Academic Profile

Statistics

Similar Authors

Papers on arXiv

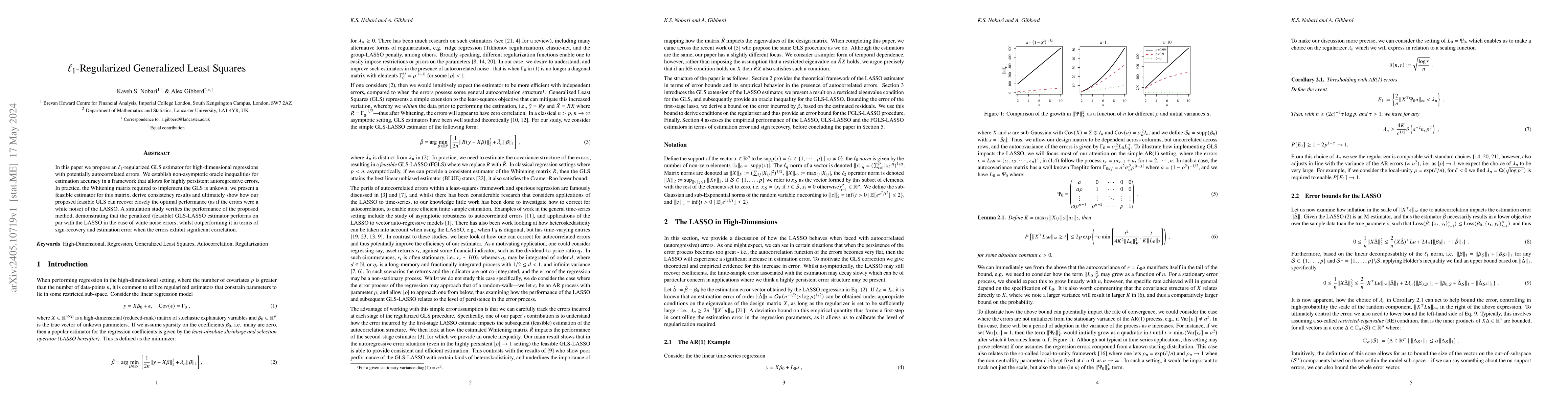

In this paper we propose an $\ell_1$-regularized GLS estimator for high-dimensional regressions with potentially autocorrelated errors. We establish non-asymptotic oracle inequalities for estimation...

Advances in modern technology have enabled the simultaneous recording of neural spiking activity, which statistically can be represented by a multivariate point process. We characterise the second o...

Low-frequency time-series (e.g., quarterly data) are often treated as benchmarks for interpolating to higher frequencies, since they generally exhibit greater precision and accuracy in contrast to t...

sparseDFM is an R package for the implementation of popular estimation methods for dynamic factor models (DFMs) including the novel Sparse DFM approach of Mosley et al. (2023). The Sparse DFM amelio...

The concepts of sparsity, and regularised estimation, have proven useful in many high-dimensional statistical applications. Dynamic factor models (DFMs) provide a parsimonious approach to modelling ...

