Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this note we re-examine the analysis of the paper "On the martingale property of stochastic exponentials" by B. Wong and C.C. Heyde, Journal of Applied Probability, 41(3):654-664, 2004. Some coun...

We provide a criterion for establishing lower bounds on the rate of convergence in $f$-variation of a continuous-time ergodic Markov process to its invariant measure. The criterion consists of novel...

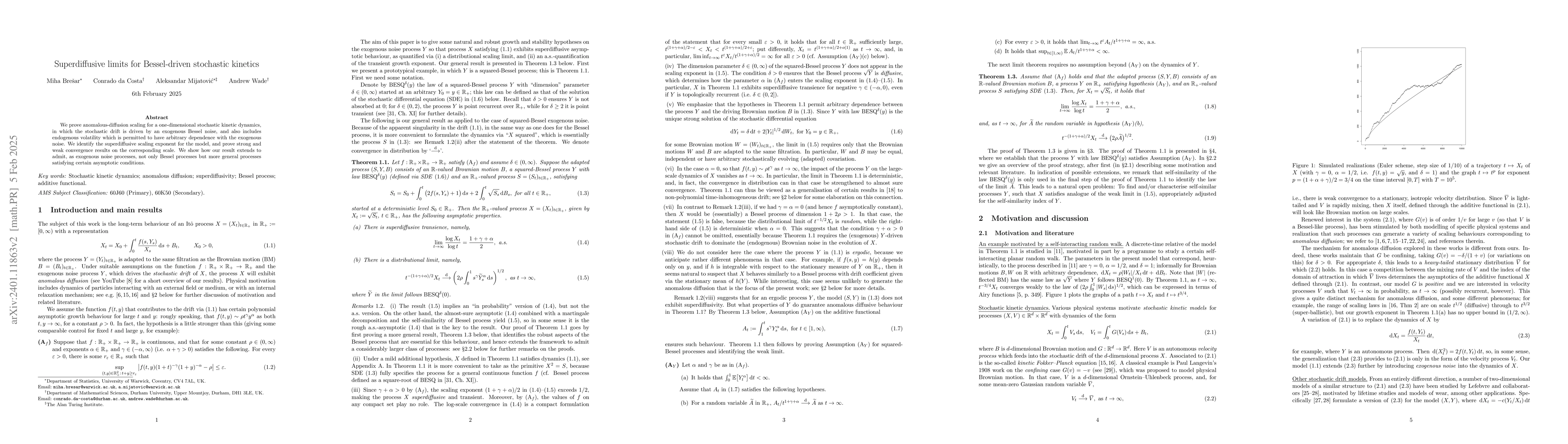

We prove anomalous-diffusion scaling for a one-dimensional stochastic kinetic dynamics, in which the stochastic drift is driven by an exogenous Bessel noise, and also includes endogenous volatility ...

