Academic Profile

Statistics

Similar Authors

Papers on arXiv

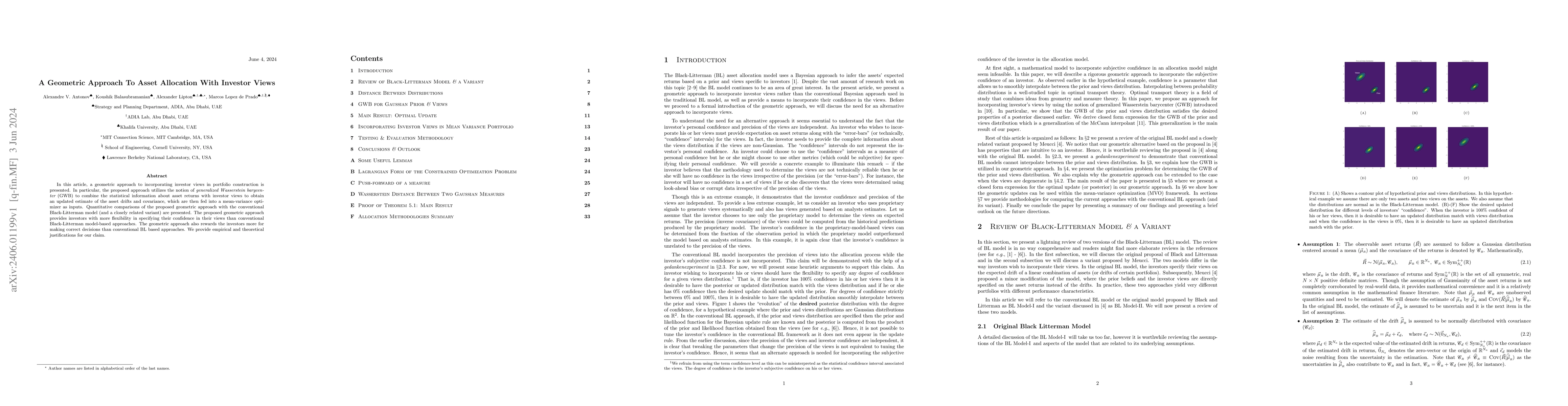

In this article, a geometric approach to incorporating investor views in portfolio construction is presented. In particular, the proposed approach utilizes the notion of generalized Wasserstein bary...

An intriguing link between a wide range of problems occurring in physics and financial engineering is presented. These problems include the evolution of small perturbations of linear flows in hydrod...

We discover several surprising relationships between large classes of seemingly unrelated foundational problems of financial engineering and fundamental problems of hydrodynamics and molecular physi...

Local Stochastic Volatility (LSV) models have been used for pricing and hedging derivatives positions for over twenty years. An enormous body of literature covers analytical and numerical techniques...

We combine the one-dimensional Monte Carlo simulation and the semi-analytical one-dimensional heat potential method to design an efficient technique for pricing barrier options on assets with correl...

By expanding the Dirac delta function in terms of the eigenfunctions of the corresponding Sturm-Liouville problem, we construct some new (oscillating) integral transforms. These transforms are then ...

We review different classes of cryptocurrencies with emphasis on their economic properties. Pure-asset coins such as Bitcoin, Ethereum and Ripple are characterized by not being a liability of any ec...

We introduce the contract service provider (CSP) model as an analog of the successful Internet ISP model. Our exploration is motivated by the need to seek alternative blockchain service-fee models t...

The emerging virtual asset service providers (VASP) industry currently faces a number of challenges related to the Travel Rule, notably pertaining to customer personal information, account number an...

