Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose and discuss Bayesian machine learning methods for mixed data sampling (MIDAS) regressions. This involves handling frequency mismatches with restricted and unrestricted MIDAS variants and ...

Model mis-specification in multivariate econometric models can strongly influence quantities of interest such as structural parameters, forecast distributions or responses to structural shocks, even...

Macroeconomic data is characterized by a limited number of observations (small T), many time series (big K) but also by featuring temporal dependence. Neural networks, by contrast, are designed for ...

The relationship between inflation and predictors such as unemployment is potentially nonlinear with a strength that varies over time, and prediction errors error may be subject to large, asymmetric...

We develop a non-parametric multivariate time series model that remains agnostic on the precise relationship between a (possibly) large set of macroeconomic time series and their lagged values. The ...

We develop a Bayesian non-parametric quantile panel regression model. Within each quantile, the response function is a convex combination of a linear model and a non-linear function, which we approx...

Based on evidence gathered from a newly built large macroeconomic data set for the UK, labeled UK-MD and comparable to similar datasets for the US and Canada, it seems the most promising avenue for ...

This paper analyzes nonlinearities in the international transmission of financial shocks originating in the US. To do so, we develop a flexible nonlinear multi-country model. Our framework is capable ...

We propose a method to learn the nonlinear impulse responses to structural shocks using neural networks, and apply it to uncover the effects of US financial shocks. The results reveal substantial asym...

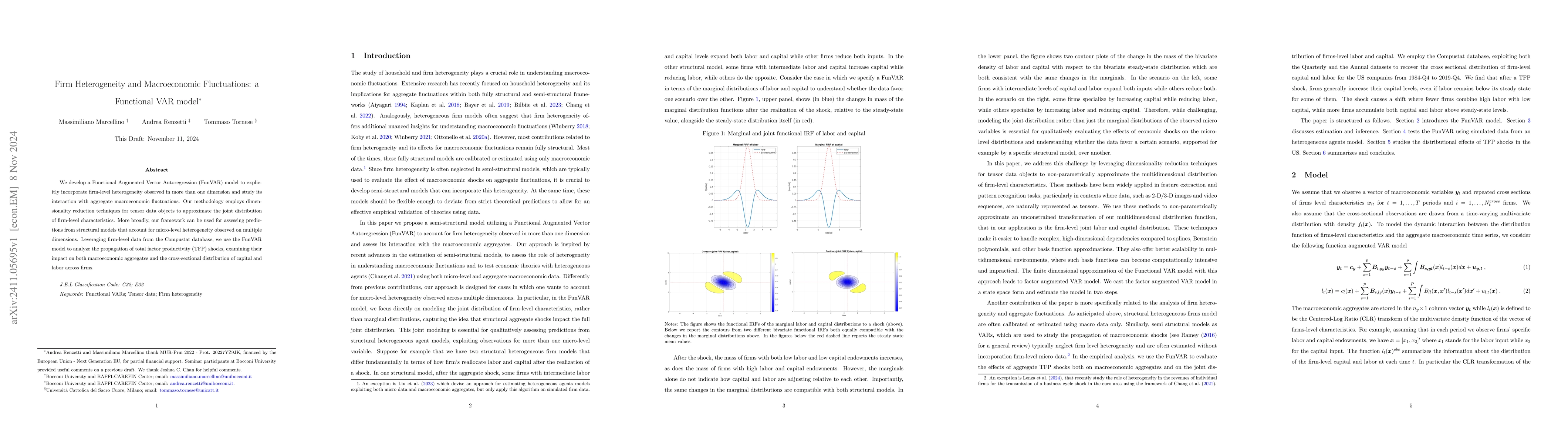

We develop a Functional Augmented Vector Autoregression (FunVAR) model to explicitly incorporate firm-level heterogeneity observed in more than one dimension and study its interaction with aggregate m...

We propose a functional MIDAS model to leverage high-frequency information for forecasting and nowcasting distributions observed at a lower frequency. We approximate the low-frequency distribution usi...

We study the distributional implications of uncertainty shocks by developing a model that links macroeconomic aggregates to the US distribution of earnings and consumption. We find that: initially, th...

Commonly used priors for Vector Autoregressions (VARs) induce shrinkage on the autoregressive coefficients. Introducing shrinkage on the error covariance matrix is sometimes done but, in the vast majo...