Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper addresses the problem of pricing involved financial derivatives by means of advanced of deep learning techniques. More precisely, we smartly combine several sophisticated neural network-b...

We present a novel methodology to price derivative contracts using quantum computers by means of Quantum Accelerated Monte Carlo. Our contribution is an algorithm that permits pricing derivative con...

The goal of this work is to develop deep learning numerical methods for solving option XVA pricing problems given by non-linear PDE models. A novel strategy for the treatment of the boundary conditi...

We introduce the Real Quantum Amplitude Estimation (RQAE) algorithm, an extension of Quantum Amplitude Estimation (QAE) which is sensitive to the sign of the amplitude. RQAE is an iterative algorith...

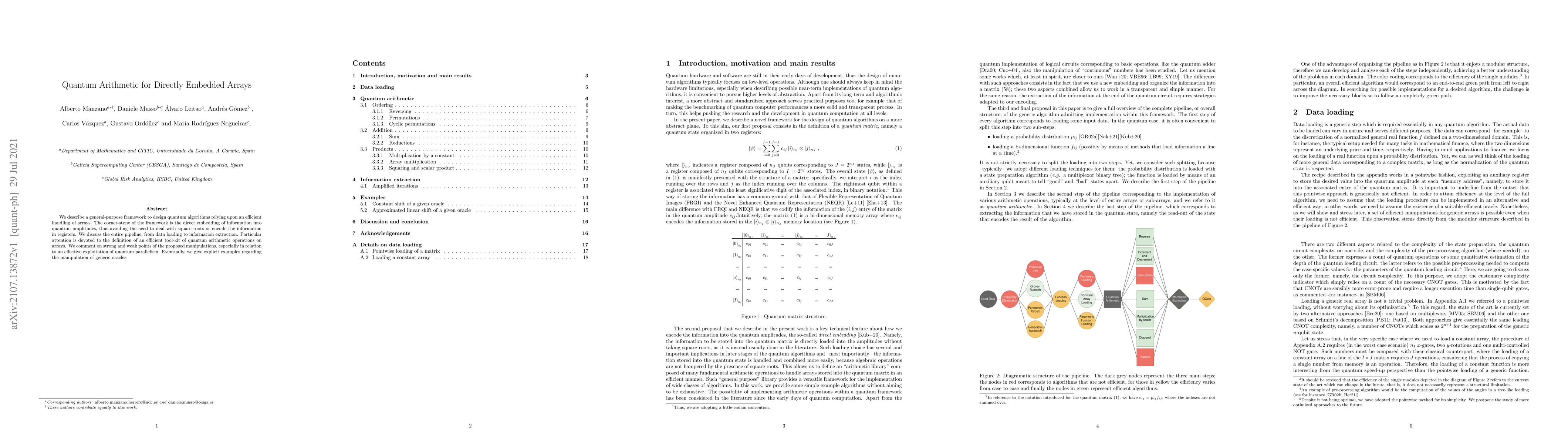

We describe a general-purpose framework to design quantum algorithms relying upon an efficient handling of arrays. The corner-stone of the framework is the direct embedding of information into quant...

In this article we mainly extend the deterministic model developed in [10] to a stochastic setting. More precisely, we incorporated randomness in some coefficients by assuming that they follow a pre...

Extracting implied information, like volatility and/or dividend, from observed option prices is a challenging task when dealing with American options, because of the computational costs needed to so...

The present work addresses the challenge of training neural networks for Dynamic Initial Margin (DIM) computation in counterparty credit risk, a task traditionally burdened by the high costs associate...

The ongoing progress in quantum technologies has fueled a sustained exploration of their potential applications across various domains. One particularly promising field is quantitative finance, where ...

In this work, we introduce a machine/deep learning methodology to solve parametric integrals. Besides classical machine learning approaches, we consider a differential learning framework that incorpor...

This work introduces an end-to-end framework for multi-asset option pricing that combines market-consistent risk-neutral density recovery with quantum-accelerated numerical integration. We first calib...