Academic Profile

Statistics

Similar Authors

Papers on arXiv

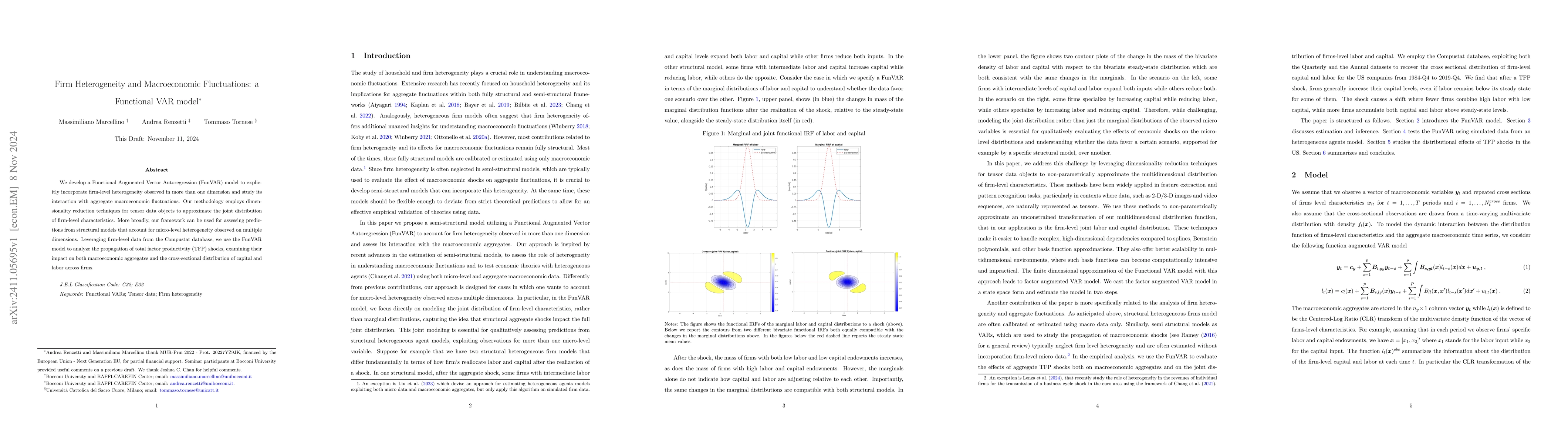

We develop a Functional Augmented Vector Autoregression (FunVAR) model to explicitly incorporate firm-level heterogeneity observed in more than one dimension and study its interaction with aggregate m...

We propose a functional MIDAS model to leverage high-frequency information for forecasting and nowcasting distributions observed at a lower frequency. We approximate the low-frequency distribution usi...

We study the distributional implications of uncertainty shocks by developing a model that links macroeconomic aggregates to the US distribution of earnings and consumption. We find that: initially, th...