Publication

Metrics

AI Quick Summary

This paper introduces a novel quantum algorithm for pricing derivative contracts using Quantum Accelerated Monte Carlo, capable of handling negative payoffs and prices, which existing quantum algorithms cannot. Experimental results show that the proposed method retains speedups compared to other quantum proposals.

Paper Preview

Abstract

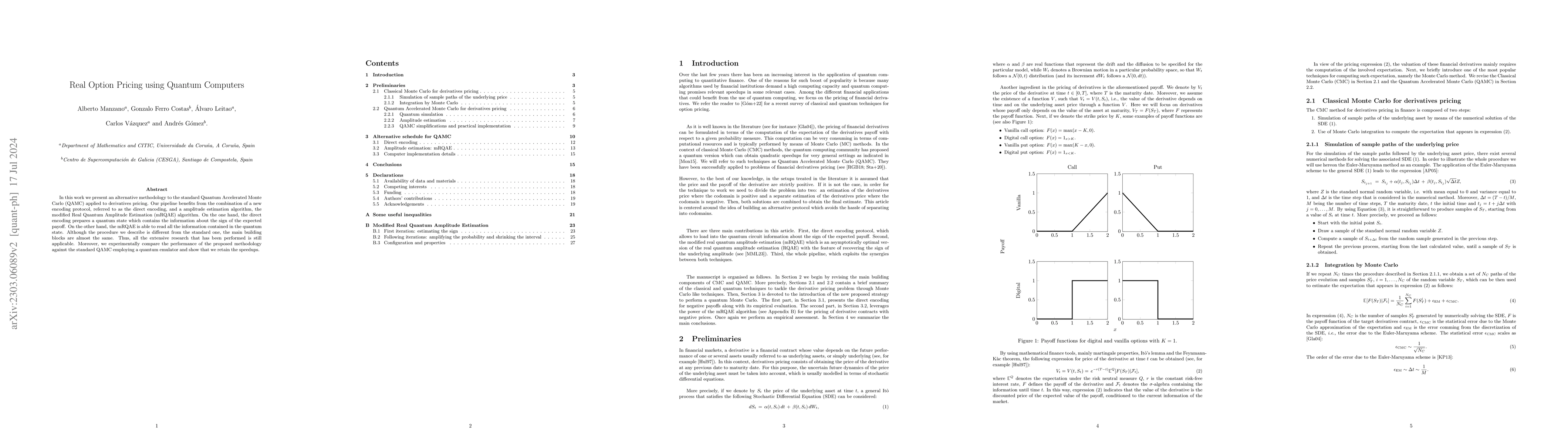

We present a novel methodology to price derivative contracts using quantum computers by means of Quantum Accelerated Monte Carlo. Our contribution is an algorithm that permits pricing derivative contracts with negative payoffs. Note that the presence of negative payoffs can give rise to negative prices. This behaviour cannot be captured by existing quantum algorithms. Although the procedure we describe is different from the standard one, the main building blocks are the same. Thus, all the extensive research that has been performed is still applicable. Moreover, we experimentally compare the performance of the proposed methodology against other proposals employing a quantum emulator and show that we retain the speedups.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0