Academic Profile

Statistics

Similar Authors

Papers on arXiv

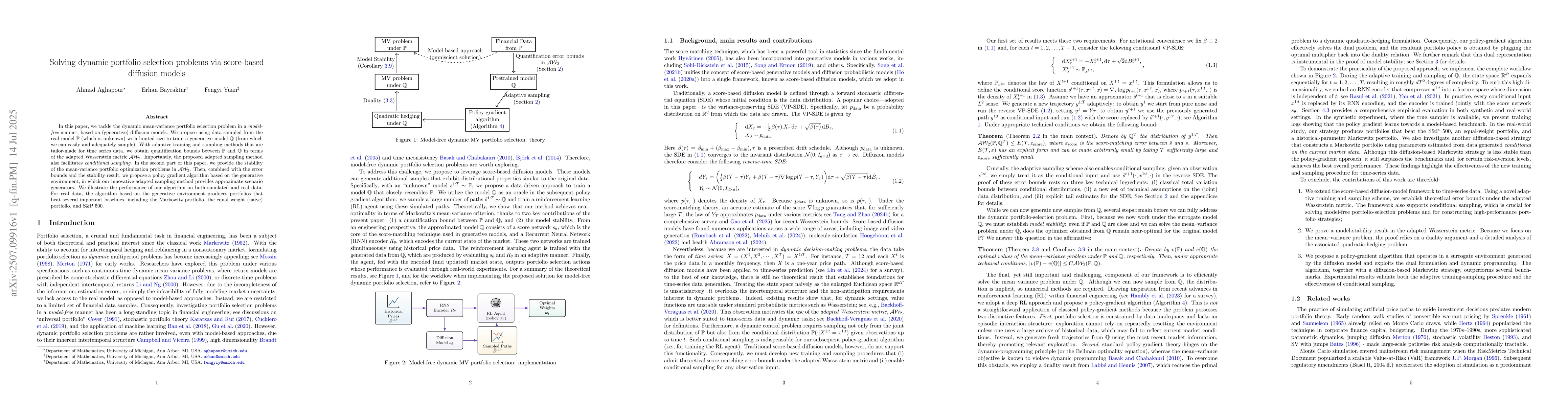

In this paper, we tackle the dynamic mean-variance portfolio selection problem in a {\it model-free} manner, based on (generative) diffusion models. We propose using data sampled from the real model $...

Diffusion generative models synthesize samples by discretizing reverse-time dynamics driven by a learned score (or denoiser). Existing convergence analyses of diffusion models typically scale at least...

We study zero-shot conditional sampling with pretrained diffusion models for linear inverse problems, including inpainting and super-resolution. In these problems, the observation determines only part...

Diffusion models perform remarkably well on high-dimensional data such as images, often using only a modest number of reverse-time steps. Despite this practical success, existing convergence theory do...