Academic Profile

Statistics

Similar Authors

Papers on arXiv

The simulation of the expectation of a stochastic quantity E[Y] by Monte Carlo methods is known to be computationally expensive especially if the stochastic quantity or its approximation Y_n is expe...

The (asymptotic) behaviour of the second moment of solutions to stochastic differential equations is treated in mean-square stability analysis. This property is discussed for approximations of infin...

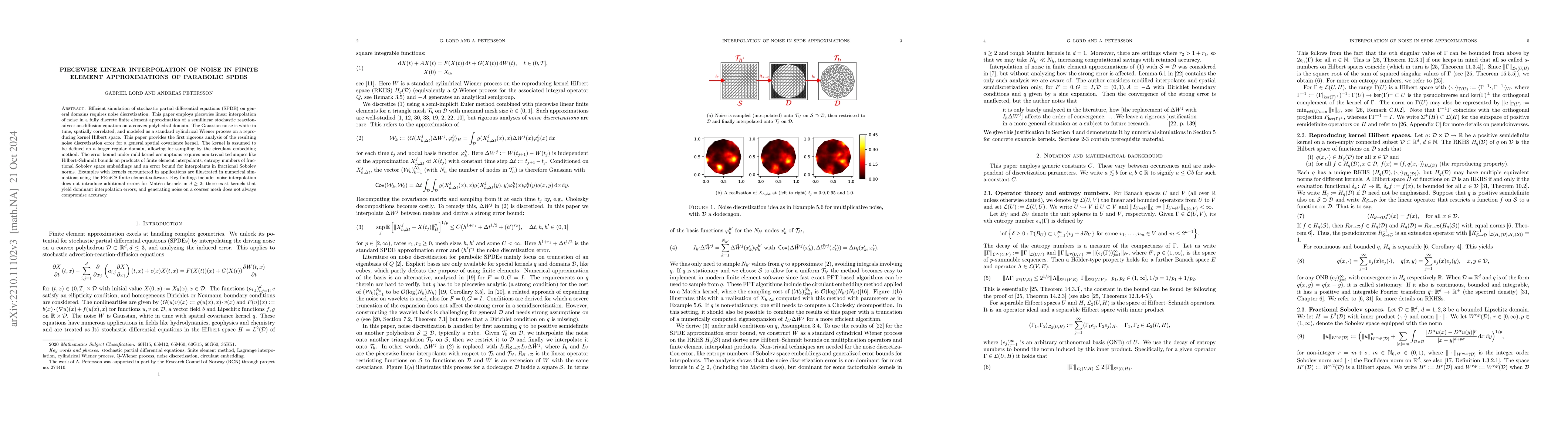

Efficient simulation of stochastic partial differential equations (SPDE) on general domains requires noise discretization. This paper employs piecewise linear interpolation of noise in a fully discr...

