Academic Profile

Statistics

Similar Authors

Papers on arXiv

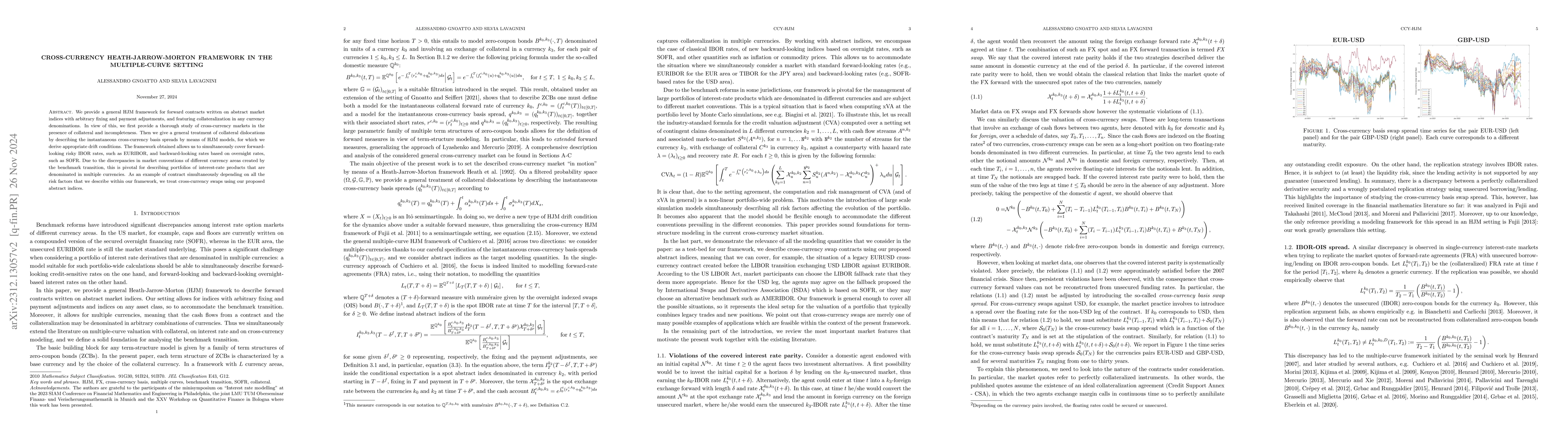

We provide a general HJM framework for forward contracts written on abstract market indices with arbitrary fixing and payment adjustments. We allow for indices on any asset class, featuring collater...

We present a novel computational approach for quadratic hedging in a high-dimensional incomplete market. This covers both mean-variance hedging and local risk minimization. In the first case, the so...

The aim of this work is to propose an extension of the Deep BSDE solver by Han, E, Jentzen (2017) to the case of FBSDEs with jumps. As in the aforementioned solver, starting from a discretized versi...

In this paper, we derive a representation for the value process associated to the solutions of FBSDEs in a jump-diffusion setting under multiple probability measures. Motivated by concrete financial...

We propose a quantization-based numerical scheme for a family of decoupled FBSDEs. We simplify the scheme for the control in Pag\`es and Sagna (2018) so that our approach is fully based on recursive...

In this paper, we present a novel computational framework for portfolio-wide risk management problems, where the presence of a potentially large number of risk factors makes traditional numerical te...

We generalize the results of Bielecki and Rutkowski (2015) on funding and collateralization to a multi-currency framework and link their results with those of Piterbarg (2012), Moreni and Pallavicin...

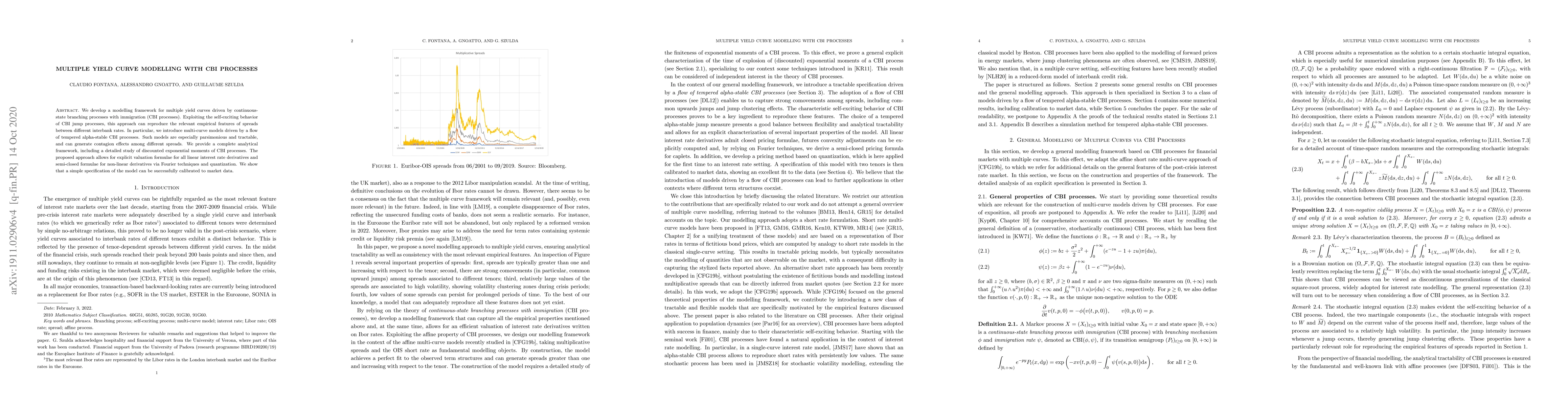

We develop a modelling framework for multiple yield curves driven by continuous-state branching processes with immigration (CBI processes). Exploiting the self-exciting behavior of CBI jump processe...

In this paper we extend the existing literature on xVA along three directions. First, we enhance current BSDE-based xVA frameworks to include initial margin in presence of defaults. Next, we solve t...

We study the error arising in the numerical approximation of FBSDEs and related PIDEs by means of a deep learning-based method. Our results focus on decoupled FBSDEs with jumps and extend the seminal ...

We propose a structural default model for portfolio-wide valuation adjustments (xVAs) and represent it as a system of coupled backward stochastic differential equations. The framework is divided into ...

We consider the pricing and hedging of counterparty credit risk and funding when there is no possibility to hedge the jump to default of either the bank or the counterparty. This represents the situat...

We present the first deep-learning solver for backward stochastic Volterra integral equations (BSVIEs) and their fully-coupled forward-backward variants. The method trains a neural network to approxim...