01

MethodologyHow they did it

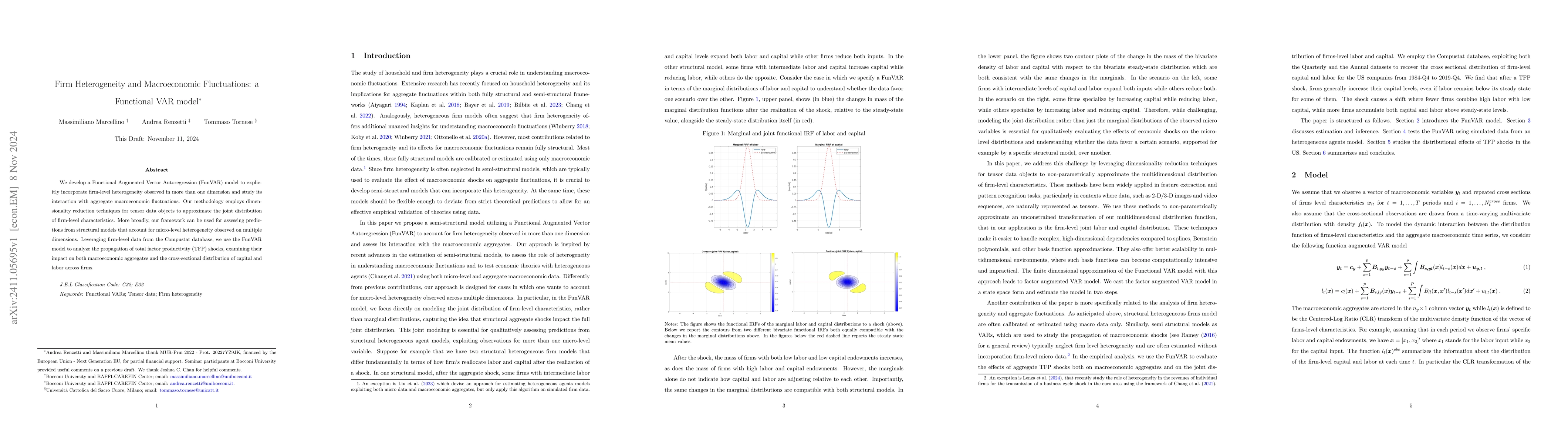

The paper develops a Functional Augmented Vector Autoregression (FunVAR) model to explicitly incorporate firm-level heterogeneity observed in more than one dimension and study its interaction with aggregate macroeconomic fluctuations. The methodology employs dimensionality reduction techniques for tensor data objects to approximate the joint distribution of firm-level characteristics.

Discussion 0