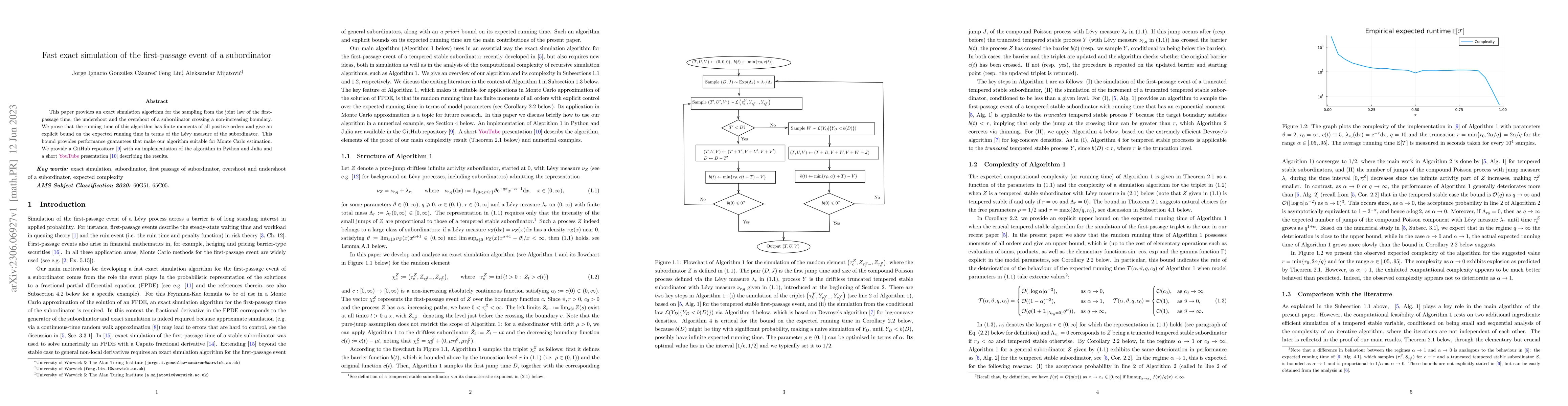

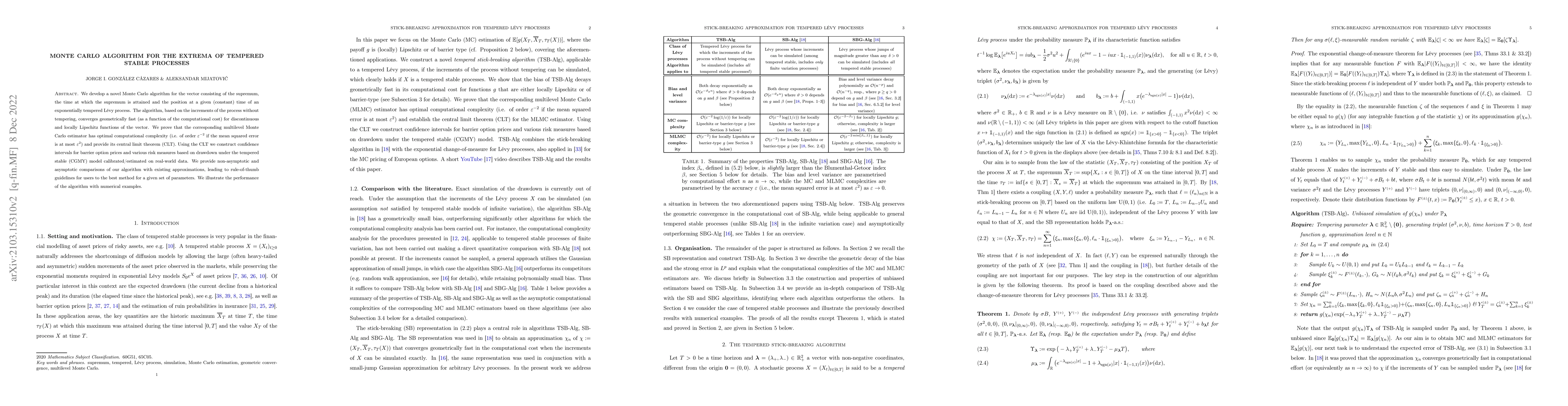

This paper provides an exact simulation algorithm for the sampling from the joint law of the first-passage time, the undershoot and the overshoot of a subordinator crossing a non-increasing boundary...

We construct a fast exact algorithm for the simulation of the first-passage time, jointly with the undershoot and overshoot, of a tempered stable subordinator over an arbitrary non-increasing absolu...

