Academic Profile

Statistics

Similar Authors

Papers on arXiv

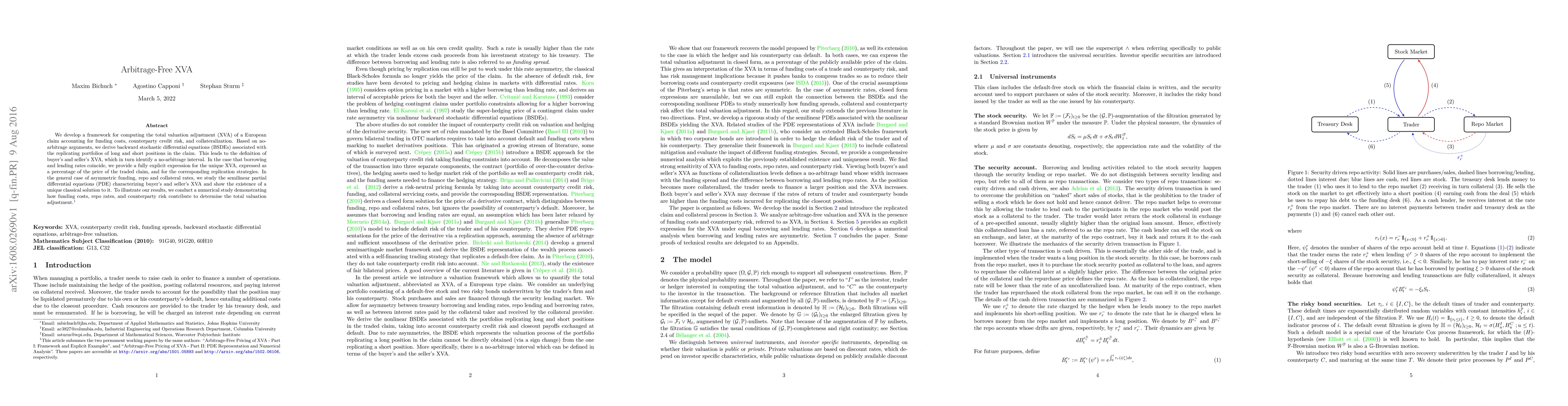

We develop a framework for computing the total valuation adjustment (XVA) of a European claim accounting for funding costs, counterparty credit risk, and collateralization. Based on no-arbitrage arg...

We study the completion of approximately low rank matrices with entries missing not at random (MNAR). In the context of typical large-dimensional statistical settings, we establish a framework for t...

Financial markets are undergoing an unprecedented transformation. Technological advances have brought major improvements to the operations of financial services. While these advances promote improve...

We study Just-in-time (JIT) liquidity provision in blockchain-based decentralized exchanges. A JIT liquidity provider (LP) monitors pending swap orders in public mempools of blockchains to sandwich ...

In this paper, we revisit and further explore a mathematically rigorous connection between Causal inference (C-inf) and the Low-rank recovery (LRR) established in [10]. Leveraging the Random duality...

In this paper we establish a mathematically rigorous connection between Causal inference (C-inf) and the low-rank recovery (LRR). Using Random Duality Theory (RDT) concepts developed in [46,48,50] a...

Transactions submitted through the blockchain peer-to-peer (P2P) network may leak out exploitable information. We study the economic incentives behind the adoption of blockchain dark venues, where u...

We study the forward investment performance process (FIPP) in an incomplete semimartingale market model with closed and convex portfolio constraints, when the investor's risk preferences are of the ...

Does the proof-of-work protocol serve its intended purpose of supporting decentralized cryptocurrency mining? To address this question, we develop a game-theoretical model where miners first invest ...

We investigate the market microstructure of Automated Market Makers (AMMs), the most prominent type of blockchain-based decentralized exchanges. We show that the order execution mechanism yields tok...

We provide an explicit characterization of the optimal market making strategy in a discrete-time Limit Order Book (LOB). In our model, the number of filled orders during each period depends linearly...

We propose a novel approach to infer investors' risk preferences from their portfolio choices, and then use the implied risk preferences to measure the efficiency of investment portfolios. We analyz...

We study the ex-ante minimization of market inefficiency, defined in terms of minimum deviation of market prices from fundamental values, from a centralized planner's perspective. Prices are pressur...

We study a class of sampled stochastic optimization problems, where the underlying state process has diffusive dynamics of the mean-field type. We establish the existence of optimal relaxed controls...

