Academic Profile

Statistics

Similar Authors

Papers on arXiv

Time-Varying Parameters Vector Autoregressive (TVP-VAR) models are frequently used in economics to capture evolving relationships among the macroeconomic variables. However, TVP-VARs have the tenden...

Monitoring downside risk and upside risk to the key macroeconomic indicators is critical for effective policymaking aimed at maintaining economic stability. In this paper I propose a parametric fram...

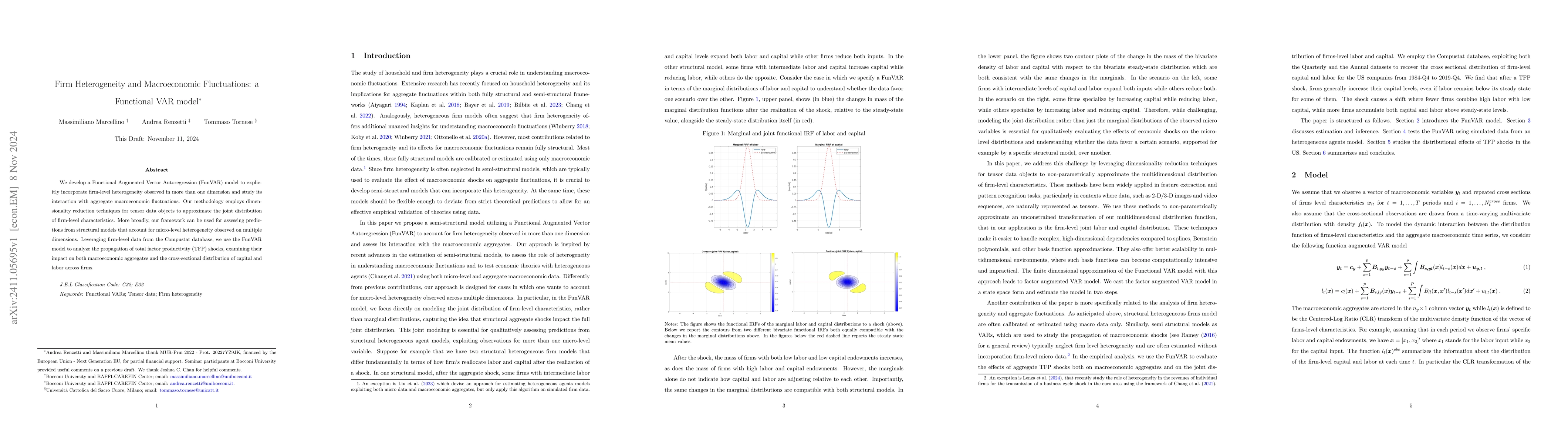

We develop a Functional Augmented Vector Autoregression (FunVAR) model to explicitly incorporate firm-level heterogeneity observed in more than one dimension and study its interaction with aggregate m...

We propose a functional MIDAS model to leverage high-frequency information for forecasting and nowcasting distributions observed at a lower frequency. We approximate the low-frequency distribution usi...