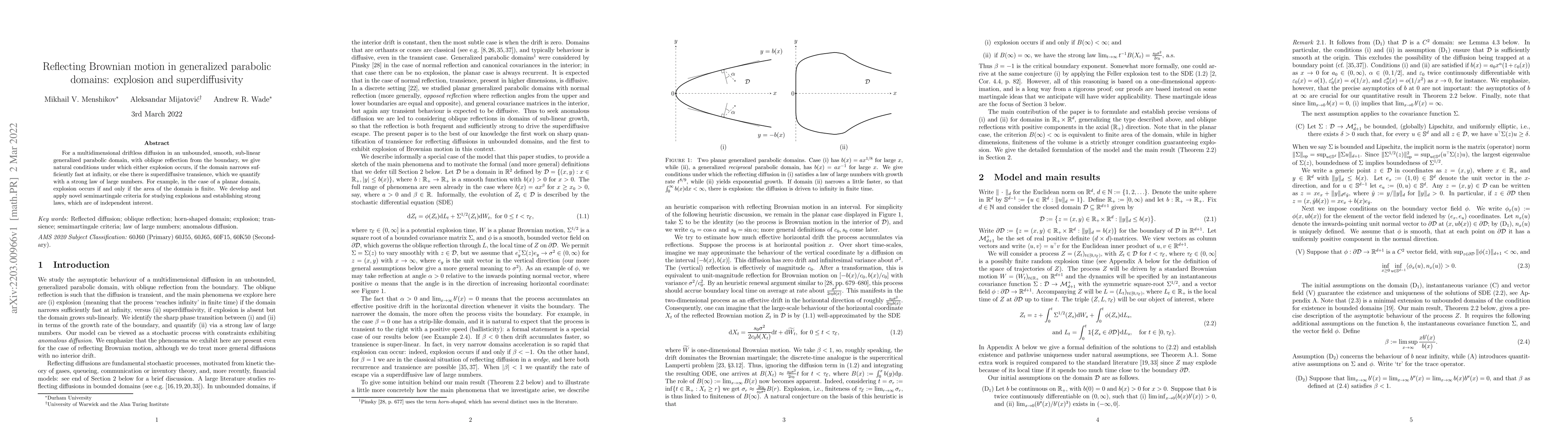

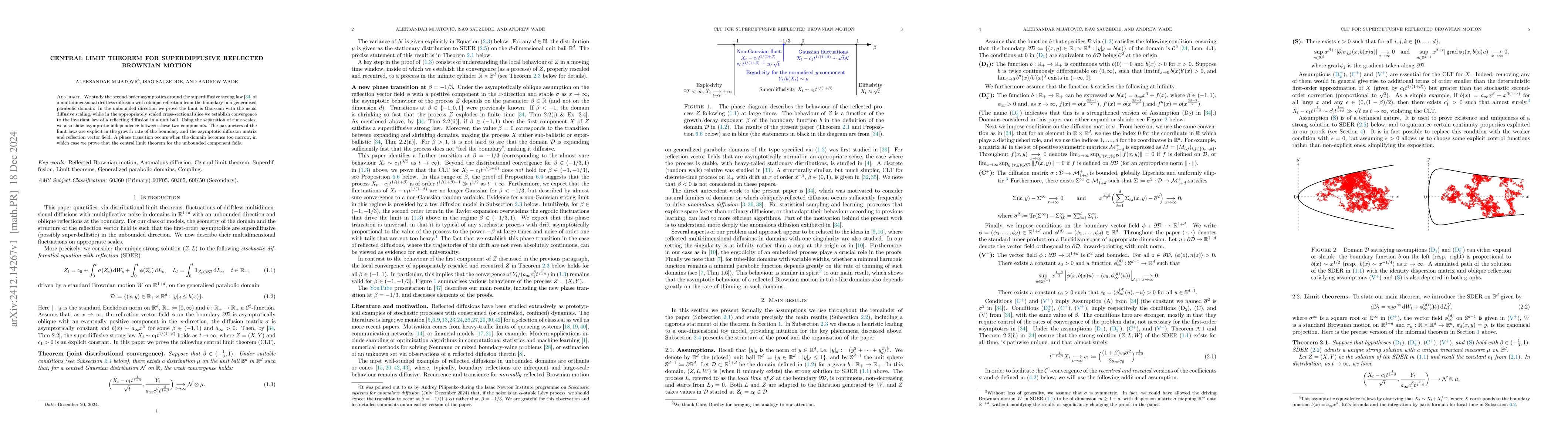

We quantify the asymptotic behaviour of multidimensional drifltess diffusions in domains unbounded in a single direction, with asymptotically normal reflections from the boundary. We identify the cr...

