Academic Profile

Statistics

Similar Authors

Papers on arXiv

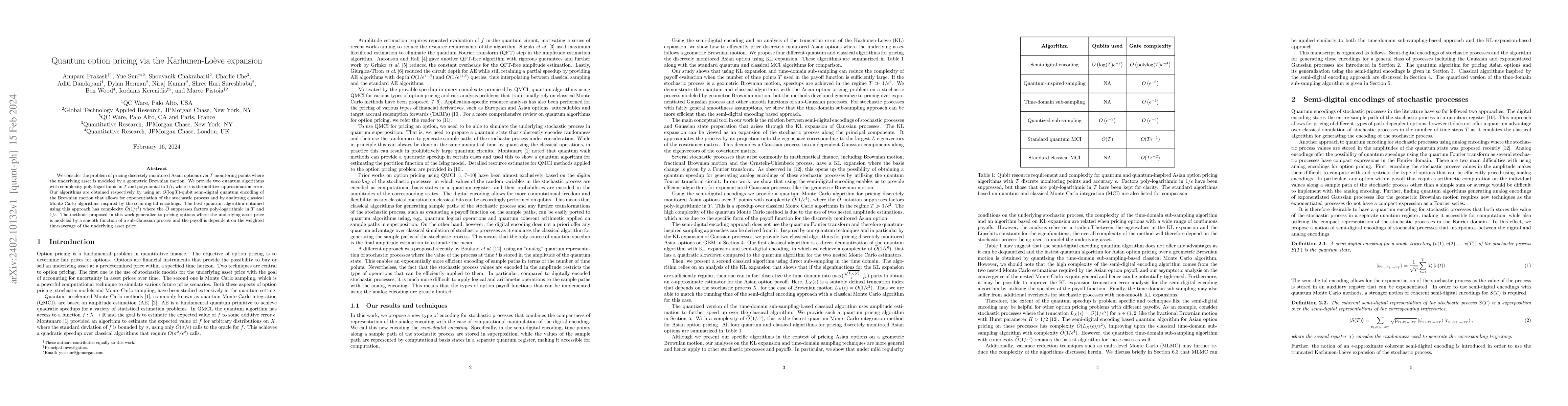

We consider the problem of pricing discretely monitored Asian options over $T$ monitoring points where the underlying asset is modeled by a geometric Brownian motion. We provide two quantum algorith...

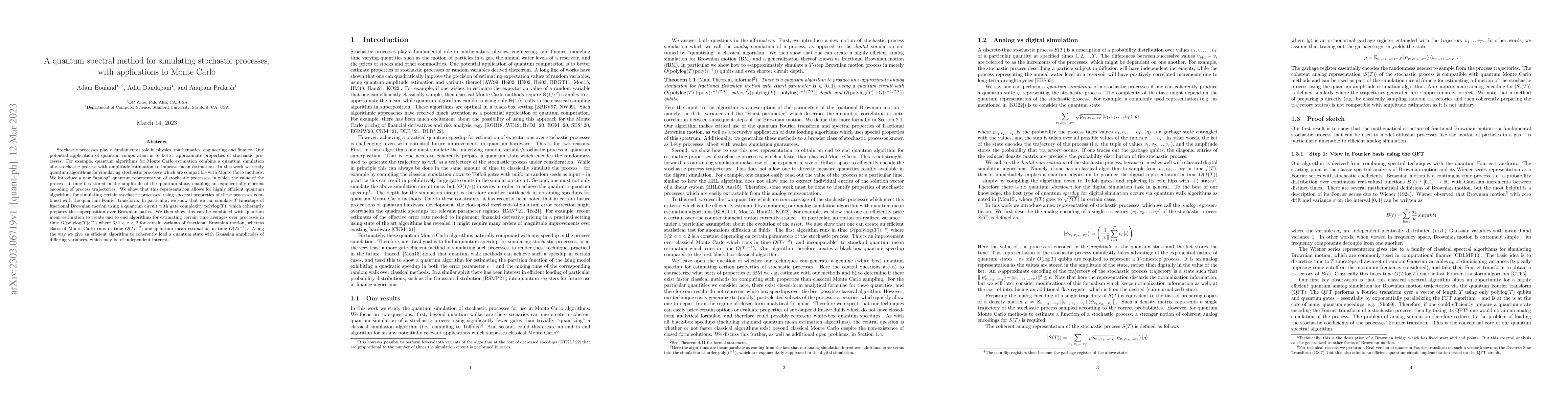

Stochastic processes play a fundamental role in physics, mathematics, engineering and finance. One potential application of quantum computation is to better approximate properties of stochastic proc...

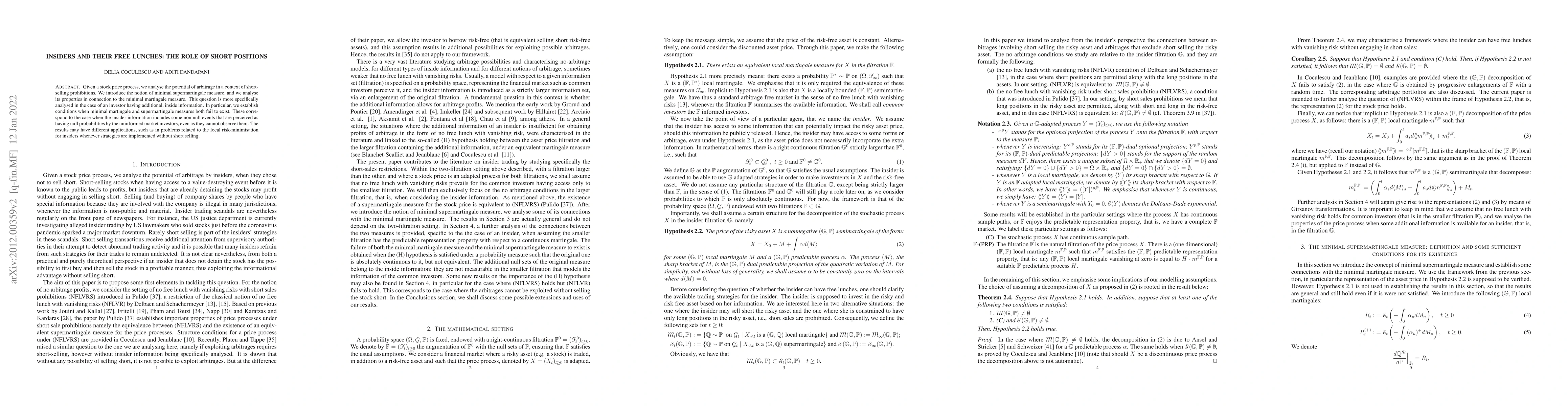

Given a stock price process, we analyse the potential of arbitrage by insiders in a context of short-selling prohibitions. We introduce the notion of minimal supermartingale measure, and we analyse ...

In a series of recent papers, Damiano Brigo, Andrea Pallavicini, and co-authors have shown that the value of a contract in a Credit Valuation Adjustment (CVA) setting, being the sum of the cash flow...