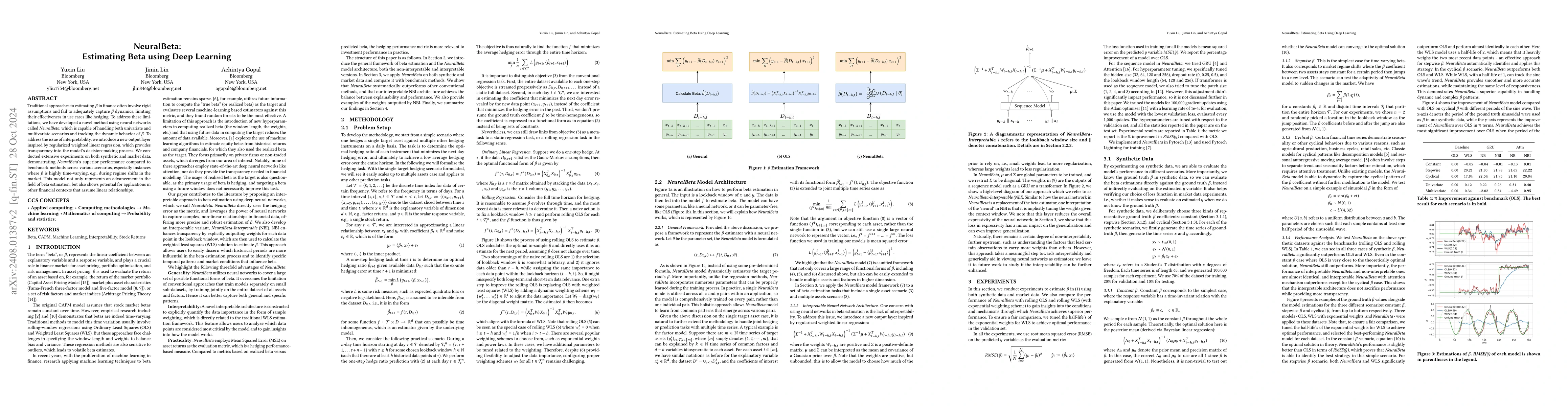

Traditional approaches to estimating beta in finance often involve rigid assumptions and fail to adequately capture beta dynamics, limiting their effectiveness in use cases like hedging. To address th...

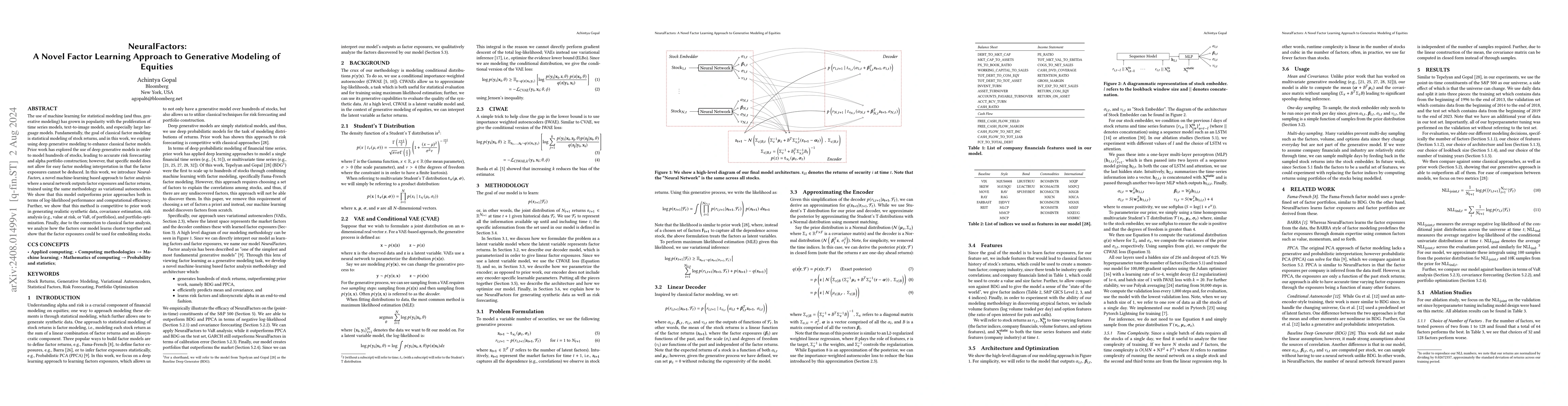

The use of machine learning for statistical modeling (and thus, generative modeling) has grown in popularity with the proliferation of time series models, text-to-image models, and especially large la...

Missing data is a common problem in finance and often requires methods to fill in the gaps, or in other words, imputation. In this work, we focused on the imputation of missing implied volatilities fo...

Time-series data is a vital modality within data science communities. This is particularly valuable in financial applications, where it helps in detecting patterns, understanding market behavior, and ...

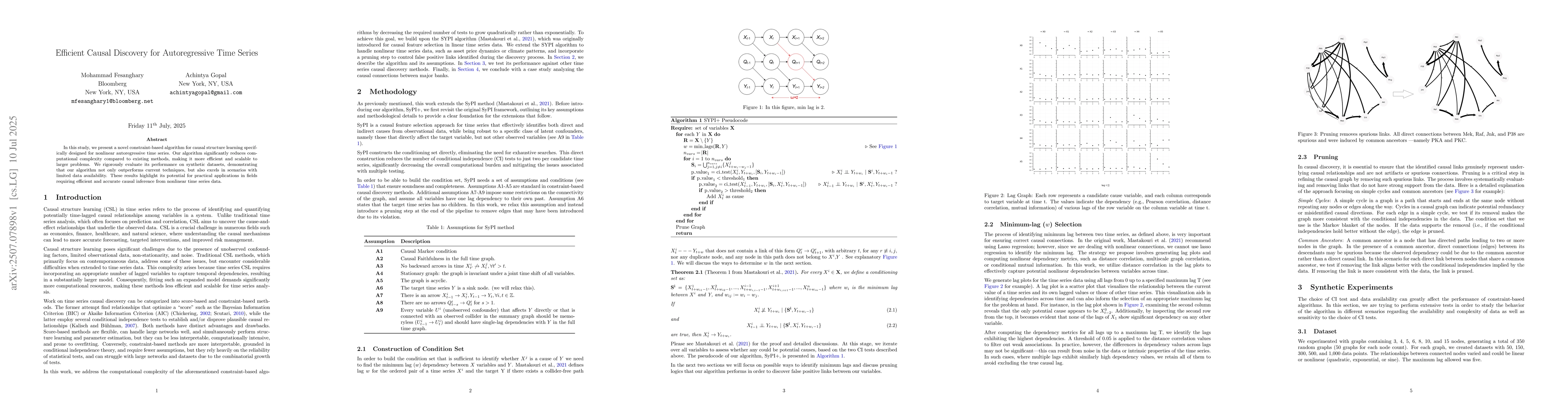

In this study, we present a novel constraint-based algorithm for causal structure learning specifically designed for nonlinear autoregressive time series. Our algorithm significantly reduces computati...