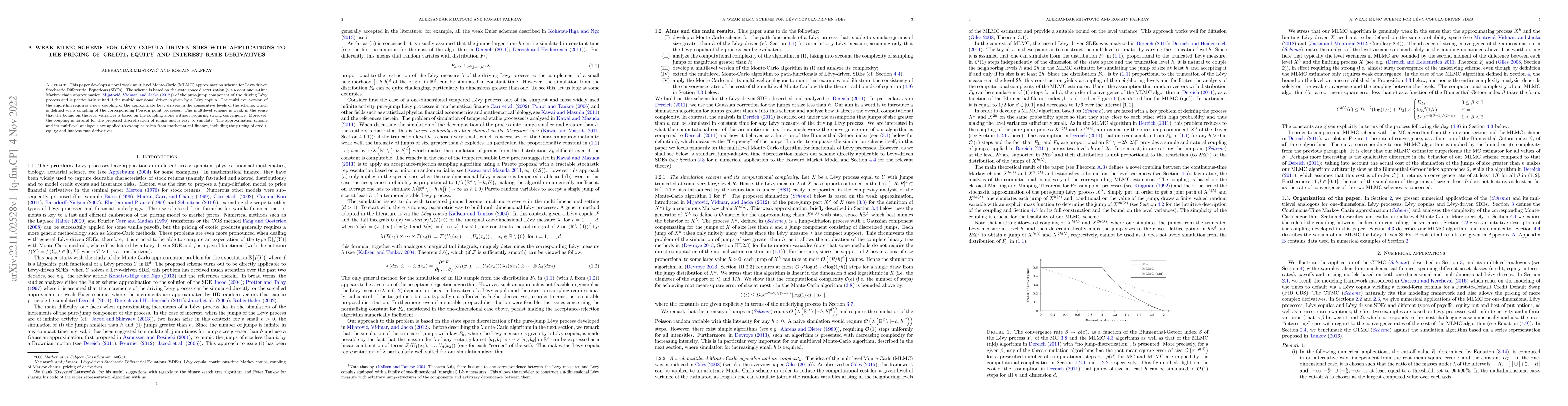

This paper develops a novel weak multilevel Monte-Carlo (MLMC) approximation scheme for L\'evy-driven Stochastic Differential Equations (SDEs). The scheme is based on the state space discretization ...

We study optimal Markovian couplings of Markov processes, where the optimality is understood in terms of minimization of concave transport costs between the time-marginal distributions of the couple...

For a multidimensional driftless diffusion in an unbounded, smooth, sub-linear generalized parabolic domain, with oblique reflection from the boundary, we give natural conditions under which either ...

We establish distributional limit theorems for the shape statistics of a concave majorant (i.e. the fluctuations of its length, its supremum, the time it is attained and its value at $T$) of any L\'...

We develop a novel Monte Carlo algorithm for the vector consisting of the supremum, the time at which the supremum is attained and the position at a given (constant) time of an exponentially tempere...

This paper presents a novel formula for the transition density of the Brownian motion on a sphere of any dimension and discusses an algorithm for the simulation of the increments of the spherical Br...

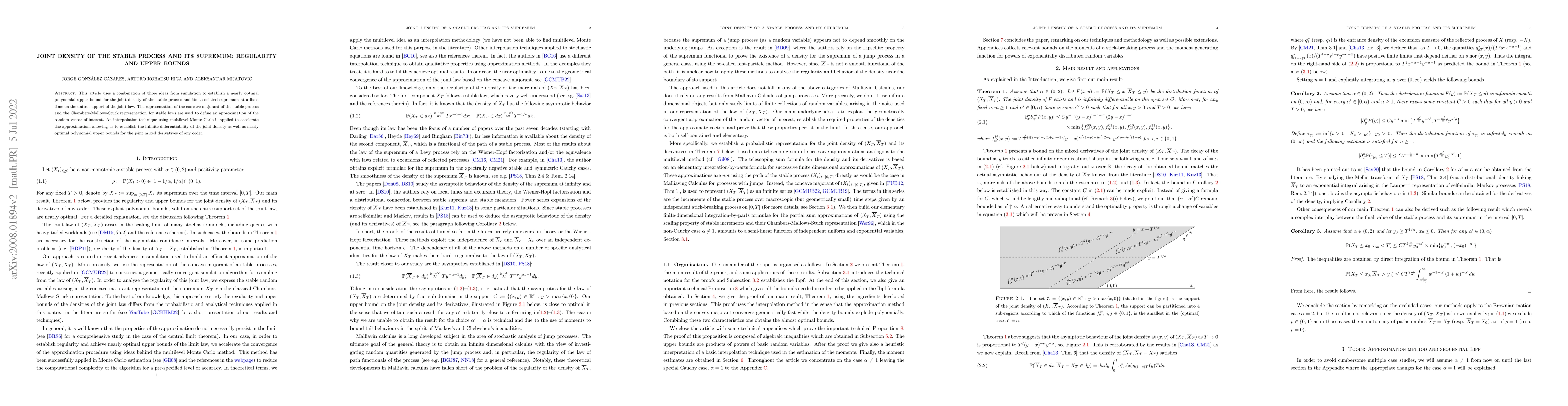

This article uses a combination of three ideas from simulation to establish a nearly optimal polynomial upper bound for the joint density of the stable process and its associated supremum at a fixed...

