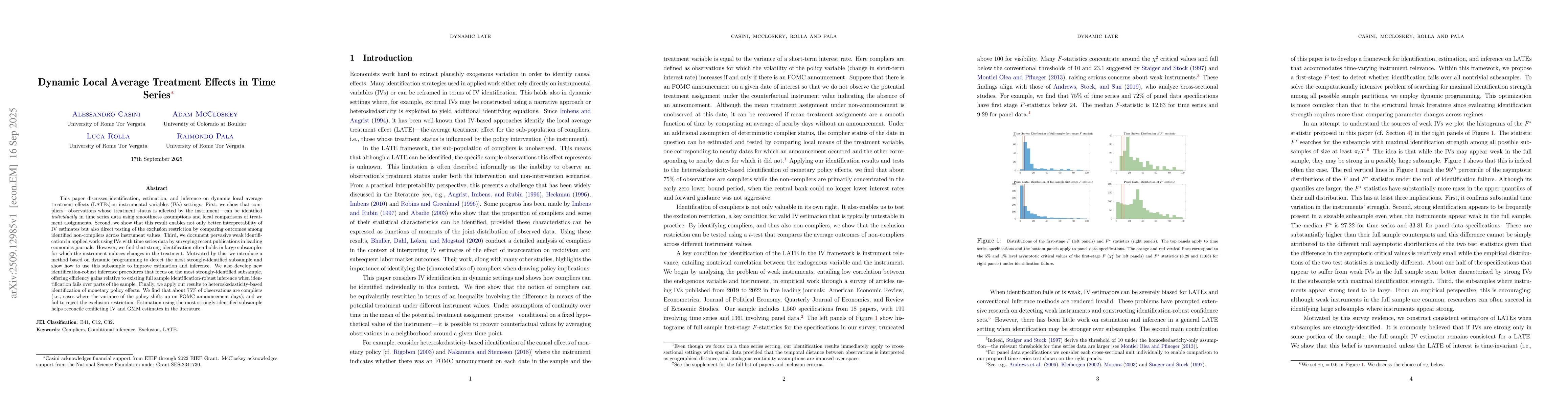

This paper discusses identification, estimation, and inference on dynamic

local average treatment effects (LATEs) in instrumental variables (IVs)

settings. First, we show that compliers--observations whose treatment status is

affected by the instrument--can be identified individually in time series data

using smoothness assumptions and local comparisons of treatment assignments.

Second, we show that this result enables not only better interpretability of IV

estimates but also direct testing of the exclusion restriction by comparing

outcomes among identified non-compliers across instrument values. Third, we

document pervasive weak identification in applied work using IVs with time

series data by surveying recent publications in leading economics journals.

However, we find that strong identification often holds in large subsamples for

which the instrument induces changes in the treatment. Motivated by this, we

introduce a method based on dynamic programming to detect the most

strongly-identified subsample and show how to use this subsample to improve

estimation and inference. We also develop new identification-robust inference

procedures that focus on the most strongly-identified subsample, offering

efficiency gains relative to existing full sample identification-robust

inference when identification fails over parts of the sample. Finally, we apply

our results to heteroskedasticity-based identification of monetary policy

effects. We find that about 75% of observations are compliers (i.e., cases

where the variance of the policy shifts up on FOMC announcement days), and we

fail to reject the exclusion restriction. Estimation using the most

strongly-identified subsample helps reconcile conflicting IV and GMM estimates

in the literature.

Discussion 0