Academic Profile

Statistics

Similar Authors

Papers on arXiv

Recent studies propose enhancing machine learning models by aligning the geometric characteristics of the latent space with the underlying data structure. Instead of relying solely on Euclidean spac...

Recent research indicates that the performance of machine learning models can be improved by aligning the geometry of the latent space with the underlying data structure. Rather than relying solely ...

One of the key decisions in execution strategies is the choice between a passive (liquidity providing) or an aggressive (liquidity taking) order to execute a trade in a limit order book (LOB). Essen...

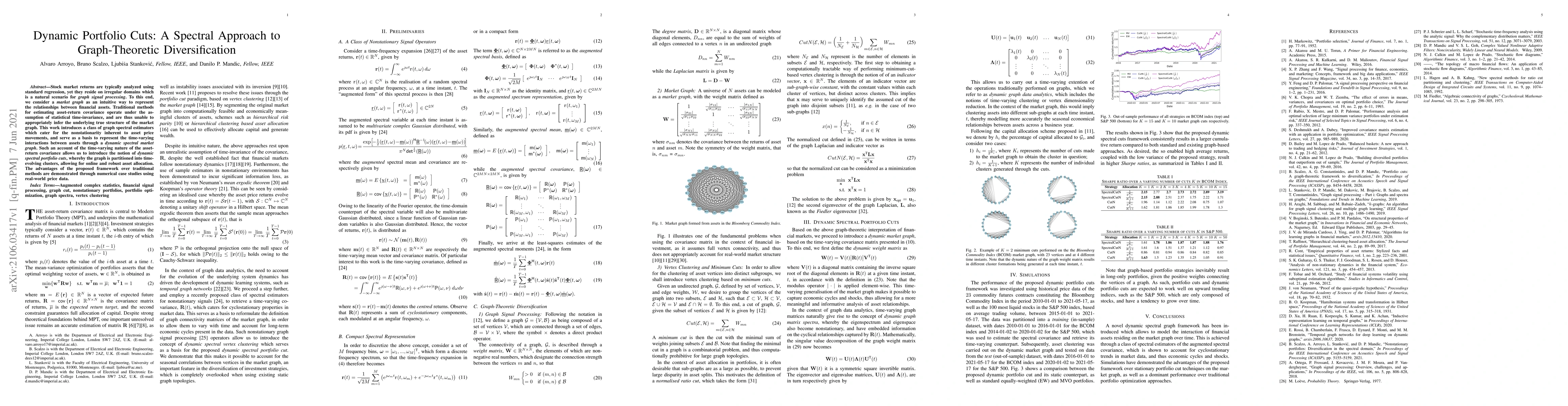

Stock market returns are typically analyzed using standard regression, yet they reside on irregular domains which is a natural scenario for graph signal processing. To this end, we consider a market...

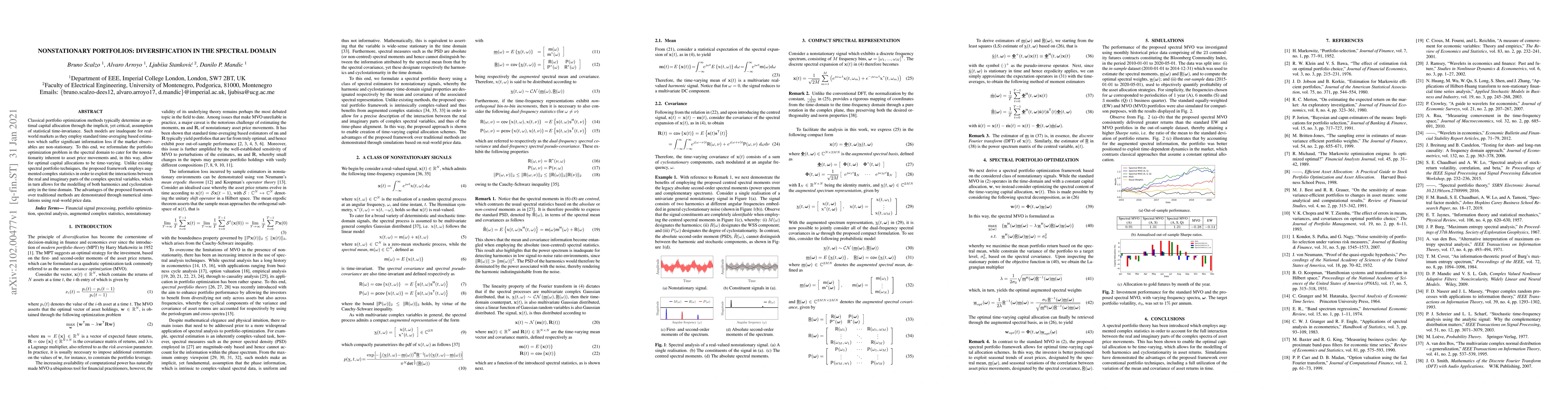

Classical portfolio optimization methods typically determine an optimal capital allocation through the implicit, yet critical, assumption of statistical time-invariance. Such models are inadequate f...