A Geometric Approach To Asset Allocation With Investor Views

Publication

Metrics

AI Quick Summary

This paper introduces a geometric approach to asset allocation that uses the generalized Wasserstein barycenter to integrate investor views into portfolio construction, offering greater flexibility and reward for correct decisions compared to the conventional Black-Litterman model. Empirical and theoretical justifications support the effectiveness of this new method.

Paper Preview

Abstract

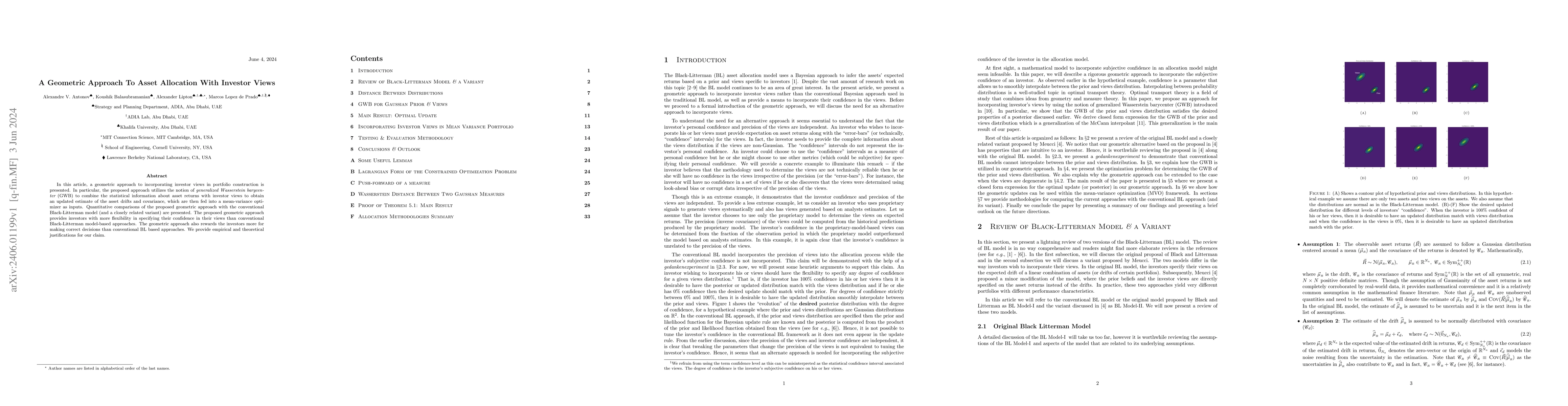

In this article, a geometric approach to incorporating investor views in portfolio construction is presented. In particular, the proposed approach utilizes the notion of generalized Wasserstein barycenter (GWB) to combine the statistical information about asset returns with investor views to obtain an updated estimate of the asset drifts and covariance, which are then fed into a mean-variance optimizer as inputs. Quantitative comparisons of the proposed geometric approach with the conventional Black-Litterman model (and a closely related variant) are presented. The proposed geometric approach provides investors with more flexibility in specifying their confidence in their views than conventional Black-Litterman model-based approaches. The geometric approach also rewards the investors more for making correct decisions than conventional BL based approaches. We provide empirical and theoretical justifications for our claim.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0