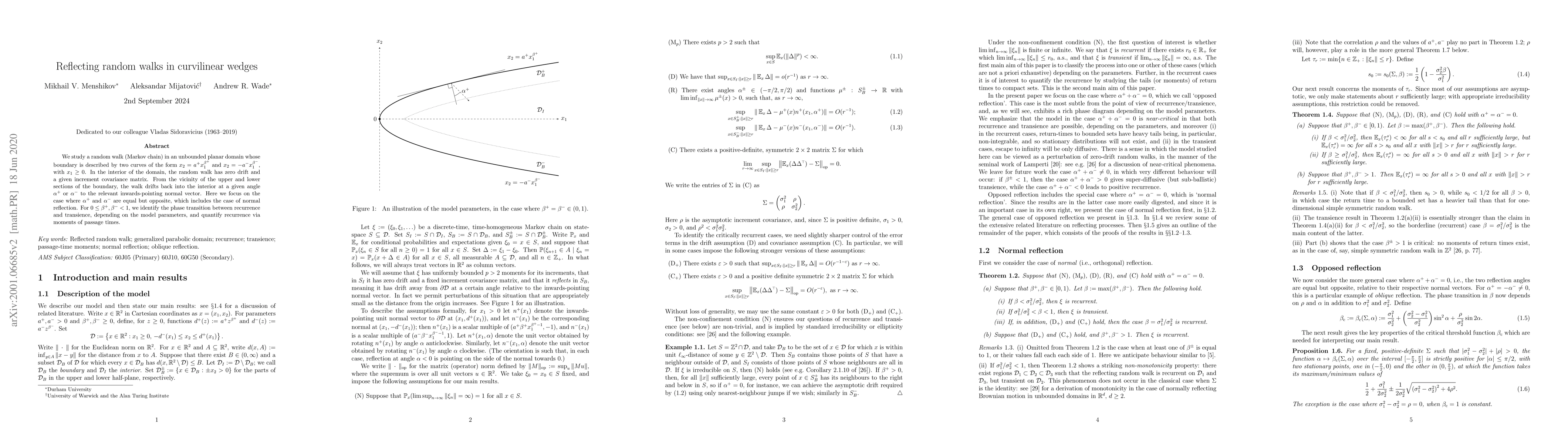

We study a random walk (Markov chain) in an unbounded planar domain whose boundary is described by two curves of the form $x_2 = a^+ x_1^{\beta^+}$ and $x_2 = -a^- x_1^{\beta^-}$, with $x_1 \geq 0$....

We provide verification theorems (at different levels of generality) for infinite horizon stochastic control problems in continuous time for semimartingales. The control framework is given as an abs...

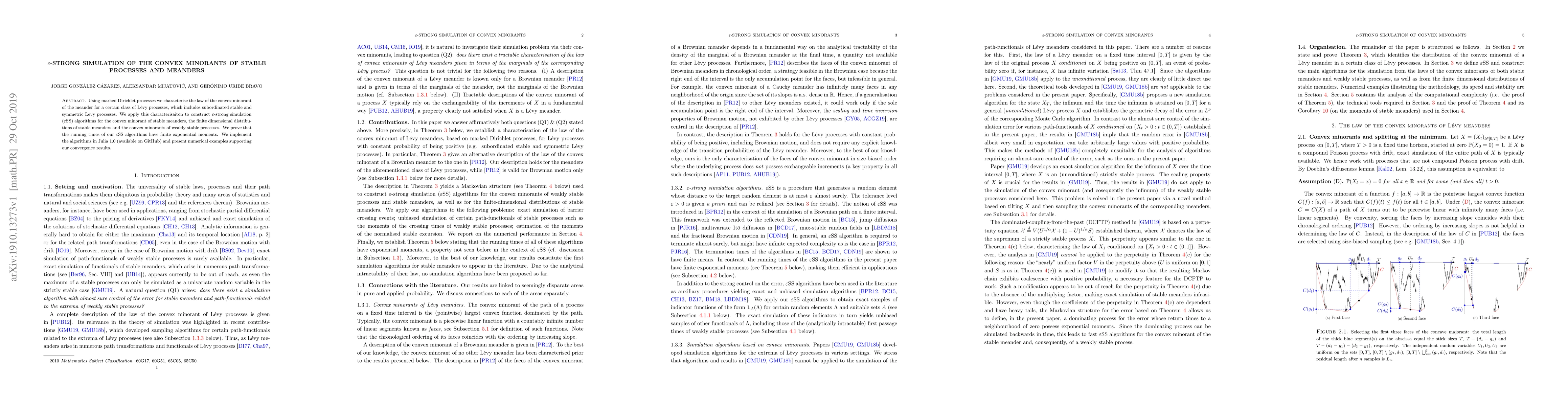

Using marked Dirichlet processes we characterise the law of the convex minorant of the meander for a certain class of L\'evy processes, which includes subordinated stable and symmetric L\'evy proces...

