1

arXiv Papers

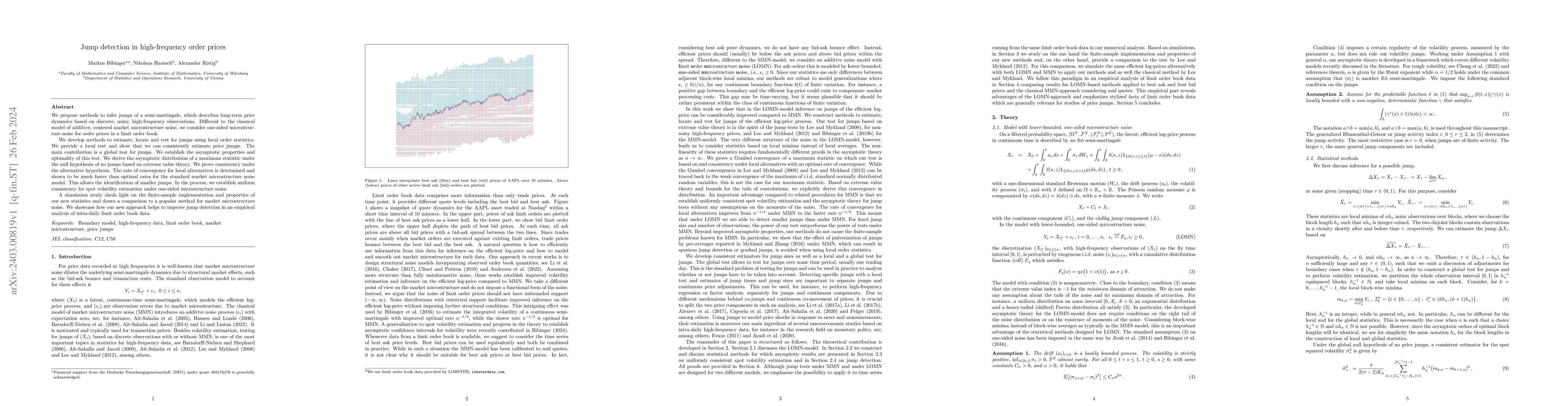

17

Total Publications

Profile

Academic Profile

Metrics

Statistics

1

arXiv Papers

17

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

Jump detection in high-frequency order prices

We propose methods to infer jumps of a semi-martingale, which describes long-term price dynamics based on discrete, noisy, high-frequency observations. Different to the classical model of additive, ...