We introduce an arbitrage-free framework for robust valuation adjustments. An investor trades a credit default swap portfolio with a risky counterparty, and hedges credit risk by taking a position i...

Despite being an essential tool across engineering and finance, Monte Carlo simulation can be computationally intensive, especially in large-scale, path-dependent problems that hinder straightforward ...

We propose a data-driven dynamic factor framework where a response variable depends on a high-dimensional set of covariates, without imposing any parametric model on the joint dynamics. Leveraging Ani...

In the Day-Ahead (DA) market, suppliers sell and load-serving entities (LSEs) purchase energy commitments, with both sides adjusting for imbalances between contracted and actual deliveries in the Real...

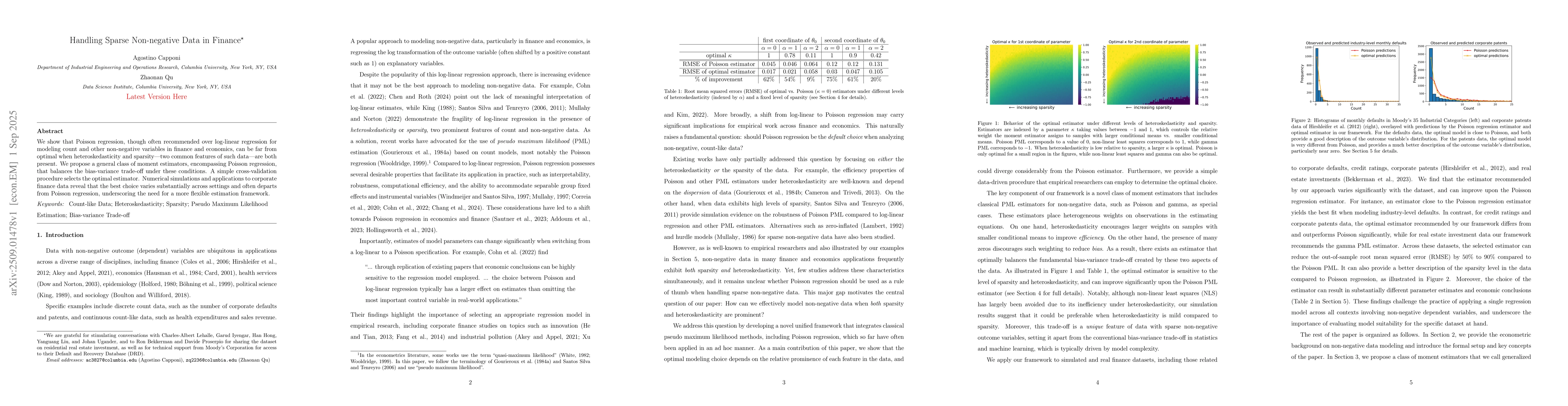

We show that Poisson regression, though often recommended over log-linear regression for modeling count and other non-negative variables in finance and economics, can be far from optimal when heterosk...

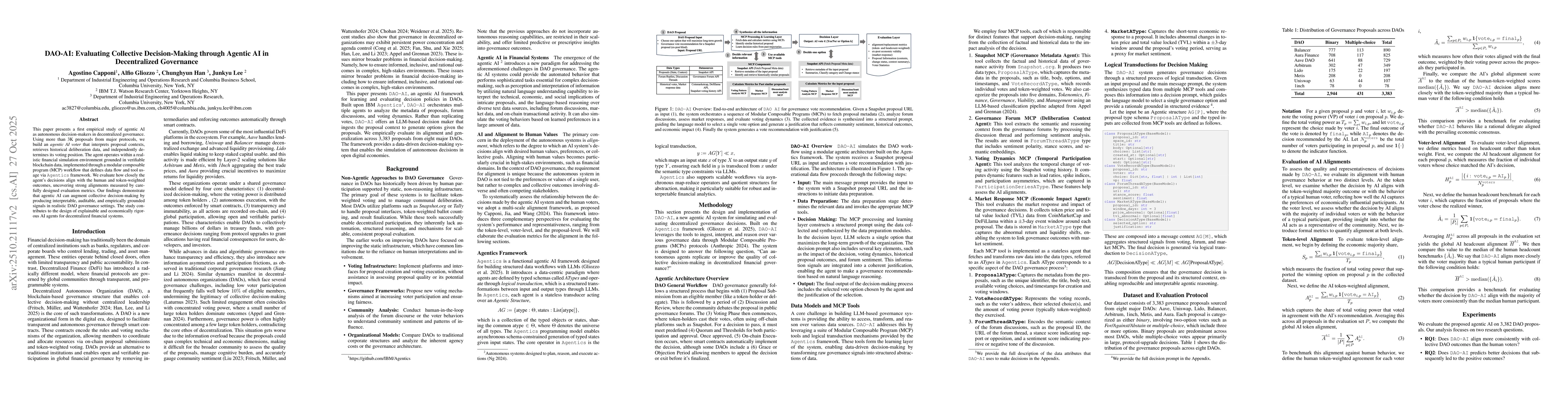

This paper presents a first empirical study of agentic AI as autonomous decision-makers in decentralized governance. Using more than 3K proposals from major protocols, we build an agentic AI voter tha...