Consider a stochastic process $\mathfrak{X}$, regenerative at a state $x$ which is instantaneous and regular. Let $L$ be a regenerative local time for $\mathfrak{X}$ at $x$. Suppose furthermore that...

We describe an exact simulation algorithm for the increments of Brownian motion on a sphere of arbitrary dimension, based on the skew-product decomposition of the process with respect to the standar...

Discrete time analogues of ergodic stochastic differential equations (SDEs) are one of the most popular and flexible tools for sampling high-dimensional probability measures. Non-asymptotic analysis...

We exhibit an exact simulation algorithm for the supremum of a stable process over a finite time interval using dominated coupling from the past (DCFTP). We establish a novel perpetuity equation for...

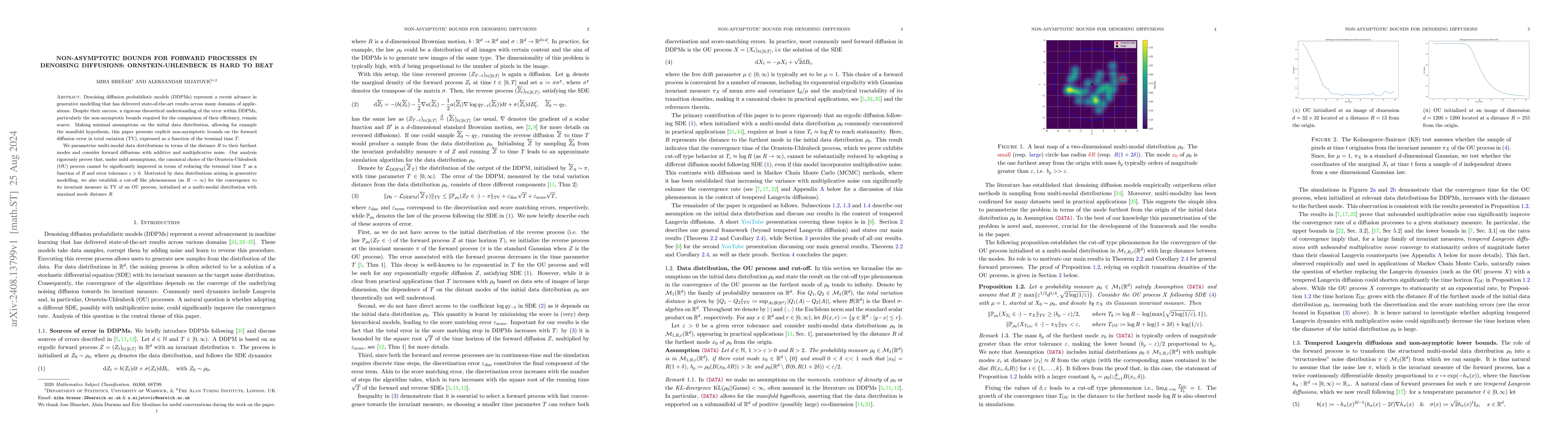

Denoising diffusion probabilistic models (DDPMs) represent a recent advance in generative modelling that has delivered state-of-the-art results across many domains of applications. Despite their succe...

Stochastic gradient descent is a classic algorithm that has gained great popularity especially in the last decades as the most common approach for training models in machine learning. While the algori...

