Academic Profile

Statistics

Similar Authors

Papers on arXiv

We provide precise conditions for nonparametric identification of causal effects by high-frequency event study regressions, which have been used widely in the recent macroeconomics, financial econom...

We show that the nonstandard limiting distribution of HAR test statistics under fixed-b asymptotics is not pivotal (even after studentization) when the data are nonstationarity. It takes the form of...

This paper develops change-point methods for the spectrum of a locally stationary time series. We focus on series with a bounded spectral density that change smoothly under the null hypothesis but e...

We introduce a nonparametric nonlinear VAR prewhitened long-run variance (LRV) estimator for the construction of standard errors robust to autocorrelation and heteroskedasticity that can be used for...

We establish theoretical results about the low frequency contamination (i.e., long memory effects) induced by general nonstationarity for estimates such as the sample autocovariance and the periodog...

We consider the derivation of data-dependent simultaneous bandwidths for double kernel heteroskedasticity and autocorrelation consistent (DK-HAC) estimators. In addition to the usual smoothing over ...

For a partial structural change in a linear regression model with a single break, we develop a continuous record asymptotic framework to build inference methods for the break date. We have T observa...

Under the classical long-span asymptotic framework we develop a class of Generalized Laplace (GL) inference methods for the change-point dates in a linear time series regression model with multiple ...

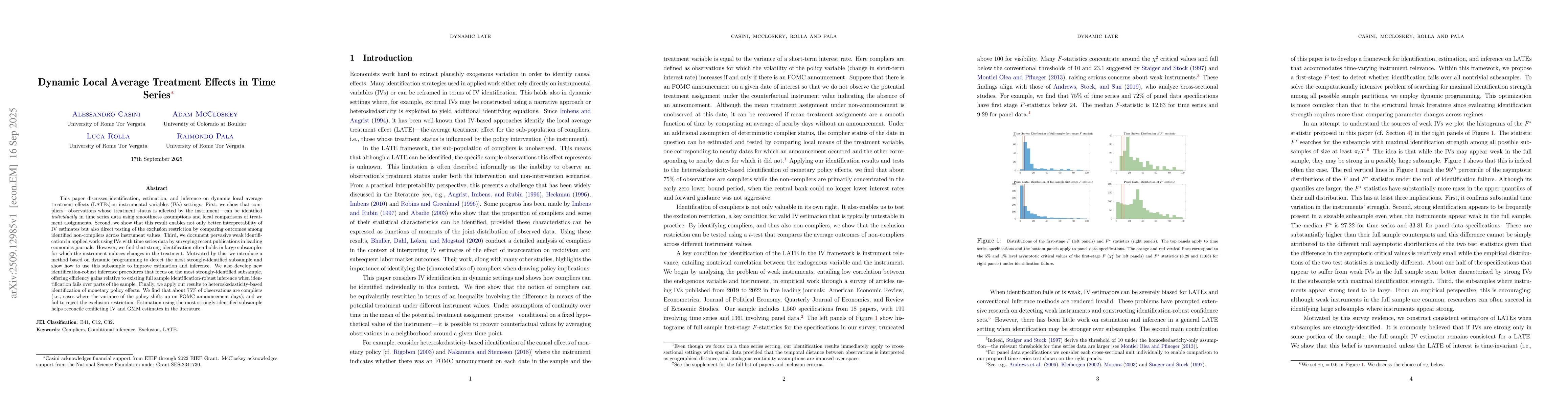

This paper discusses identification, estimation, and inference on dynamic local average treatment effects (LATEs) in instrumental variables (IVs) settings. First, we show that compliers--observations ...