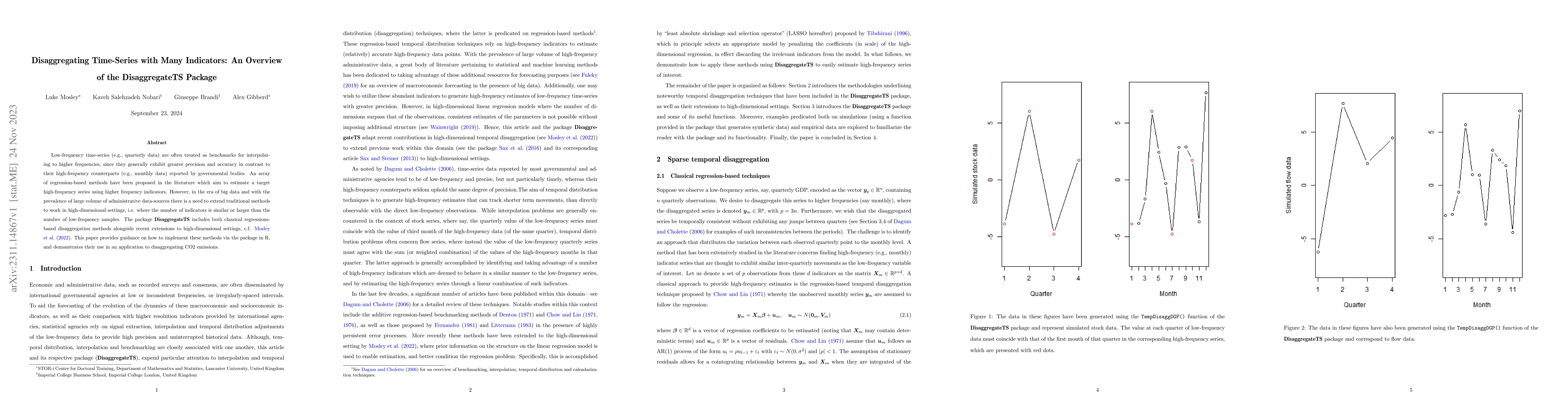

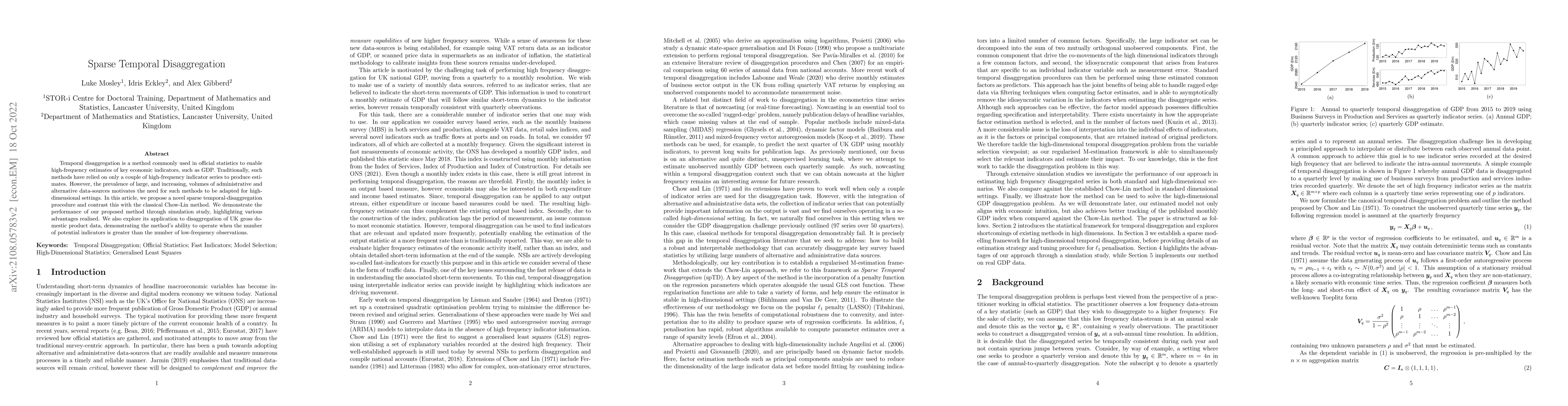

Temporal disaggregation is a method commonly used in official statistics to enable high-frequency estimates of key economic indicators, such as GDP. Traditionally, such methods have relied on only a...

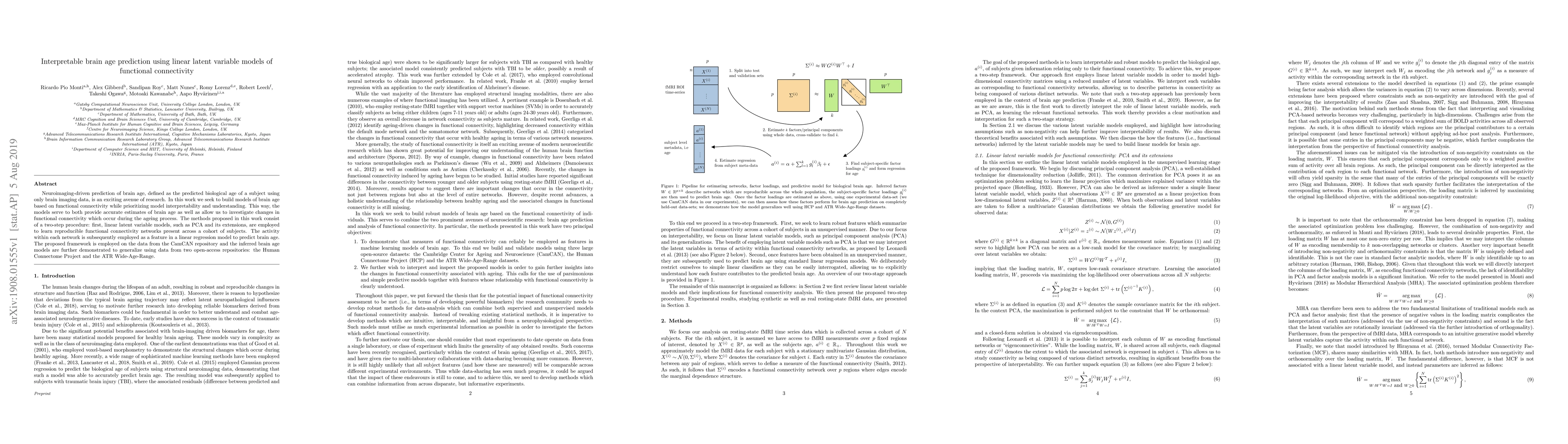

Neuroimaging-driven prediction of brain age, defined as the predicted biological age of a subject using only brain imaging data, is an exciting avenue of research. In this work we seek to build mode...