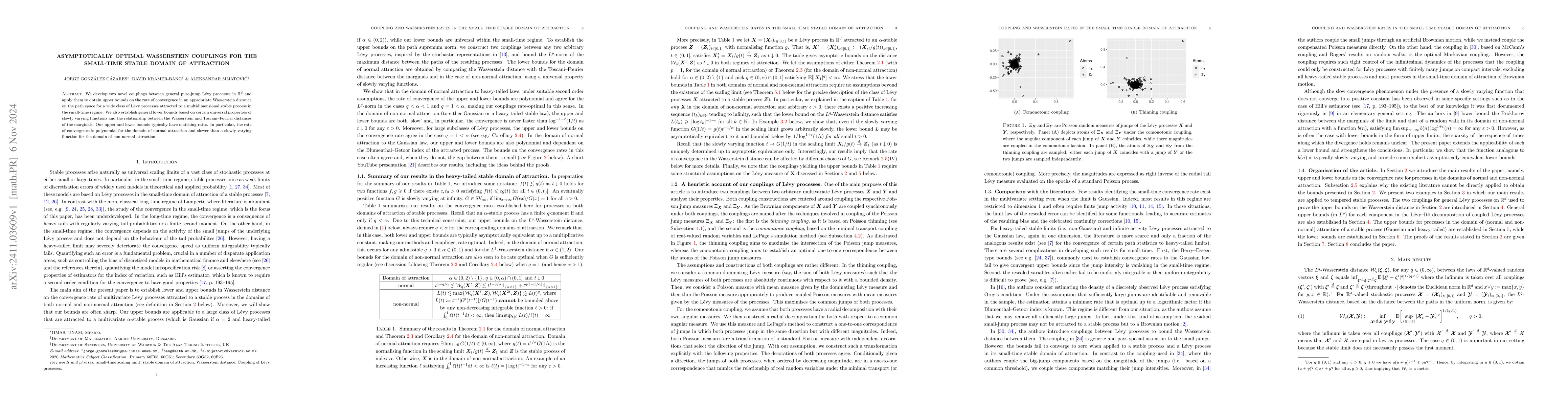

We develop two novel couplings between general pure-jump L\'evy processes in $\R^d$ and apply them to obtain upper bounds on the rate of convergence in an appropriate Wasserstein distance on the path ...

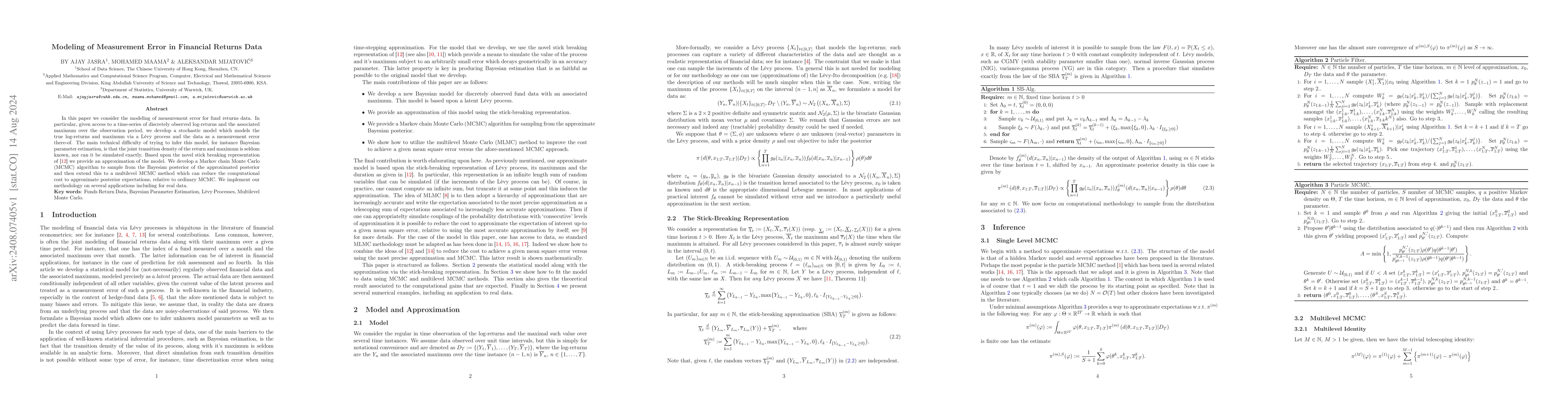

In this paper we consider the modeling of measurement error for fund returns data. In particular, given access to a time-series of discretely observed log-returns and the associated maximum over the o...

We study the second-order asymptotics around the superdiffusive strong law~\cite{MMW} of a multidimensional driftless diffusion with oblique reflection from the boundary in a generalised parabolic dom...

We establish the joint scaling limit of a critical Bienaym\'e-Galton-Watson process with immigration (BGWI) and its (counting) local time at zero to the corresponding self-similar continuous-state bra...

We prove that the norm of a $d$-dimensional L\'evy process possesses a finite second moment if and only if the convex distance between an appropriately rescaled process at time $t$ and a standard Gaus...

