Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study a class of high frequency path functionals of a diffusion with a singular threshold, including the case of a sticky-reflection, and establish convergence to the local time. These functional...

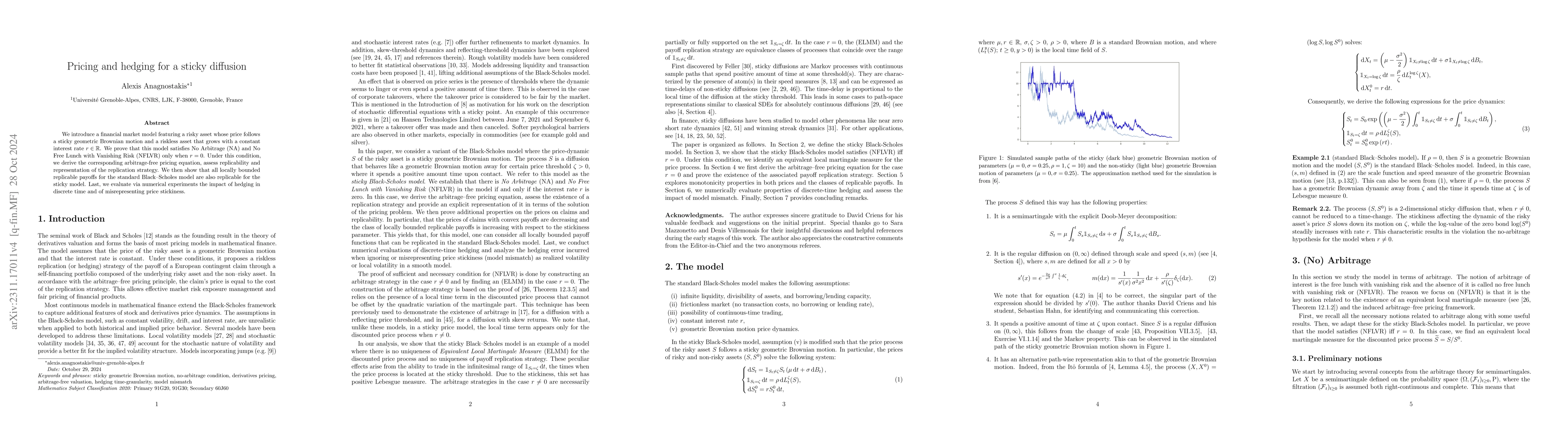

We consider a financial market model featuring a risky asset with a sticky geometric Brownian motion price dynamic and a constant interest rate $r \in \mathbb R$. We prove that the model is arbitrag...

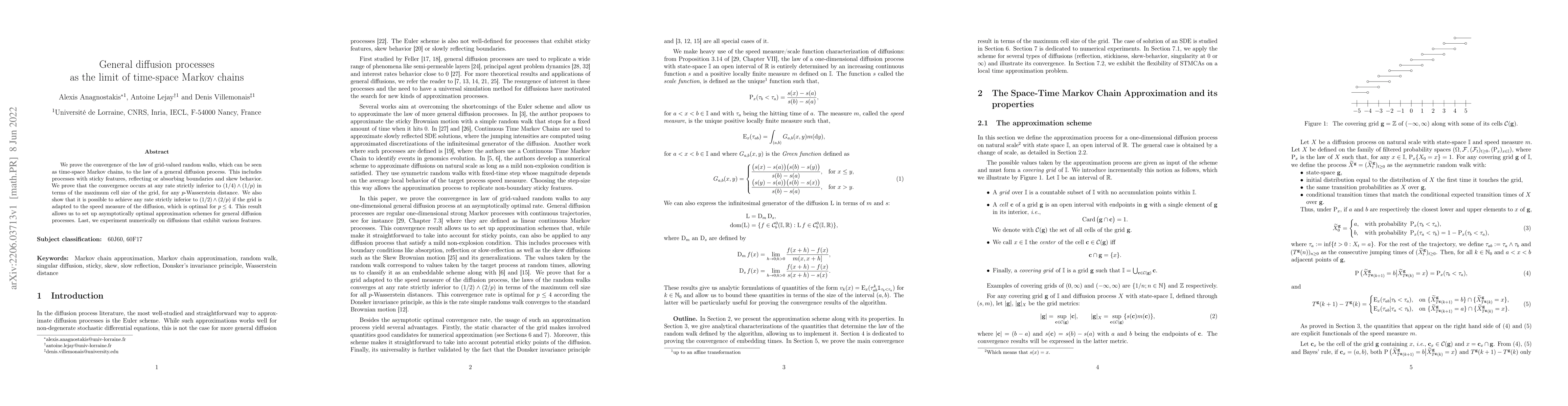

We prove the convergence of the law of grid-valued random walks, which can be seen as time-space Markov chains, to the law of a general diffusion process. This includes processes with sticky feature...

We distinguish between three types of crossing behaviors at a sticky threshold for a one-dimensional sticky diffusion process and analyze the asymptotic properties of the three corresponding number of...

We establish a representation of general regular diffusions on star-shaped graphs as time-changed Walsh Brownian motions. These are Markov processes with continuous sample paths whose law on each edge...

We establish deterministic necessary and sufficient conditions for the no-arbitrage notions "no increasing profit" (NIP), "no strong arbitrage" (NSA) and "no unbounded profit with bounded risk" (NUPBR...

We introduce the Space-Time Markov Chain Approximation (STMCA) for a general diffusion process on a finite metric graph $\Gamma$. The STMCA is a doubly asymmetric (in both time and space) random walk ...

In this paper, we investigate a financial market model consisting of a risky asset, modeled as a general diffusion parameterized by a scale function and a speed measure, and a bank account process wit...