Prediction markets allow users to trade on outcomes of real-world events, but are prone to fragmentation through overlapping questions, implicit equivalences, and hidden contradictions across markets....

Electricity markets are under increasing pressure to maintain reliability amidst rising renewable penetration, demand variability, and occasional price shocks. Traditional capacity market designs ofte...

We investigate machine learning models for stock return prediction in non-stationary environments, revealing a fundamental nonstationarity-complexity tradeoff: complex models reduce misspecification e...

Valuing corporate bonds in systemic economies is challenging due to intricate webs of inter-institutional exposures. When a bank defaults, cascading losses propagate through the network, with payments...

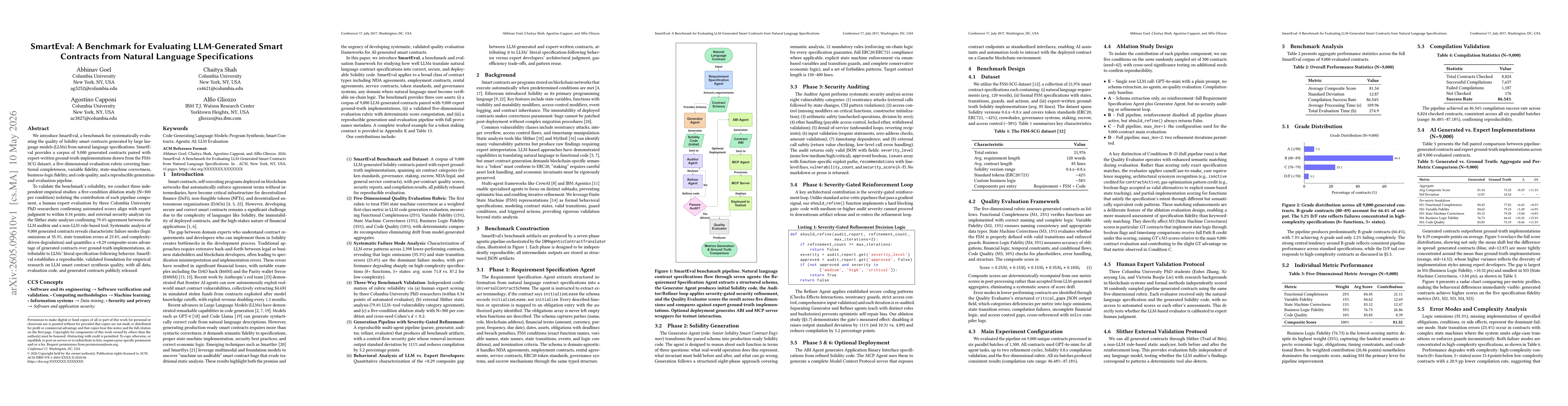

We present an end-to-end framework for systematic evaluation of LLM-generated smart contracts from natural-language specifications. The system parses contractual text into structured schemas, generate...

We introduce a new agentic artificial intelligence (AI) platform for portfolio management. Our architecture consists of three layers. First, two large language model (LLM) agents are assigned speciali...

Product reviews significantly influence purchasing decisions on e-commerce platforms. However, the sheer volume of reviews can overwhelm users, obscuring the information most relevant to their specifi...

We introduce SmartEval, a benchmark for systematically evaluating the quality of Solidity smart contracts generated by large language models (LLMs) from natural language specifications. SmartEval prov...

This paper develops a model to evaluate the viability of blockchain markets as the sole venue for price formation. Blockchains clear at discrete intervals called block time, and transactions are execu...

We argue that trustworthy AI agents, especially in high-stakes and policy-governed domains, should make execution conditional on certified traces rather than rely only on stronger generative models, o...

We study optimal portfolio choice for a household simultaneously managing a random-deadline goal, such as a medical emergency or job loss, and a fixed-deadline goal such as retirement or college tuiti...