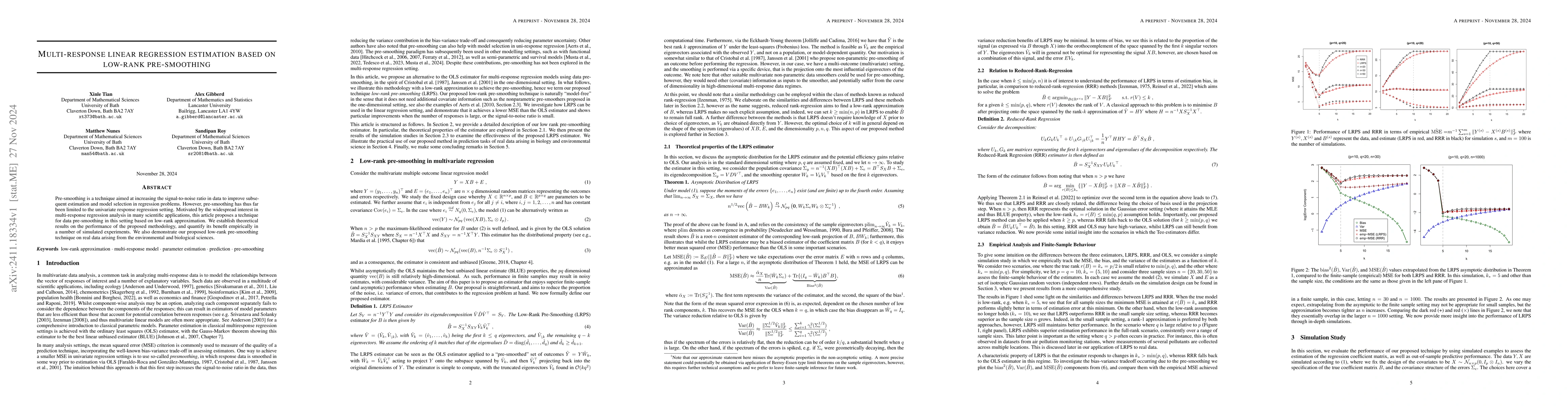

Pre-smoothing is a technique aimed at increasing the signal-to-noise ratio in data to improve subsequent estimation and model selection in regression problems. However, pre-smoothing has thus far been...

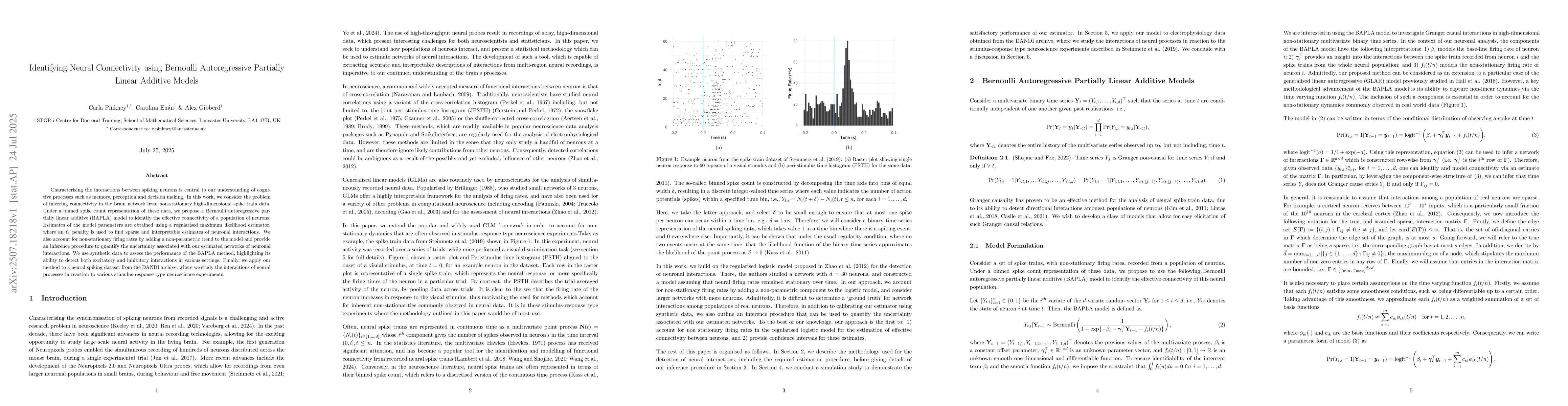

Characterising the interactions between spiking neurons is central to our understanding of cognitive processes such as memory, perception and decision making. In this work, we consider the problem of ...