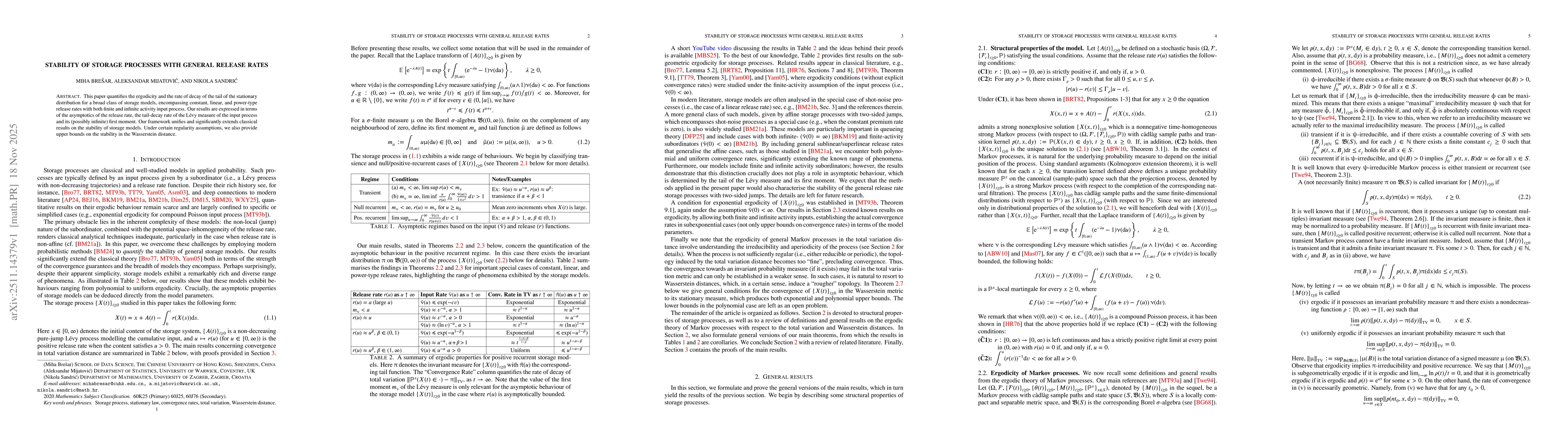

This paper quantifies the ergodicity and the rate of decay of the tail of the stationary distribution for a broad class of storage models, encompassing constant, linear, and power-type release rates w...

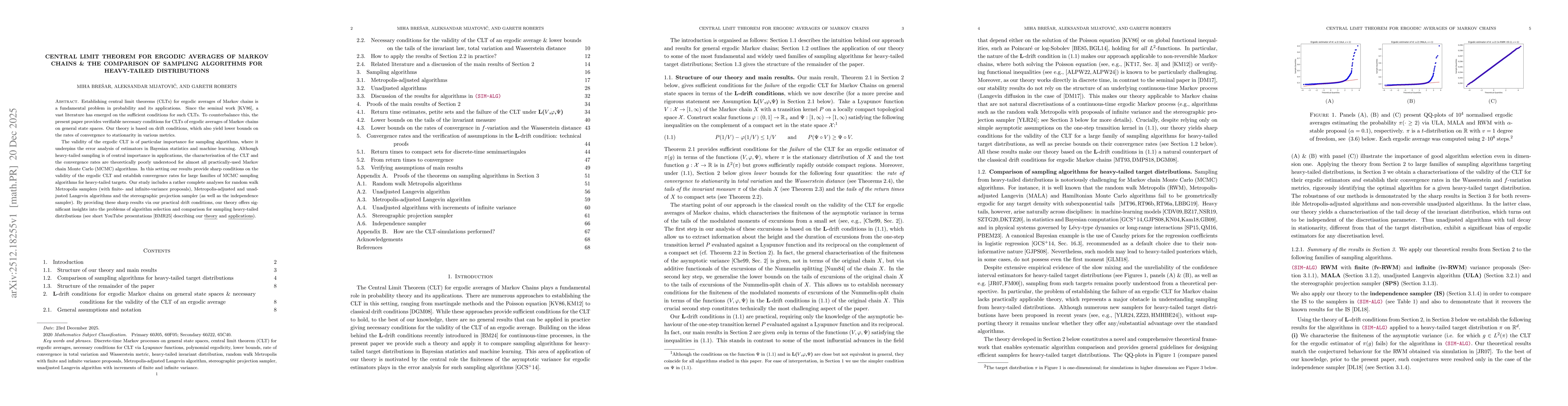

Establishing central limit theorems (CLTs) for ergodic averages of Markov chains is a fundamental problem in probability and its applications. Since the seminal work~\cite{MR834478}, a vast literature...

This paper establishes a functional stable central limit theorem for a class of superdiffusive solutions to stochastic differential equations driven by an $α$-stable process.