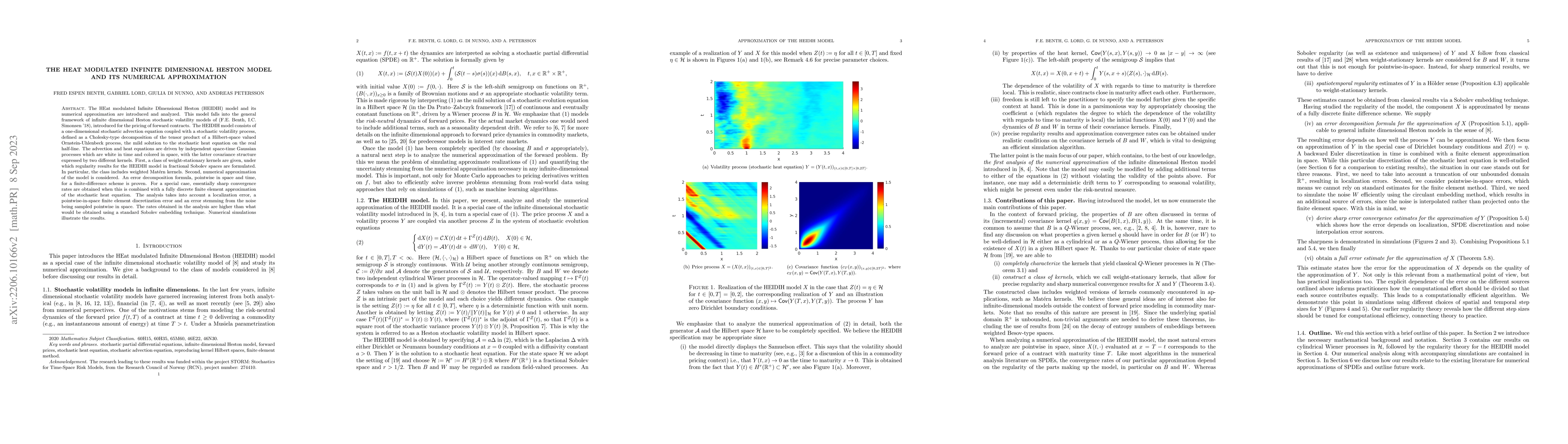

The HEat modulated Infinite DImensional Heston (HEIDIH) model and its numerical approximation are introduced and analyzed. This model falls into the general framework of infinite dimensional Heston ...

This paper introduces SPDE bridges with observation noise and contains an analysis of their spatially semidiscrete approximations. The SPDEs are considered in the form of mild solutions in an abstra...

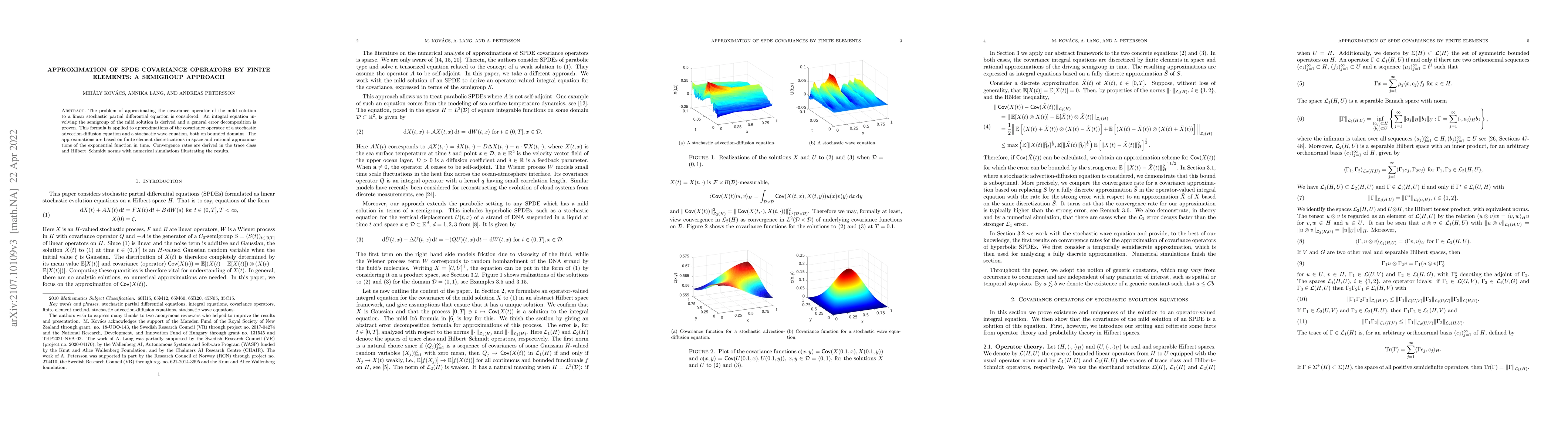

The problem of approximating the covariance operator of the mild solution to a linear stochastic partial differential equation is considered. An integral equation involving the semigroup of the mild...

Regularity estimates for an integral operator with a symmetric continuous kernel on a convex bounded domain are derived. The covariance of a mean-square continuous random field on the domain is an e...

A numerical analysis for the fully discrete approximation of an operator Lyapunov equation related to linear SPDEs (stochastic partial differential equations) driven by multiplicative noise is consi...

We consider the numerical approximation of the mild solution to a semilinear stochastic wave equation driven by additive noise. For the spatial approximation we consider a standard finite element me...

Stochastic partial differential equations (SPDEs) are often difficult to solve numerically due to their low regularity and high dimensionality. These challenges limit the practical use of computer-aid...

We develop an asymptotic limit theory for nonparametric estimation of the noise covariance kernel in linear parabolic stochastic partial differential equations (SPDEs) with additive colored noise, usi...

We study the problem of learning the law of linear stochastic partial differential equations (SPDEs) with additive Gaussian forcing from spatiotemporal observations. Most existing deep learning approa...