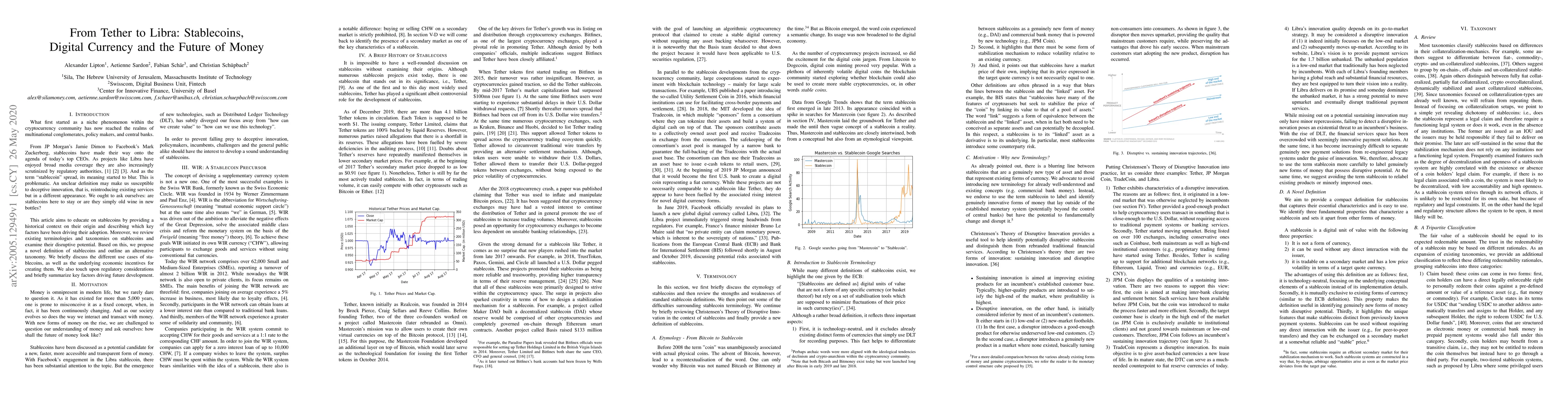

This paper provides an overview on stablecoins and introduces a novel terminology to help better identify stablecoins with truly disruptive potential. It provides a compact definition for stablecoin...

We analyze an approach to managing the COVID-19 pandemic without shutting down the economy while staying within the capacity of the healthcare system. We base our analysis on a detailed heterogeneou...

Answers to interview questions sent to a selected group of former physicists working in finance. The interview will be published as part of a Special Issue on Physics and Derivatives by The Journal ...

When prices reflect all available information, they oscillate around an equilibrium level. This oscillation is the result of the temporary market impact caused by waves of buyers and sellers. This p...

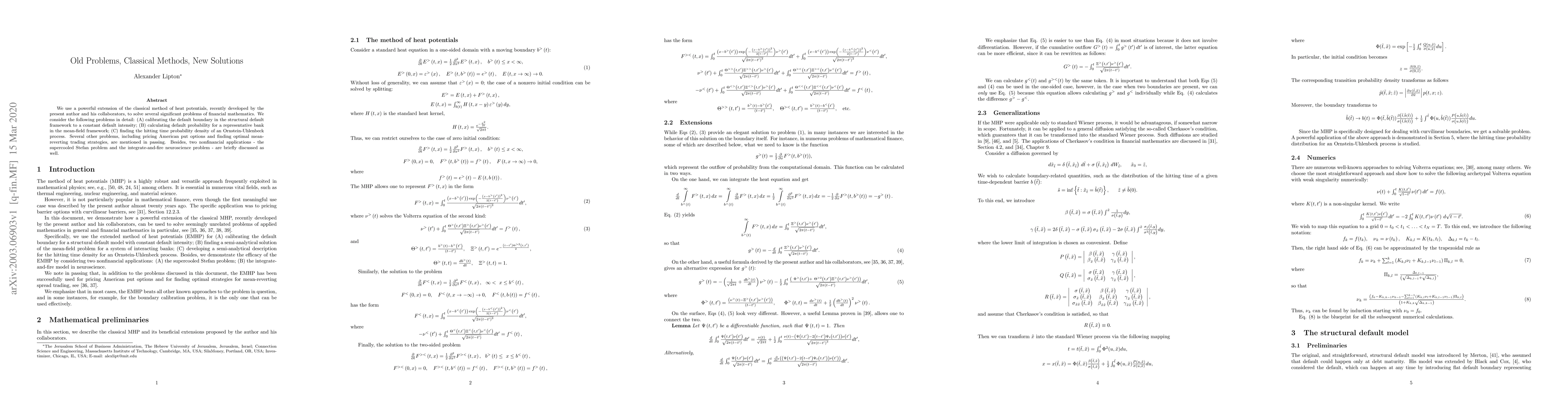

We use a powerful extension of the classical method of heat potentials, recently developed by the present author and his collaborators, to solve several significant problems of financial mathematics...

The recent FATF Recommendations defines virtual assets and virtual assets service providers (VASP), and requires under the Travel Rule that originating VASPs obtain and hold required and accurate or...

We develop static and dynamic approaches for hedging of the impermanent loss (IL) of liquidity provision (LP) staked at Decentralised Exchanges (DEXes) which employ Uniswap V2 and V3 protocols. We pro...